An essential guide to the miscellaneous long-term obligations on a company's balance sheet that don't fit into major debt categories.

It does not matter how frequently something succeeds if failure is too costly to bear.

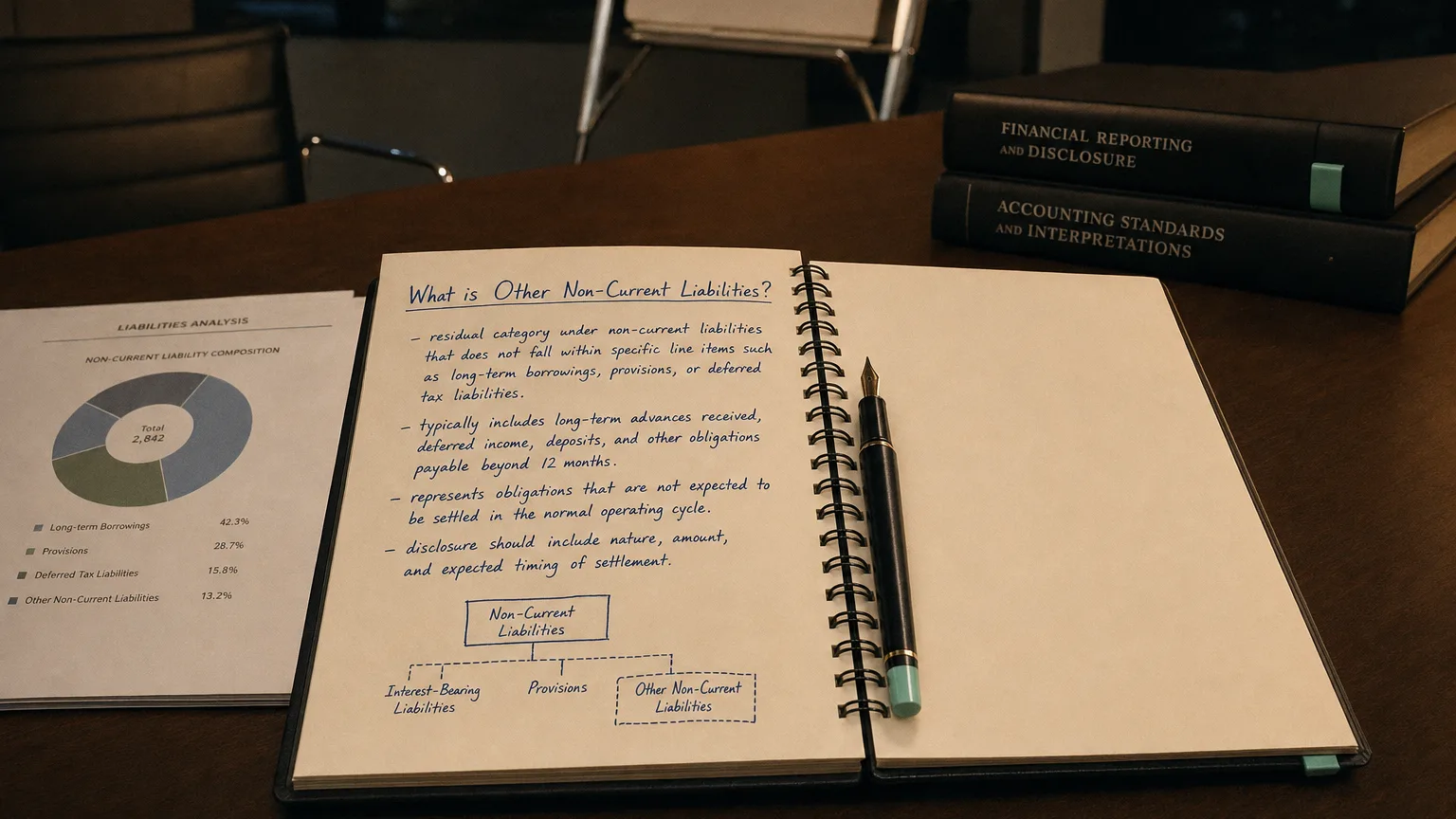

Other Non-Current Liabilities is a catch-all category on the balance sheet that groups together long-term obligations not classified under a specific line item. It includes miscellaneous liabilities that are due in more than one year and don’t fit neatly into major categories like bonds payable or long-term debt. This line item represents obligations that are too small or varied to list individually on the face of the balance sheet but are important for a complete picture of a company’s financial commitments.

Typical Components and Examples

Other non-current liabilities can include a range of long-term obligations. Common examples include:

- Deferred Tax Liabilities (DTLs): Arise from timing differences between financial and tax accounting. Under both IFRS and U.S. GAAP, these are always classified as non-current.

- Asset Retirement Obligations (AROs): Long-term provisions for the future costs of dismantling facilities or remediating environmental damage, common in energy or mining industries.

- Long-Term Provisions: Reserves for expected future costs, such as product warranties extending beyond one year, legal contingencies, or environmental cleanup liabilities.

- Deferred or Unearned Revenue (Long-Term Portion): Payments received from customers for services or goods to be delivered over multiple years.

- Post-Employment Benefit Obligations: Smaller pension liabilities or retiree healthcare obligations that are not material enough to be disclosed separately.

- Uncertain Tax Positions: Liabilities for tax positions that may be challenged by tax authorities, with the timing of resolution being uncertain and long-term.

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

How They Differ from Other Liability Categories

vs. Current Liabilities

The primary difference is the time to settlement. Current liabilities are due within 12 months, representing an immediate call on a company’s resources. Other non-current liabilities are due in the long term, beyond the next year.

vs. Long-Term Debt

Specific, significant, interest-bearing obligations like bonds payable or long-term bank loans are typically shown on a dedicated ‘Long-Term Debt’ line. ‘Other Non-Current Liabilities’ is an umbrella category for more miscellaneous, often non-debt obligations that are not material enough to warrant their own line item.

Importance for Financial Analysis

Although it may seem like a residual category, analysts pay close attention to this line item:

- Hidden Obligations: This category can house significant commitments. Analysts read footnotes carefully to understand its composition, especially if the balance is large or changes significantly.

- Future Cash Flow Impacts: Many items in this category represent future cash outflows. A buildup of legal or environmental provisions could foreshadow substantial future payments.

- Solvency and Leverage Ratios: These liabilities contribute to total liability figures used in ratios like Debt-to-Equity. Some components, like pension obligations, have debt-like qualities and are factored into risk assessments.

- Quality of Earnings: Changes in provisions within this category can affect the income statement. Analysts check if a company is building appropriate reserves or releasing them to temporarily boost earnings.

Real-World Example

Apple Inc.’s 2018 Form 10-K revealed that a ‘significant portion’ of its other non-current liabilities was a one-time U.S. repatriation tax payable in installments over several years. An investor who ignored the footnotes might miss this sizable future cash obligation.

Accounting and Regulatory Framework (GAAP vs. IFRS)

Both U.S. GAAP and IFRS recognize the distinction between current and non-current liabilities. They also have guidelines to ensure important items are not hidden in the ‘other’ category:

- U.S. GAAP/SEC Rules: Regulation S-X requires that if any single component of ‘Other Liabilities’ exceeds 5% of total liabilities, it must be disclosed separately on the balance sheet or in a note.

- IFRS: While not having a strict percentage rule, the principle of materiality under IAS 1 serves a similar purpose. If an item is material to understanding the company’s financial position, it should be presented separately.

In both frameworks, it is common to find a footnote titled ‘Other Liabilities’ that breaks down the major components, providing crucial context for analysts.