is a financial concept covered in this article. Facility Rental and Airport-Related Charges in Transportation Industries

Pennies don't fall from heaven, they have to be earned here on earth.

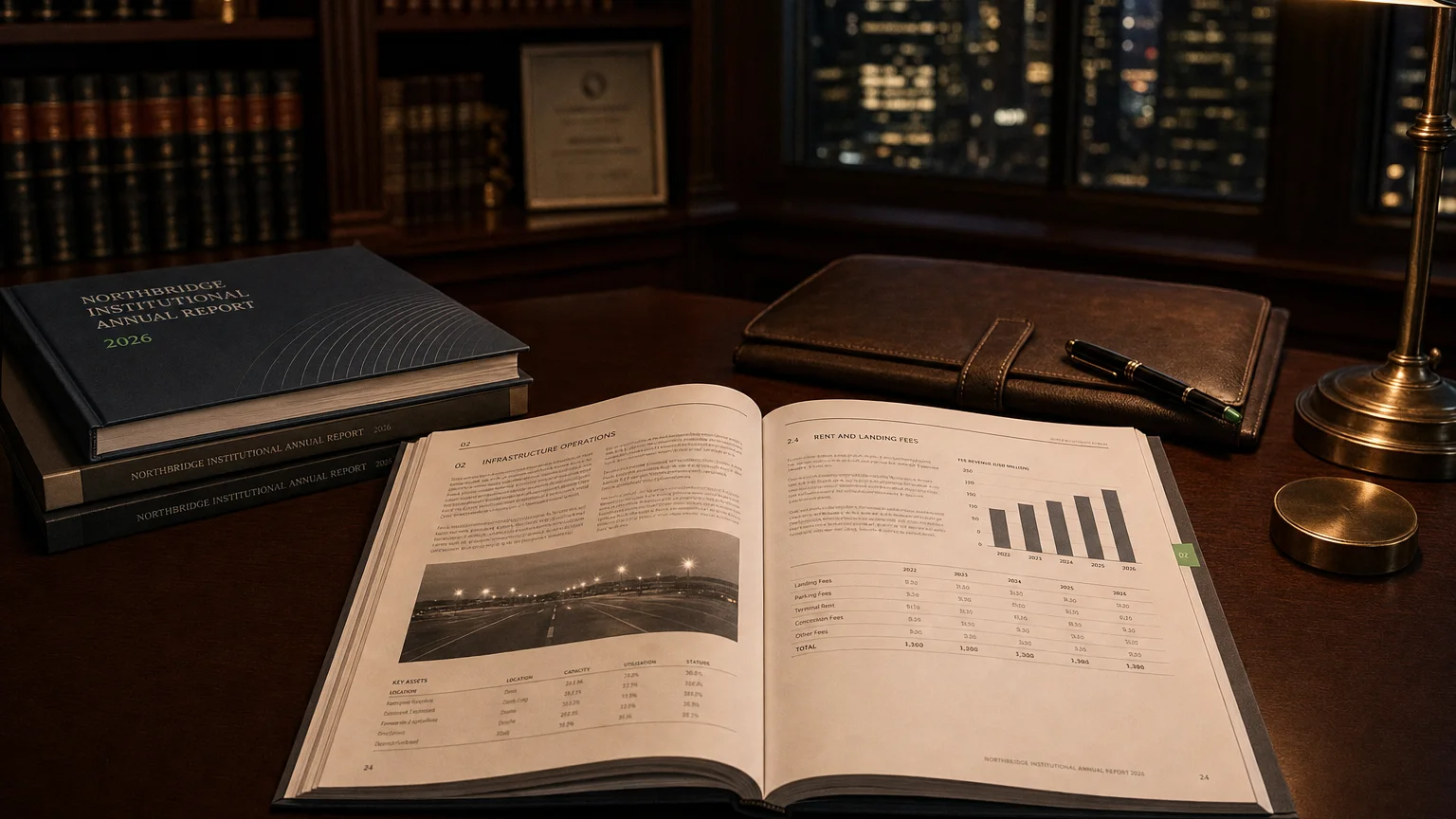

Rent and Landing Fees is an operating expense line item primarily seen in the airline, airport operations, and transportation sectors. It includes rental costs for terminal space, gates, hangars, counters, and office facilities at airports, as well as landing fees charged by airports based on aircraft weight, frequency, or time of day. These costs are essential for accessing airport infrastructure and are typically variable with flight volume or fixed under long-term leases. Reported within operating expenses, they significantly impact margins in capital-light airline models and are a key focus for cost management, route profitability, and negotiations with airport authorities.

What are Rent and Landing Fees?

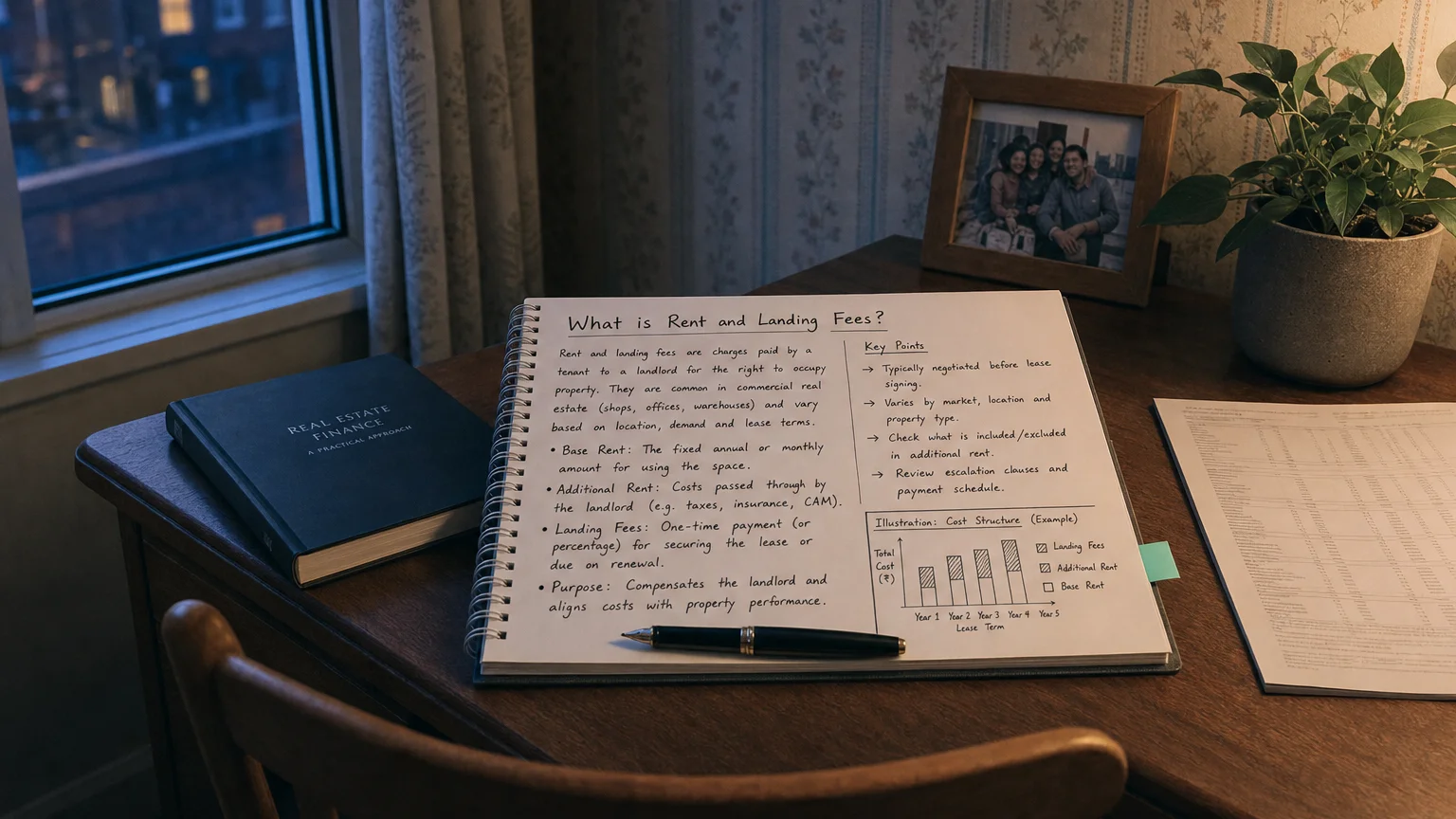

Rent and Landing Fees represent the charges airlines and transportation companies pay to airports for the use of infrastructure and airspace access.

Rent covers leased facilities (terminals, gates, ticket counters, baggage areas, hangars). Landing fees are per-operation charges based on maximum takeoff weight (MTOW), often with peak/off-peak pricing.

These are classified as operating expenses under US GAAP and IFRS because they are essential to revenue generation. Pre-ASC 842, most were pure rent expense; post-adoption, long-term leases are partially capitalized (depreciation + interest).

Major cost driver for airlines—often second only to labor and fuel.

Breakdown of Components

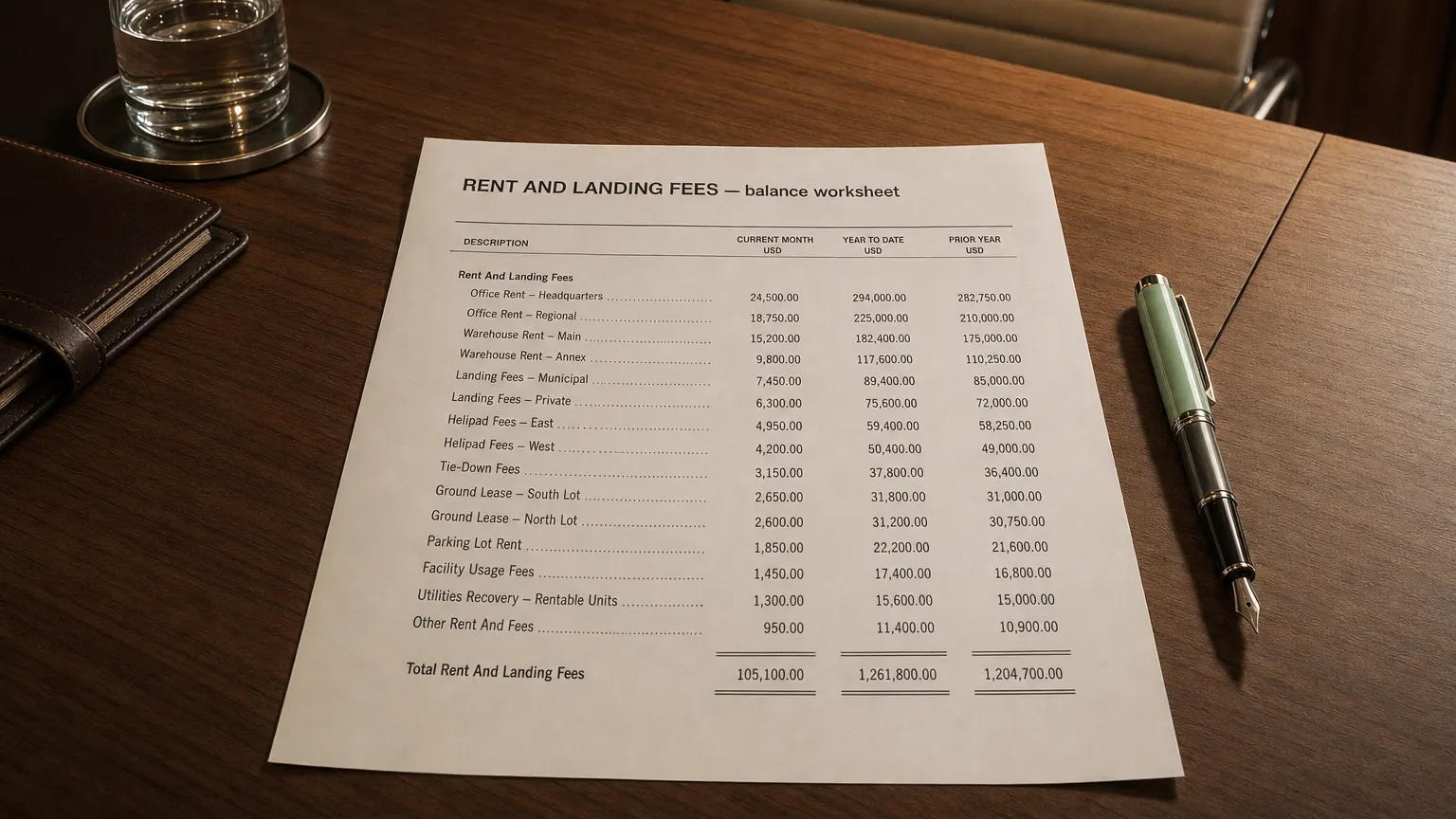

Typical items included:

Key Elements

- Terminal and gate rentals (fixed or per enplanement)

- Landing fees (weight-based, e.g., $5-15 per 1,000 lbs MTOW)

- Apron and parking fees (aircraft overnight stands)

- Counter and office space rent

- Hangar and maintenance facility leases

- Common use facility charges (CUTE/CUPPS systems)

- Passenger facility charges (PFC) passed through (sometimes netted)

Fees vary by airport—hub airports (e.g., ATL, ORD) charge premium rates.

“Pennies don’t fall from heaven, they have to be earned here on earth.”

— Margaret Thatcher, Prime Minister of the United Kingdom (1979-1990) Speech at Lord Mayor’s Banquet, London (1979)

How It Appears in the Income Statement

Common reporting:

Placement

- Separate line in airline income statements

- Within Other Operating Expenses

- Part of Airport Fees or Station Expenses

Reduces operating income; variable portion scales with ASMs (available seat miles).

Tip: Compare rent & landing fees per enplanement or per ASM for airline efficiency.

Examples

Example 1: Major Network Carrier

Annual operations: 1M flights, average MTOW 150K lbs.

Landing fees: 1,200 per flight = 1.8B Other facilities: 0.5B **Rent & Landing Fees**: 3.5B (~15% of op ex).

Example 2: Low-Cost Carrier

Focuses on secondary airports with lower fees.

Landing fees: 800M Rent & Landing Fees: $1.4B (lower % of op ex due to cost discipline).

Hub carriers pay premium; LCCs/ULCCs negotiate aggressively or use cheaper airports.

Importance in Financial Analysis

Analysts track rent & landing fees to:

- Evaluate unit cost structure (CASM ex-fuel)

- Assess airport concentration risk (slot constraints, monopoly pricing)

- Compare network strategy (hub premium vs. point-to-point efficiency)

- Forecast margin sensitivity to fee increases

Rising fees pressure margins; long-term contracts provide stability but limit flexibility.

Warning: Privatized or capacity-constrained airports can impose sharp increases—monitor negotiations.

Q · 01What is Rent And Landing Fees?+