is a financial concept covered in this article. Long-Term Amounts Owed to Related Entities or Individuals

When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.

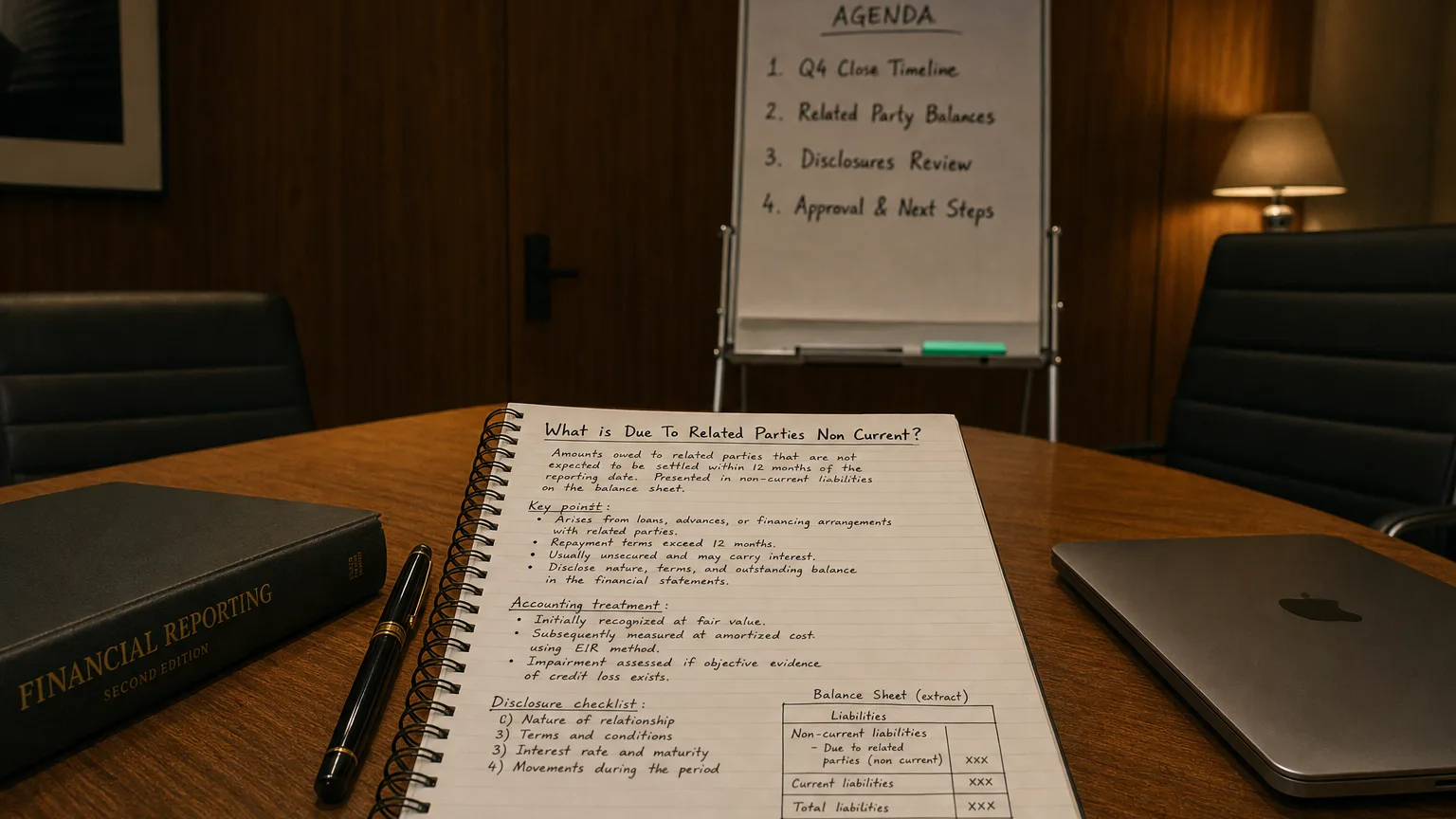

Due to Related Parties Non Current represents the long-term portion of amounts owed by the company to related parties—such as parent companies, subsidiaries, joint ventures, affiliates, key management personnel, or significant shareholders. These are obligations not expected to be settled within 12 months, often arising from intercompany loans, advances, or operational transactions.

Definition and Scope

Due to Related Parties Non Current are balances owed to entities or individuals with significant influence or control over the company (or vice versa). The non-current classification applies when settlement is not required within 12 months.

These are distinct from third-party debt due to potential non-arm’s-length terms (e.g., below-market interest).

Related party definition per IAS 24/ASC 850 includes common control, key management, and close family members.

“When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

Common Examples

- Long-term loans from parent company or major shareholder

- Advances from affiliates for funding operations

- Deferred payments to related entities for assets/services

- Intercompany financing arrangements

- Loans from directors or key executives

- Balances from joint venture funding

Often seen in private companies, conglomerates, and multinational groups with centralized treasury.

Accounting and Disclosure Requirements

Treatment:

- Recorded at amortized cost (if loan) or nominal amount

- Interest imputed if below-market (except certain intragroup)

- Classified current/non-current by expected settlement

- Extensive note disclosure: nature, terms, interest rates, balances

IAS 24/ASC 850 mandate detailed related party disclosures to highlight potential conflicts.

Balance Sheet Presentation

Shown under non-current liabilities as:

- ‘Due to Related Parties Non Current’

- ‘Long-Term Amounts Due to Related Parties’

- ‘Non-Current Related Party Payables’

- Sometimes aggregated in ‘Other Non Current Liabilities’

Footnotes provide counterparty names, terms, and transaction details.

Why These Balances Exist

- Group treasury funding (low-cost internal financing)

- Tax-efficient capital allocation

- Support for subsidiaries or projects

- Shareholder loans in private companies

- Cash pooling arrangements

Often more flexible and cheaper than external debt.

Analytical Implications

These balances signal:

- Dependence on related party funding

- Potential off-market terms (subsidized financing)

- Risk if parent/owner faces issues

- Governance concerns (conflict of interest)

- Tax authority scrutiny (transfer pricing)

Large or growing balances may indicate weak standalone credit or aggressive related party support.