is a financial concept covered in this article. Cost of Providing Employee Retirement and Other Post-Employment Benefits

When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.

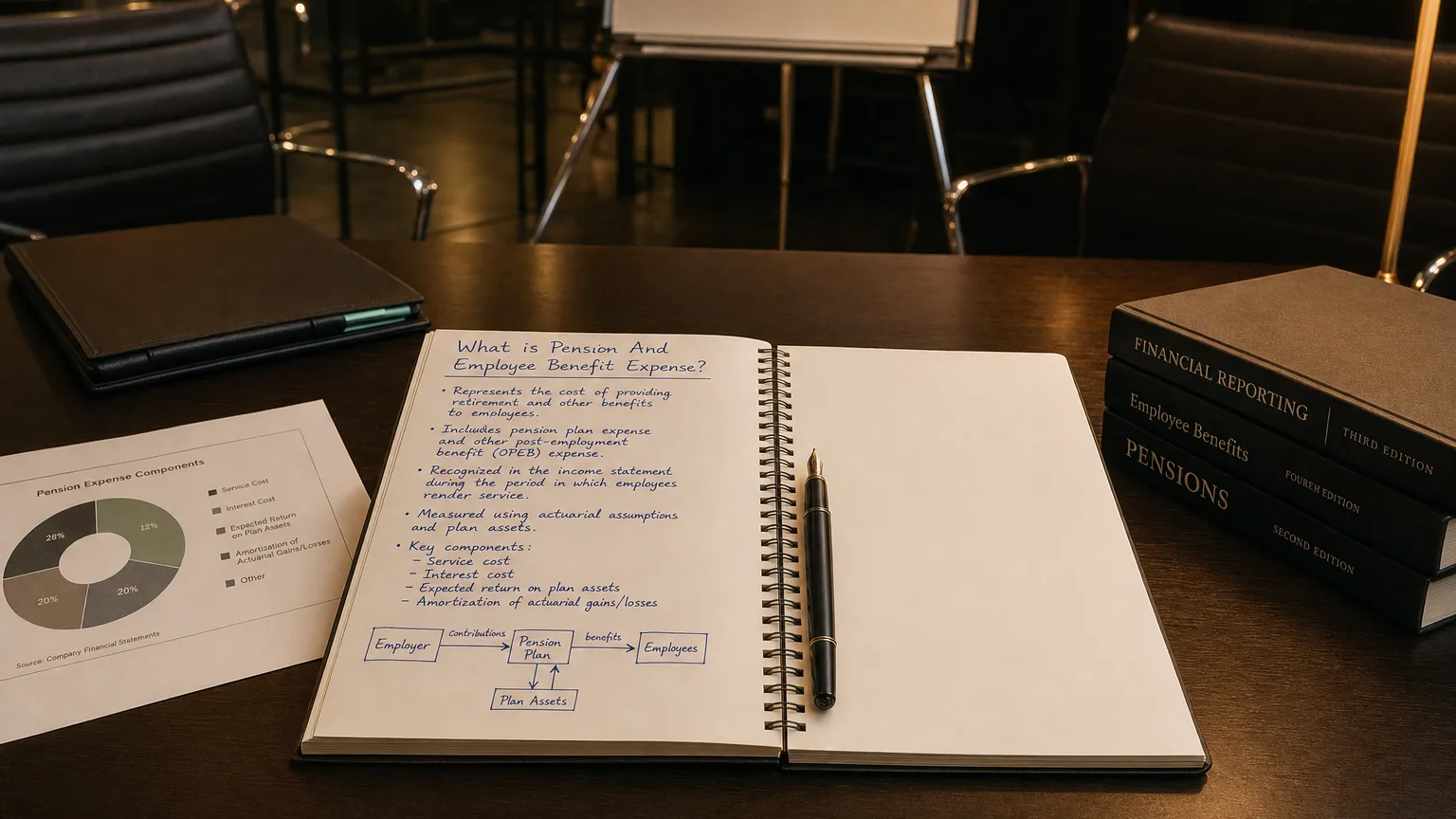

Pension and Employee Benefit Expense is the periodic cost a company recognizes for providing defined benefit pensions, other postretirement benefits (like healthcare), and sometimes other long-term employee benefits (severance, long-service awards). It’s a non-cash (mostly) expense in the income statement that reflects the cost of promising future benefits to employees for service rendered today.

What the Expense Includes

The expense breaks into several pieces that together show the cost of earning employee service this year:

- Service cost: Value of benefits earned by employees this period

- Interest cost: Unwinding of discount on future obligations

- Expected return on plan assets: Offset (reduces expense)

- Amortization of prior service costs/gains/losses

- Curtailments, settlements, special termination benefits

Service cost is the ‘true’ new cost; the rest is mostly accounting mechanics.

Under IFRS, remeasurements (actual vs. expected returns, assumption changes) go to OCI, not expense.

“When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

A Simple Example

Company has a pension plan promising fixed retirement payouts.

- Employees earn 8M

- Existing obligations grow with time → Interest cost $12M

- Plan assets expected to earn 15M credit

- Net Pension Expense: 12M - 5M

Actual assets earn 3M gain to OCI (not expense under many rules). Company contributes $10M cash → operating cash outflow.

Reported expense $5M, but cash and economics differ.

Key Drivers of the Expense

- Discount rate (lower rate → higher interest cost)

- Salary growth assumptions

- Expected long-term asset returns

- Employee demographics (longevity, turnover)

- Healthcare trend rates (for OPEB)

Small assumption tweaks swing expense by millions.

Where It Shows Up

- Income statement: Usually operating expenses (or sometimes below)

- Cash flow: Non-cash portions added back; contributions outflow

- Footnotes: Detailed reconciliation and assumptions

Often grouped in ‘Pension and other benefit costs’.

US GAAP vs. IFRS Differences

US GAAP

- Corridor amortization possible (smoothing)

- Remeasurements can hit P&L over time

IFRS

- Immediate remeasurements to OCI

- No corridor—full volatility in equity

What to Watch For

- Trend vs. headcount (rising per employee?)

- Assumption changes (rate drops spike cost)

- Cash contributions vs. expense (funding level)

- OCI buildup (hidden equity volatility)

- Industry comparison (legacy plans costlier)

Low discount rates in low-interest eras dramatically increase reported expense.