A guide to understanding how companies use financial assets for returns and strategic purposes, and how they are reported on the balance sheet.

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

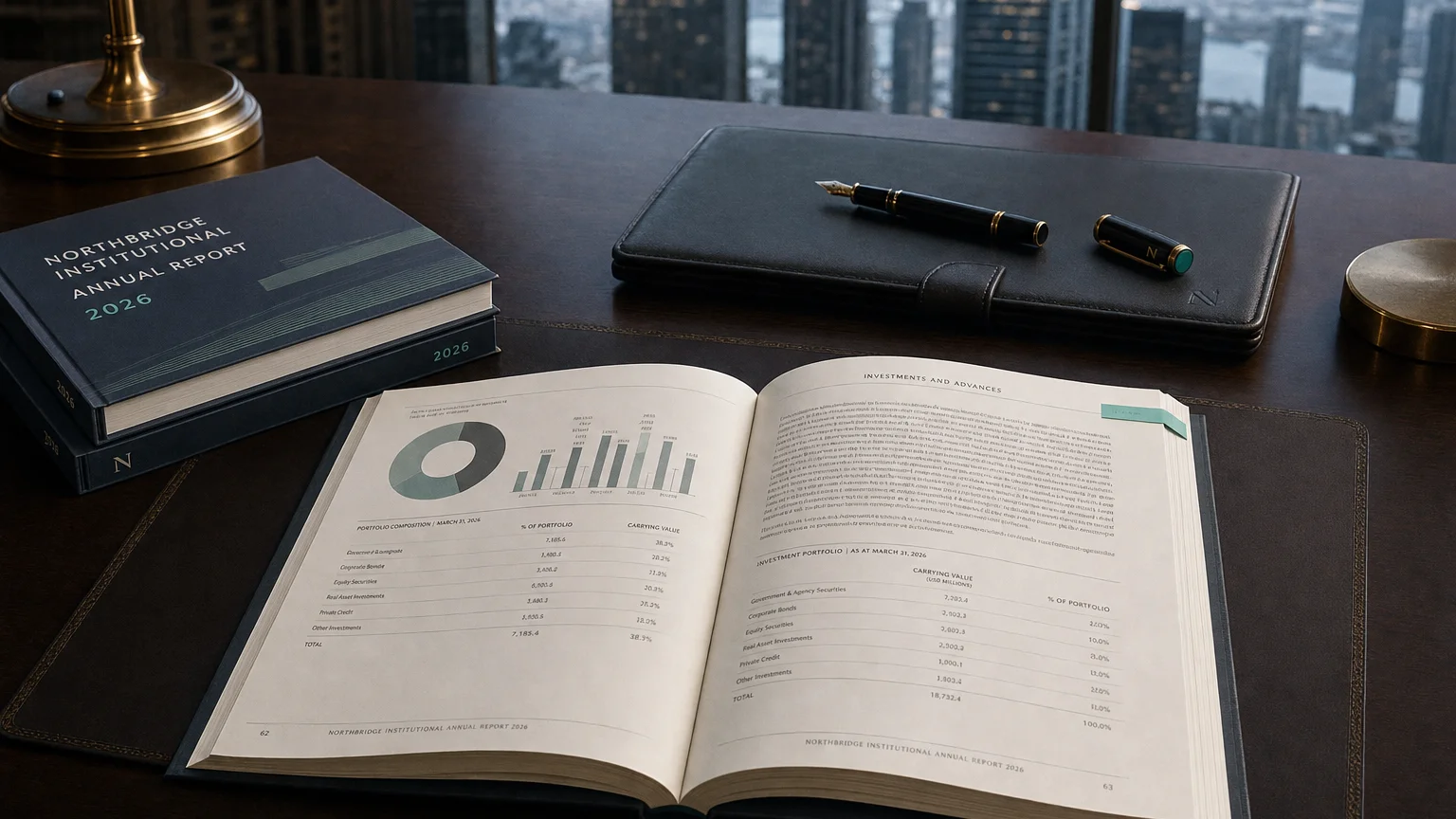

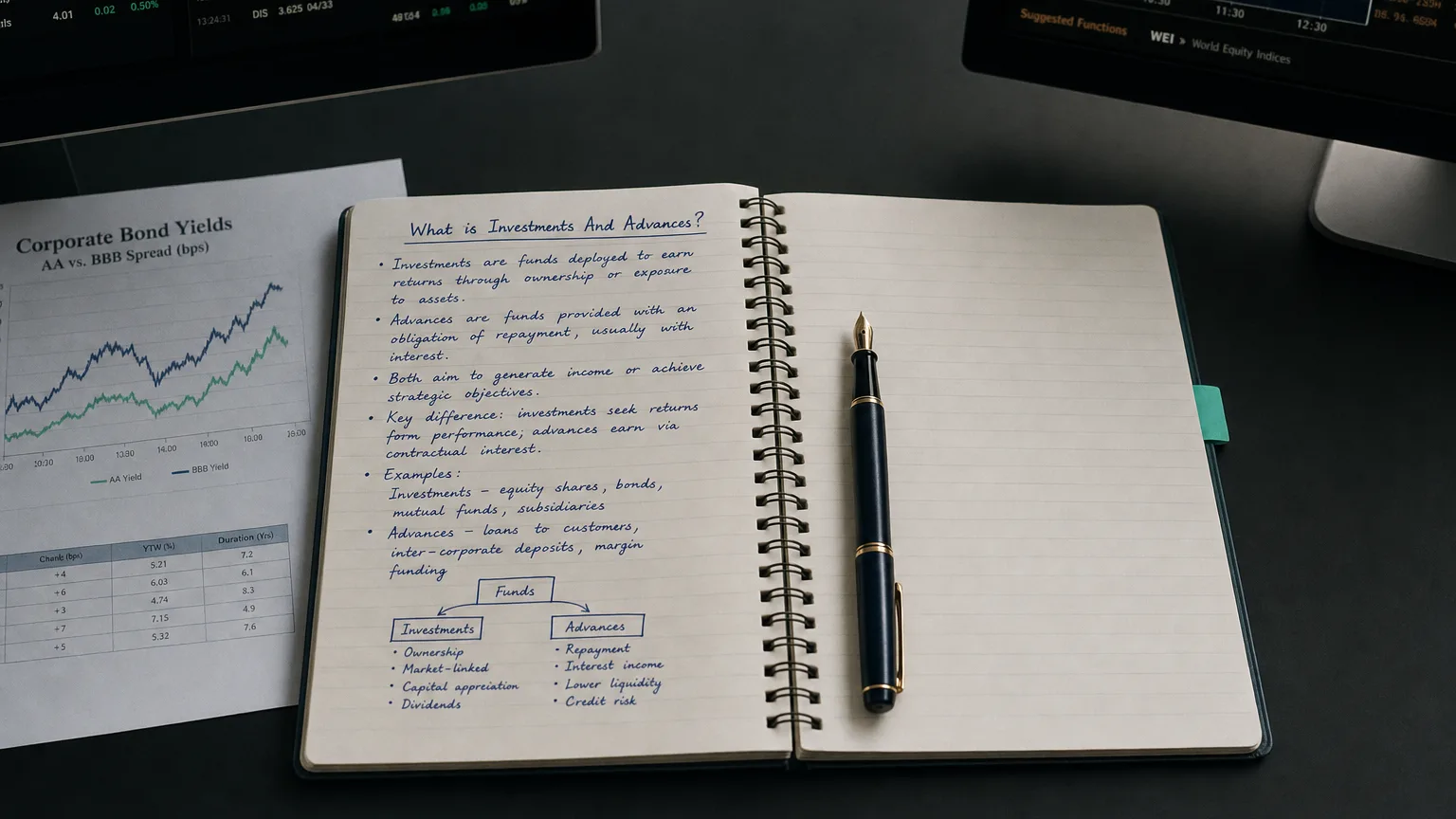

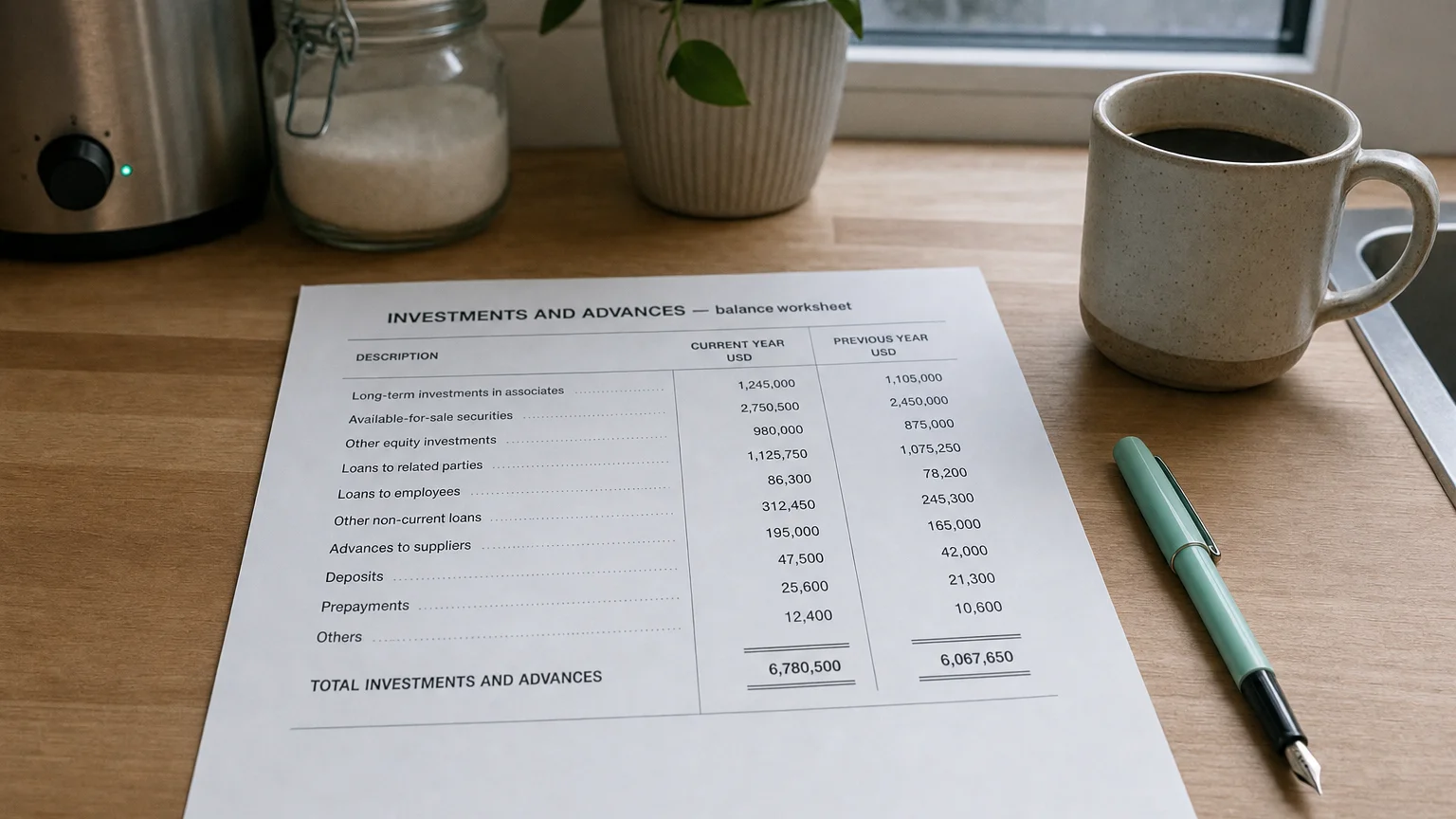

The “Investments and Advances” line item on a company’s balance sheet represents financial assets that are not part of its core operations, such as various investments and any advance payments or loans the company has made. It is a component of the company’s total assets. In essence, this category aggregates assets that can generate returns or be recovered in the future, rather than assets used directly in day-to-day operations.

What Does ‘Investments and Advances’ Include?

This category is broadly composed of two main types of assets:

- 1. Investments: These are funds the company has put into external opportunities to earn a return through interest, dividends, or capital gains. They can range from holdings of stocks and bonds to ownership stakes in subsidiaries or joint ventures.

- 2. Advances: This refers to amounts the company has paid or lent out with the expectation of future benefit or repayment. This includes loans to subsidiaries or affiliates and advance payments to suppliers or employees (a form of prepaid expense).

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

Short-Term vs. Long-Term Classification

The accounting treatment and classification of investments and advances hinge on their intended holding period and liquidity.

Current vs. Non-Current

Short-Term Investments (Current Assets): Also known as marketable securities, these are financial assets the company intends to convert to cash within one year. They are highly liquid and used to earn a return on excess cash. Their value is often marked-to-market, with changes impacting the income statement.

Long-Term Investments (Non-Current Assets): These are assets the company plans to hold for more than one year. They are less liquid and held for strategic purposes, such as gaining influence over another company or earning long-term returns. They are not part of a company’s working capital.

This classification is crucial because it helps financial statement users distinguish between assets available to meet short-term needs and those tied up for longer-term strategic goals. It also signals which value changes are likely to affect current earnings.

Common Examples of Investments and Advances

- Equity Investments in Other Companies: Minority stakes in publicly traded or private companies. If held for over a year for strategic purposes, they are non-current assets.

- Debt Investments (Bonds and Notes): Holdings of corporate or government bonds. Short-term debt securities (like T-bills) are current assets, while bonds with multi-year maturities are long-term investments.

- Loans or Advances to Subsidiaries and Affiliates: Financing provided by a parent company to a related entity. These intercompany loans are typically classified as long-term assets.

- Advance Payments and Prepaid Expenses: Upfront payments for goods, services, or rent. If the benefit will be received within a year, it is a current asset. If it spans multiple years, the long-term portion is non-current.

Why This Category Matters in Financial Analysis

Analysts examine the ‘Investments and Advances’ line item to gain critical insights into a company’s strategy, performance, and risk profile.

- Liquidity Insight: The amount of short-term investments is a strong indicator of a company’s ability to meet its immediate obligations. A large portfolio of marketable securities bolsters liquidity ratios like the current and quick ratio.

- Earnings and Returns: These assets generate non-operating income through interest, dividends, and capital gains. Analysts separate this from core operating earnings to understand the true performance of the business versus its investment activities.

- Strategic Direction: A large balance of long-term investments can signal management’s strategy for future growth, such as acquiring stakes in suppliers, customers, or innovative startups.

- Risk Assessment: This category can also raise red flags. Analysts look for large or unusual advances to related parties, which may carry recovery risk. The footnotes are scrutinized to understand the nature and riskiness of the underlying investments.

Separating Operating vs. Non-Operating Assets

Good financial analysis distinguishes between operating assets (like inventory and PP&E) and non-operating assets like investments. This helps in calculating performance ratios like Return on Assets (ROA) more accurately, revealing whether the company is deploying its capital effectively in both its core business and its financial placements.

Q · 01What is Investments And Advances?+