Sale of Business is a financial concept covered in this article. Cash Proceeds from Divesting a Business Unit or Subsidiary

When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.

Sale of Business is the cash inflow a company receives when it sells a business segment, division, subsidiary, or significant portion of its operations to another party. This line appears in the investing section of the cash flow statement and often represents a major one-time event as the company exits non-core or underperforming parts of its portfolio.

What It Represents

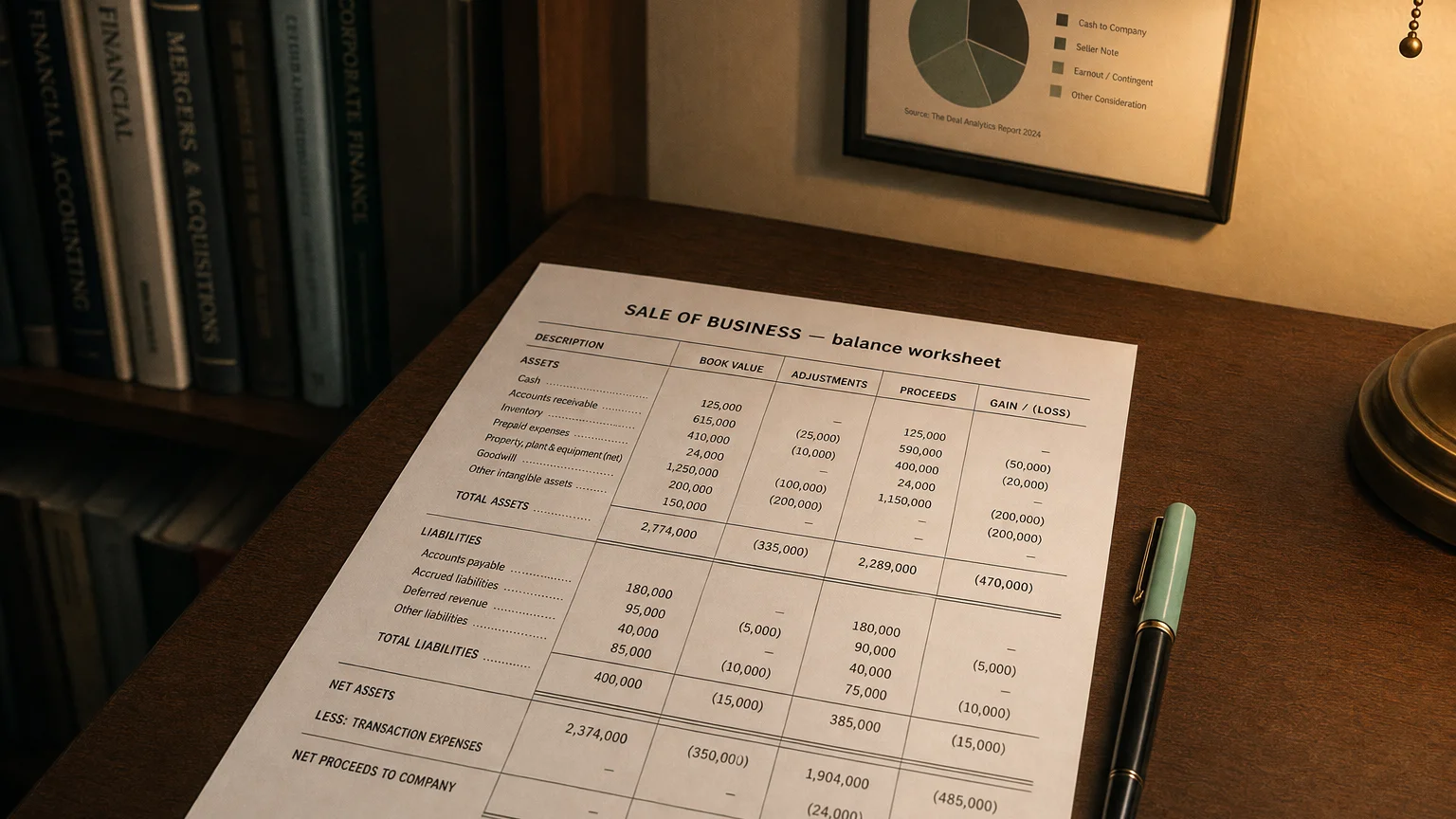

Sale of Business captures the actual cash proceeds from transferring ownership of a business unit or subsidiary.

- Gross cash received from buyer

- Minus direct transaction costs if netted (fees, legal)

- Excludes assumed liabilities or working capital adjustments (handled separately)

The accounting gain/loss (proceeds minus book value of net assets sold) hits the income statement separately.

If meets discontinued operations criteria, cash flows may be grouped separately.

“When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

A Real-World Example

Conglomerate decides its consumer electronics division no longer fits strategy.

- Sells division for $800M cash

- Pays $20M advisor/legal fees

- Sale of Business: +800M gross)

- Division net assets book value 300M pre-tax gain in P&L

Massive investing cash boost—often used for debt paydown, buybacks, or new acquisitions.

Common Reasons for Sales

- Refocus on core competencies

- Raise cash to reduce leverage

- Unlock hidden value (‘sum of parts’ higher)

- Exit low-margin or troubled units

- Regulatory/antitrust requirements

- Respond to activist investors

Accounting and Presentation

- Cash inflow in investing activities

- Labeled ‘Sale of Business’ or ‘Proceeds from Disposal of Subsidiary’

- Gross proceeds common; net if costs significant

- Gain/loss in income statement (often ‘Other gains’ or discontinued ops)

- Discontinued ops treatment if material and strategic shift

Working capital true-up or earn-outs may adjust cash later.

Impact on Financials

- Large investing cash inflow

- Removes sold unit’s assets/liabilities

- Future revenue/profit reduced

- Potential margin improvement (if low-margin unit)

- One-time gain boosts earnings

What to Watch For

- Proceeds vs. book value (gain size)

- Use of cash (productive or just balance sheet repair?)

- Revenue/earnings lost from sold unit

- One-time nature (not sustainable)

- Strategic rationale and execution timing

Repeated sales may indicate lack of focus or ongoing issues.

Q · 01What is Sale Of Business?+