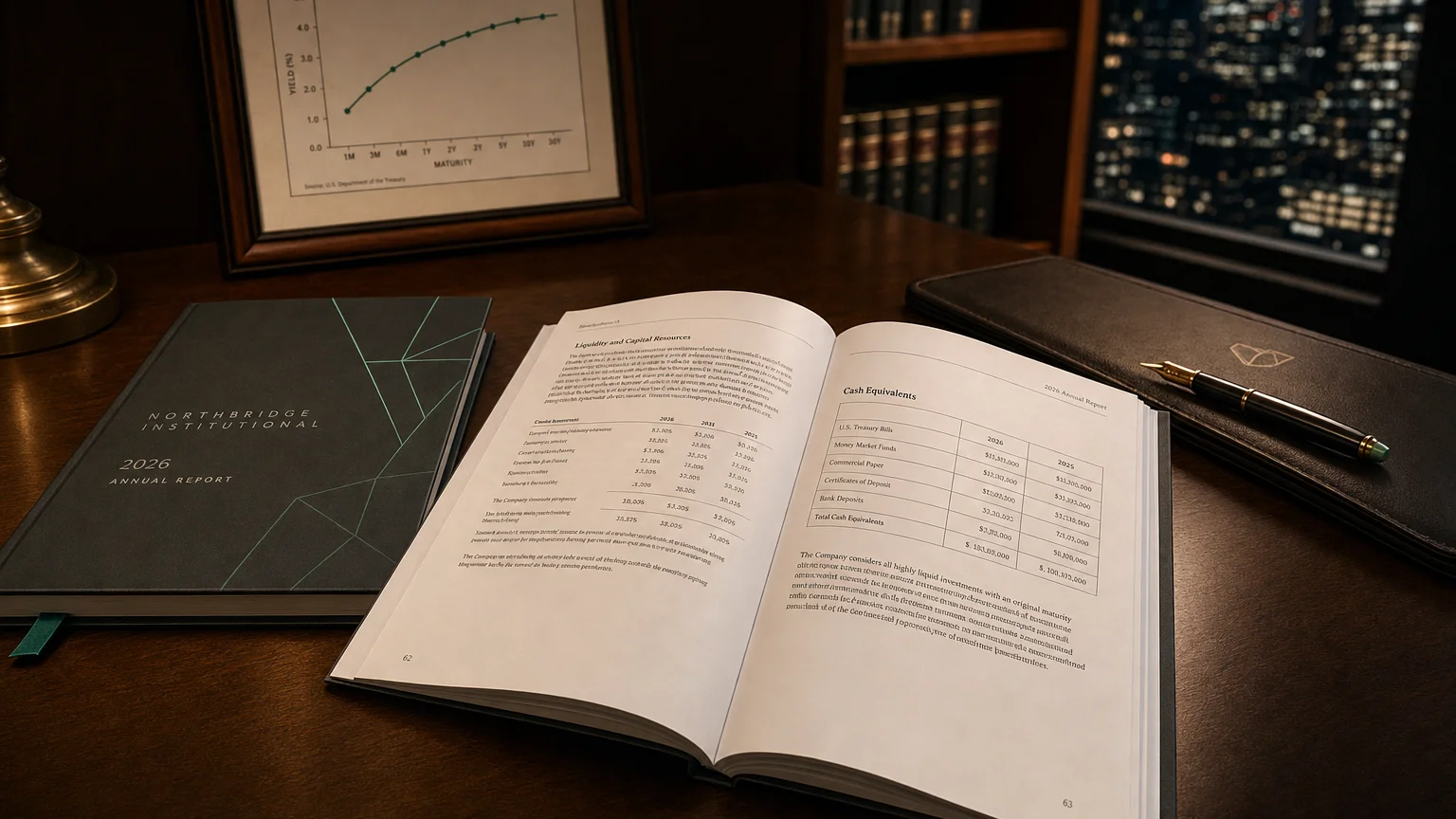

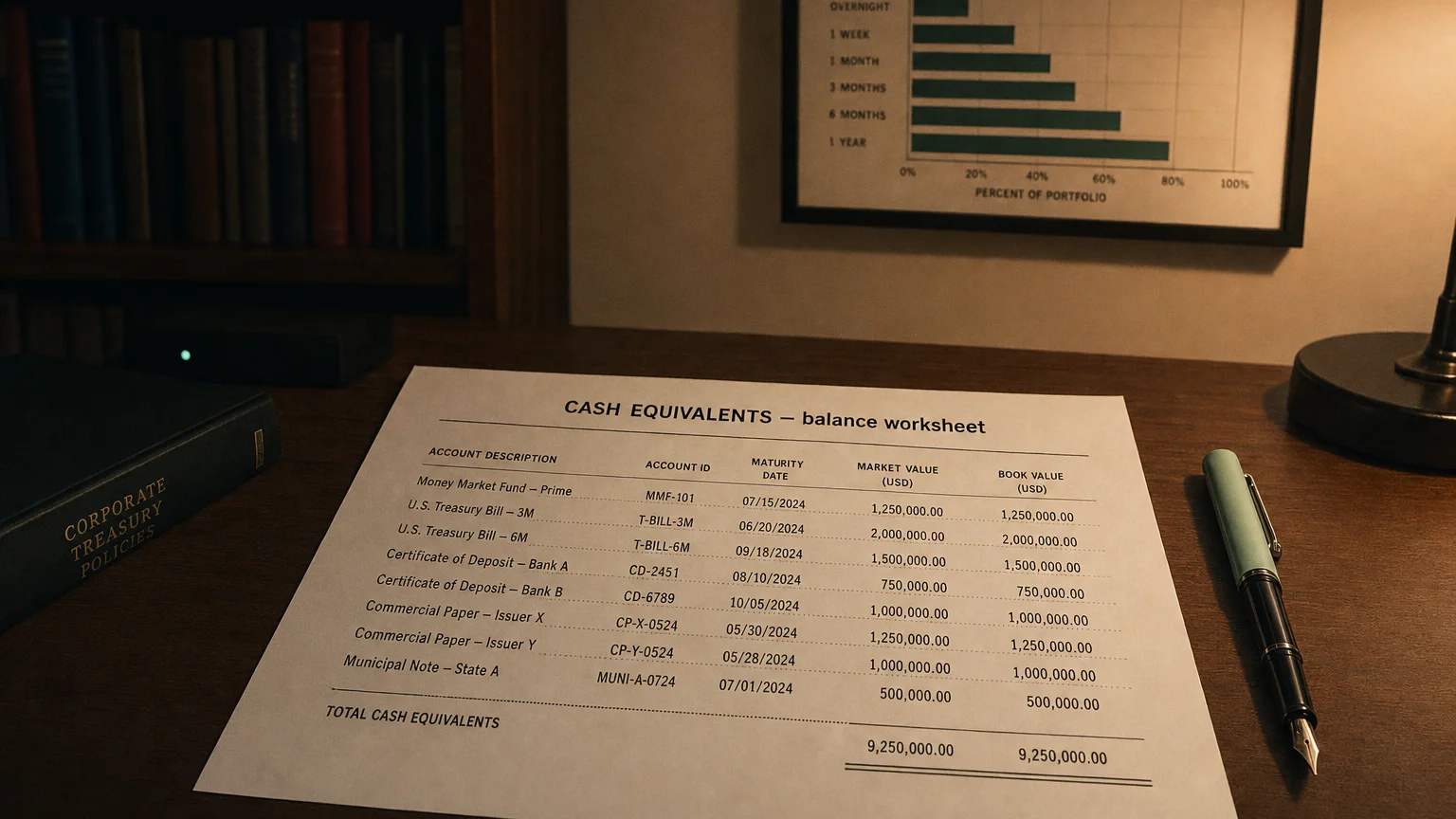

Cash equivalents are investments with original maturities of 90 days or less that are readily convertible to a known cash amount with insignificant risk of value change. Common examples include Treasury bills, commercial paper, and money market fund shares.

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

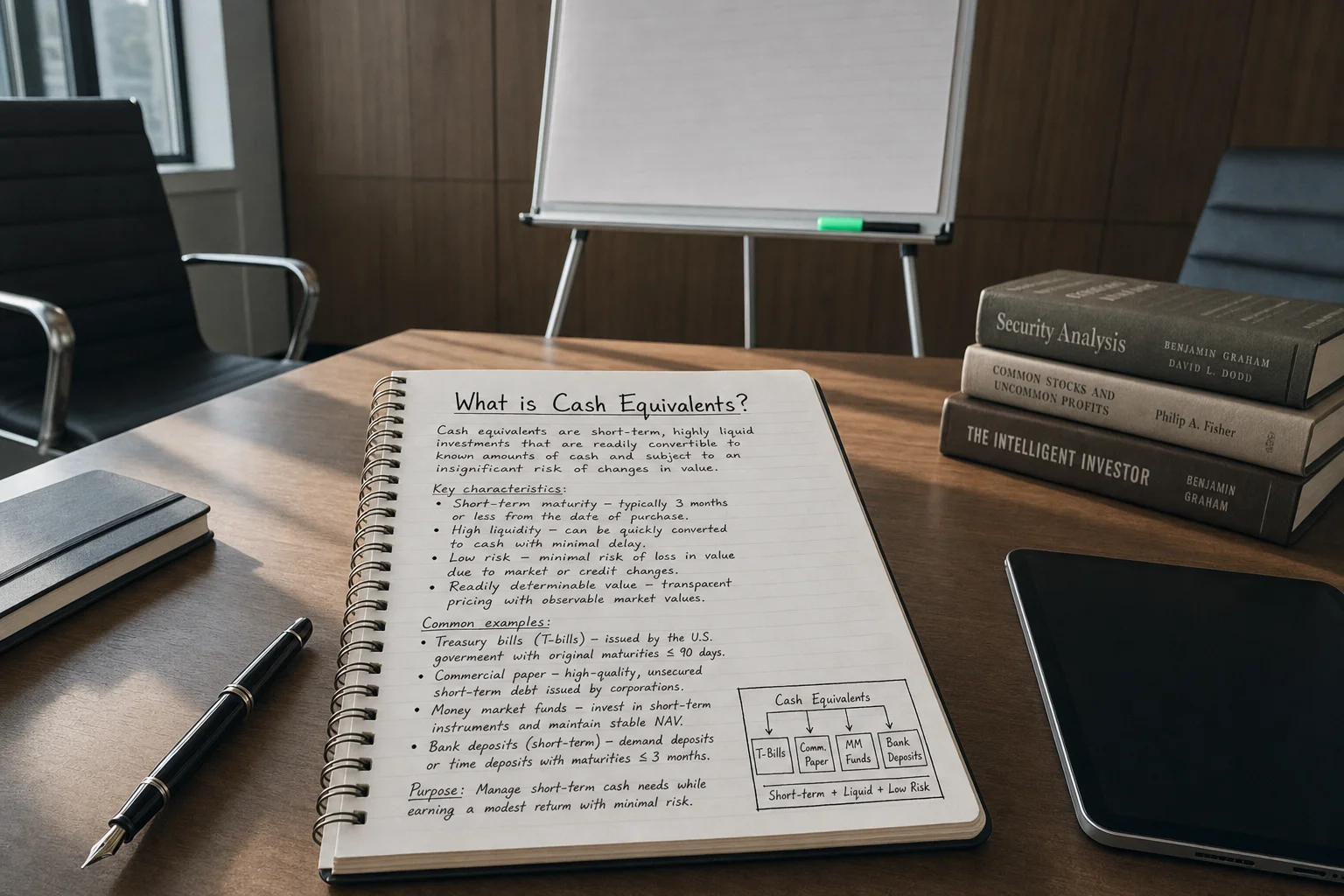

In financial accounting, cash equivalents are defined as very short-term, liquid investments that a company holds. Under both IFRS (IAS 7) and US GAAP (ASC 230), they are readily convertible to known amounts of cash and carry only an insignificant risk of value changes. In practice, this means the investment’s original maturity is typically three months or less from the purchase date, making them a crucial component of a company’s liquidity.

Defining Criteria

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

For an investment to be classified as a cash equivalent, it must satisfy a strict set of criteria focused on liquidity and risk:

- Original Short Maturity: The investment must typically have an original maturity of 90 days or less from its purchase date. An important distinction is that this applies to the original term, not the remaining time to maturity.

- High Liquidity: The asset must be able to be quickly sold or converted to cash, often in an active market, without significant delay or transaction costs.

- Low Risk: The investment’s value must be stable. The risk of changes in value due to interest rate fluctuations or credit issues must be insignificant. If an asset’s value could fluctuate materially, it is not a cash equivalent.

Common Examples of Cash Equivalents

Typical Instruments

Distinctions and Importance

It is crucial to distinguish cash equivalents from other liquid assets. Cash itself includes physical currency and demand deposits with no maturity. Other short-term investments, like a 6-month Treasury bill or common stocks, are excluded because they fail the strict criteria—either their original maturity is too long or they carry market risk and price volatility. Only the shortest, safest, and most liquid instruments pass the test to become cash equivalents.

Cash equivalents are reported together with cash in a combined line item, typically titled “Cash and Cash Equivalents,” at the very top of the current assets section of the balance sheet. This placement reflects their status as the company’s most liquid resources.

Why It Matters: “Cash is King”

This pool of assets is vital for assessing a company’s financial health. It forms the readily available buffer for operations, allowing a company to meet short-term needs like payroll and supplier payments. A strong cash and equivalents balance signals robust liquidity, while a low balance can indicate risk in covering short-term debts.

Q · 01What qualifies as a cash equivalent under US GAAP and IFRS?+

Q · 02Are money market funds always cash equivalents?+

Q · 03Why does original maturity matter more than remaining maturity?+

Q · 04Can equity securities ever be cash equivalents?+

Q · 05Where are cash equivalents reported on the balance sheet?+