Raw Materials is a financial concept covered in this article. Unprocessed Materials Awaiting Entry into Production

In investing, you get what you don't pay for. Costs matter enormously.

Raw Materials are the basic inputs a company holds in inventory that will be used in the manufacturing process to create finished goods. These are unprocessed or minimally processed items—commodities, components, or substances—purchased from suppliers and stored until needed for production. They represent the starting point of the production cycle.

What Raw Materials Include

Raw Materials cover everything waiting to enter production:

- Natural resources (ore, timber, crude oil)

- Commodities (wheat, cotton, metals)

- Chemicals and compounds

- Purchased components (bolts, circuit boards)

- Packaging materials (if direct)

Indirect materials (supplies like glue or lubricants) are often in overhead rather than raw materials inventory.

Retailers have no raw materials—merchandise is their ‘finished goods’.

“In investing, you get what you don’t pay for. Costs matter enormously.”

— John C. Bogle, Founder, The Vanguard Group Common Sense on Mutual Funds (1999)

How They Fit in the Inventory Cycle

The flow looks like this:

- Raw Materials → purchased and stored

- Released to production → become Work In Process

- Completed → Finished Goods

- Sold → Cost of Goods Sold

Raw materials sit idle until requisitioned for manufacturing.

A Simple Example

A furniture maker:

- Buys lumber, fabric, foam → Raw Materials inventory $2M

- Starts building 500 chairs → releases $800k materials to Work In Process

- Raw Materials drops to $1.2M

- Chairs finished → $800k materials (plus labor/overhead) move to Finished Goods

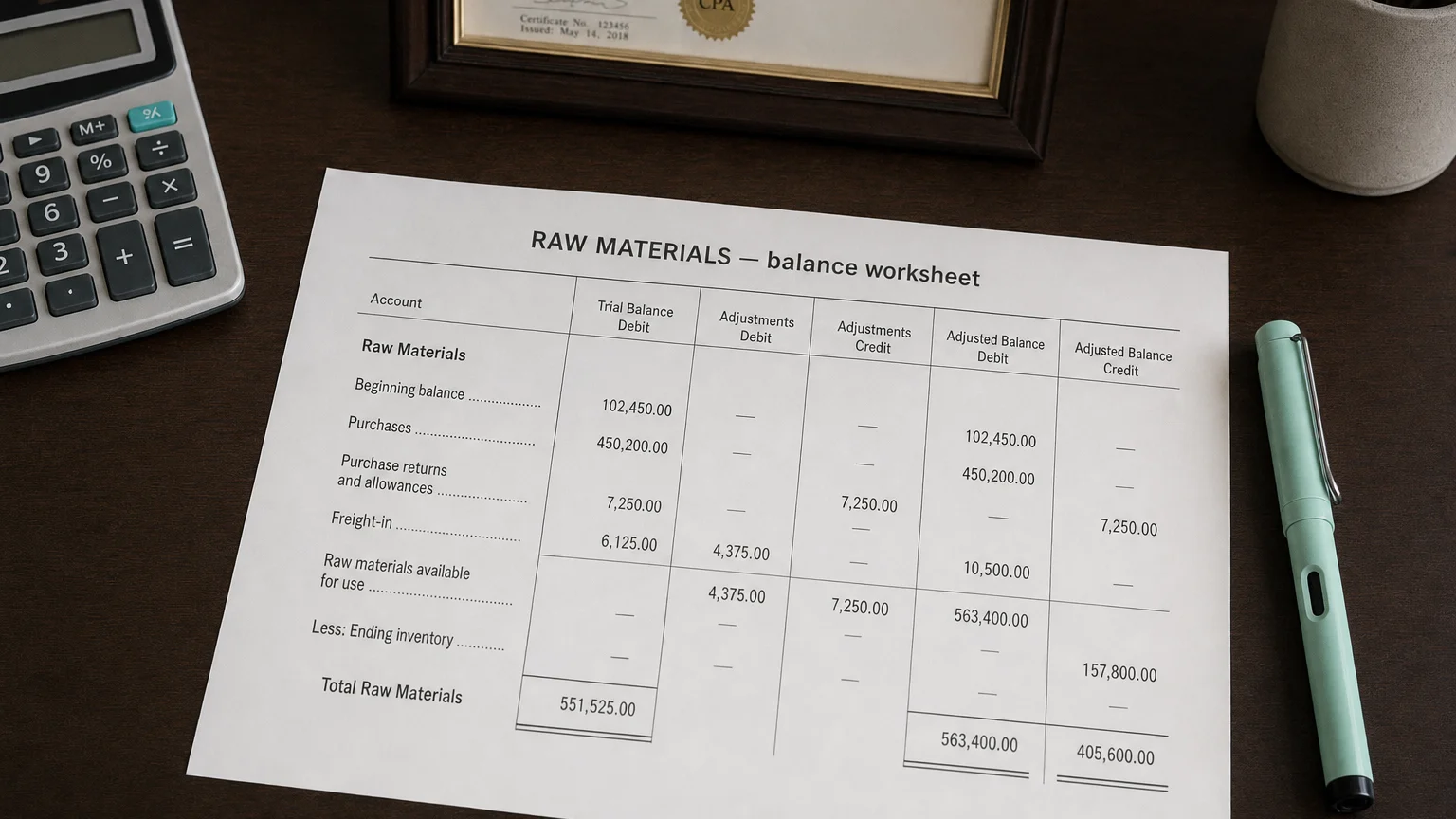

Accounting Treatment

- Purchased at cost (invoice + freight + duties)

- Valued at lower of cost or NRV

- Cost flow: FIFO, LIFO, Weighted Average

- Physical counts to verify book balance

- Write-downs for obsolescence/spoilage

Commodity price swings can create gains/losses if using LIFO (US) vs. FIFO.

Balance Sheet Presentation

Under current assets → Inventory as:

- ‘Raw Materials’

- First line in inventory breakdown

- Net of obsolescence reserve

Footnotes detail valuation method and major categories.

What to Watch For

- Level vs. production needs (stockouts risk?)

- Growth vs. sales (overbuying?)

- Commodity exposure (price volatility)

- Obsolescence risk (tech changes, spoilage)

- Supplier concentration

Rising raw materials without production increase often signals hedging or anticipated shortages.

Q · 01What is Raw Materials?+