is a financial concept covered in this article. Revealing Core Profitability by Removing One-Time Items

The intelligent investor is a realist who sells to optimists and buys from pessimists.

Normalized EBITDA (also called Adjusted EBITDA) is an EBITDA figure that has been “normalized” by removing unusual or non-recurring items that are not part of the company’s regular operations. The goal is to show a more realistic, recurring level of EBITDA that investors can expect in the future. Where standard EBITDA includes all items on the income statement (except interest, taxes, D&A), Normalized EBITDA differs by excluding one-time gains, one-time losses, and any expenses or revenues that are not expected to continue. This makes it a fairer, apples-to-apples metric for comparing companies and assessing performance over time.

What Is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is a measure of a company’s operating profit before accounting for financing costs, tax expenses, and certain non-cash charges. By excluding these items, EBITDA gives a clearer sense of the company’s core operating performance and cash earnings power. It’s widely used as a quick indicator of profitability and is often a starting point for valuing companies.

Common Normalization Adjustments

When calculating normalized EBITDA, analysts will add back or remove certain items from standard EBITDA. Here are some of the most common adjustments:

- Non-recurring legal fees or settlements: One-time legal expenses are added back because they are not expected to recur.

- Excess owner’s compensation: In private companies, owner salaries above a normal market rate are added back to reflect standard management costs.

- Restructuring or reorganization costs: Major one-time charges for layoffs, facility closures, or a business overhaul are excluded.

- One-time gains or losses on asset sales: A one-time gain from selling property would be subtracted, while a one-time loss would be added back.

- Asset write-downs or impairment charges: Large non-cash charges like a goodwill impairment are added back because they don’t reflect ongoing operations.

- Other non-operational items: Any other income or expense that is not related to core operations and is not recurring would be considered for adjustment.

“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

— Benjamin Graham, Author, The Intelligent Investor The Intelligent Investor (1949)

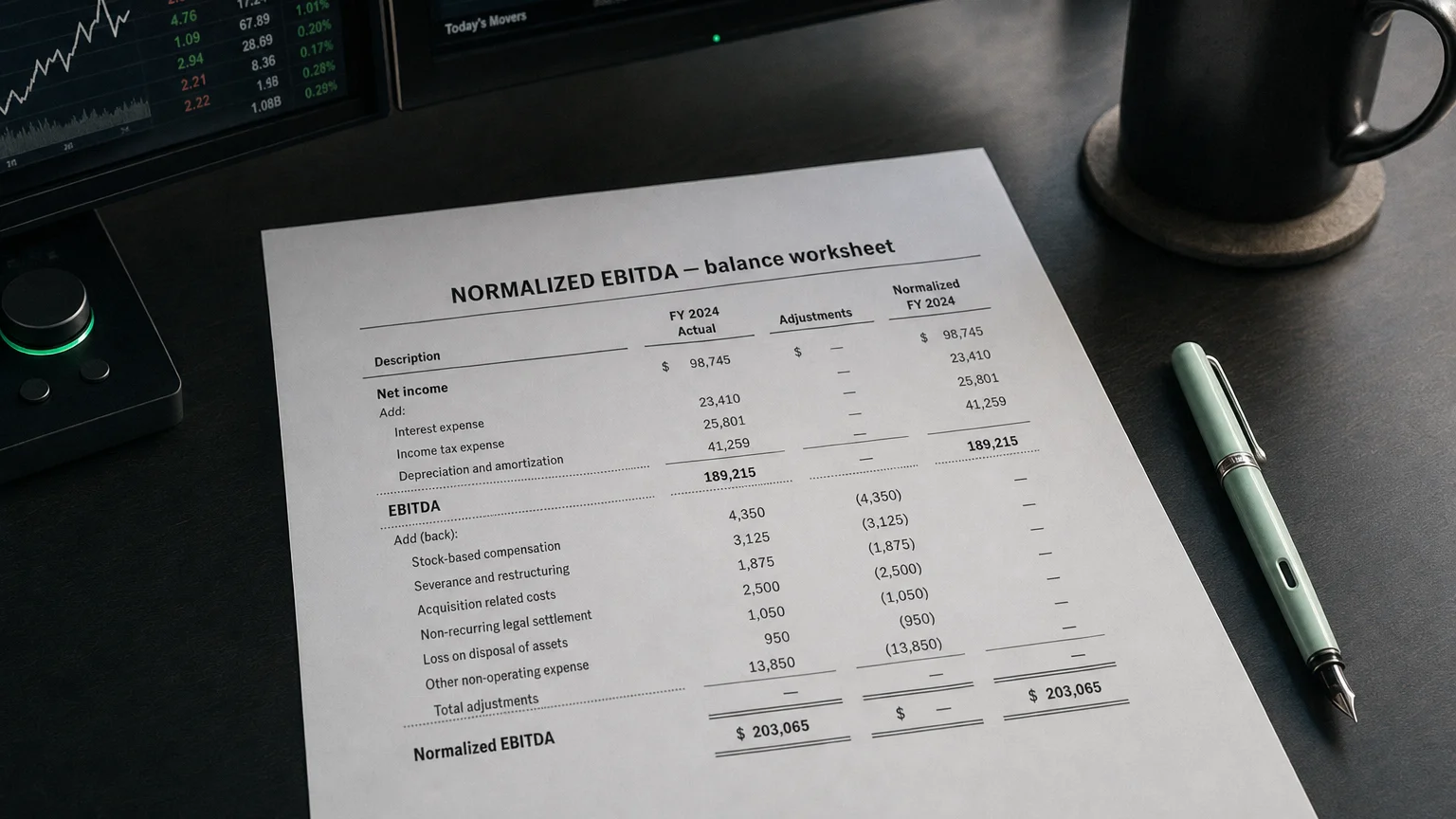

Step-by-Step Example: Calculating Normalized EBITDA

Let’s walk through a simplified example for Banana Inc.:

EBITDA Calculation

Now, we identify and apply normalization adjustments:

Normalization Adjustments

Formula: Normalized EBITDA = 0.35M + 1.50M - 5.65 million

In this example, the **Normalized EBITDA of 4.55M.

How Investors Use Normalized EBITDA

Normalized EBITDA is useful because it focuses on recurring earning potential. Here’s why that matters:

- Assessing Core Profitability: It provides a clearer view of sustainable earnings from the core business, without the noise of transient gains or losses.

- Comparability: It allows for more apples-to-apples comparisons between companies by removing idiosyncratic distortions from one-time events.

- Valuation and Investment Decisions: In practice, normalized EBITDA is often a key input for valuation. Buyers in mergers and acquisitions typically apply a valuation multiple to a company’s adjusted EBITDA.

- Estimating Future Performance: It is a better proxy for a company’s future maintainable earnings because it strips out the effects of one-off events.

Q · 01What is Normalized Ebitda?+