An explanation of Accumulated Other Comprehensive Income (AOCI) and how certain unrealized gains and losses are recorded directly to equity.

Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.

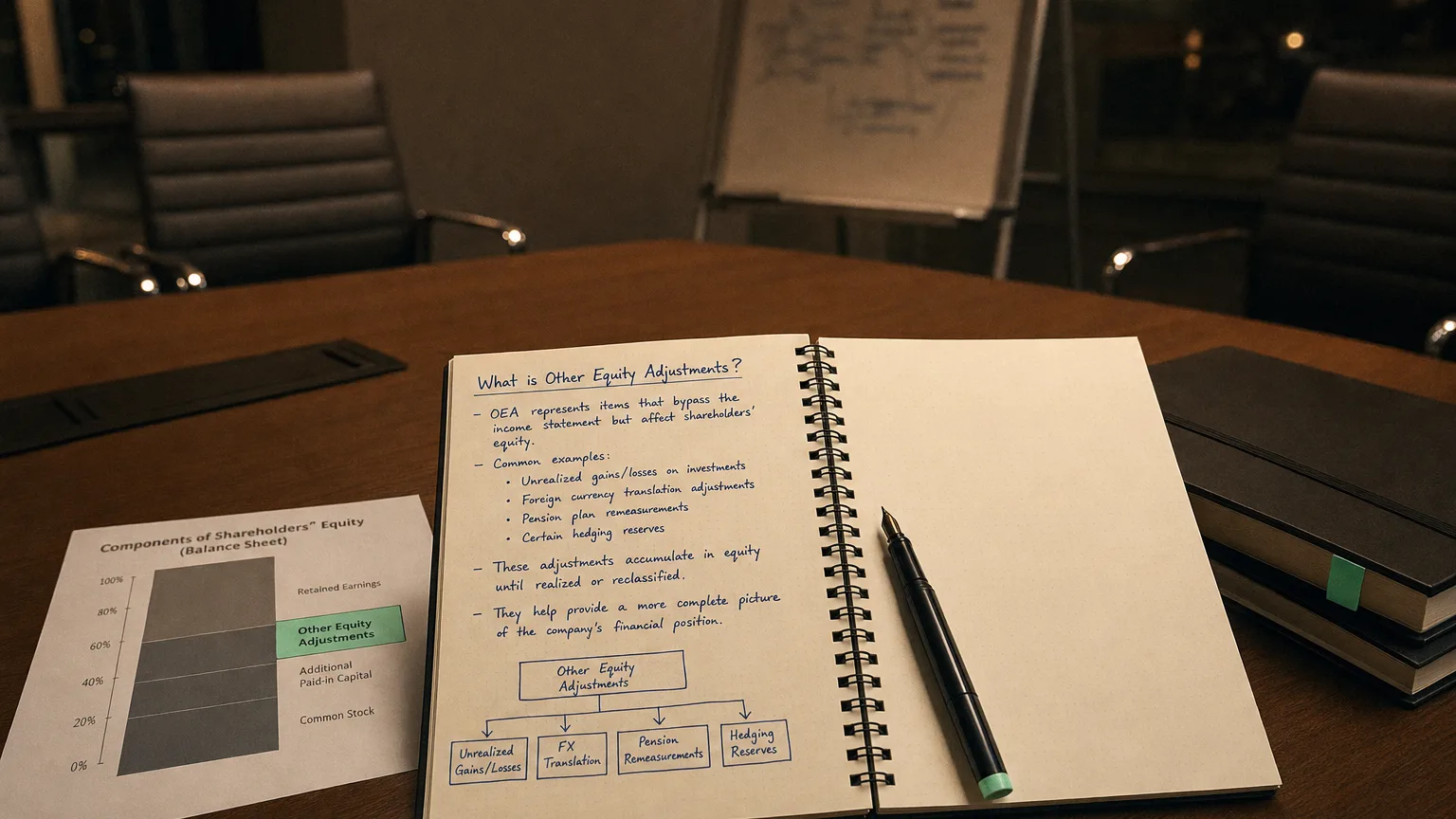

Other Equity Adjustments, often labeled as Accumulated Other Comprehensive Income (AOCI) in U.S. GAAP, represent a category of shareholders’ equity that captures certain gains and losses recorded directly in equity rather than through the income statement. In a typical balance sheet, this line is essentially a holding account for unrealized or special income and expense items. Its purpose is to segregate these items from regular retained earnings, providing clarity on what portion of equity came from such adjustments versus normal profits or owner contributions.

Common Components of Other Equity Adjustments

This equity category typically includes the accumulated gains or losses from specific sources, often referred to as Other Comprehensive Income (OCI) items:

- Foreign currency translation adjustments: Cumulative differences from converting the financial statements of foreign subsidiaries into the parent’s reporting currency.

- Unrealized gains or losses on certain financial instruments: Changes in the fair value of investments classified as ‘available-for-sale’ or ‘fair value through OCI’, and the effective portion of cash flow hedges.

- Pension remeasurement adjustments: Actuarial gains and losses related to defined benefit pension plans.

- Asset revaluation surplus (IFRS only): Upward revaluation gains on non-current assets like property, which are not permitted under U.S. GAAP.

“Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 2014 (2014)

How It Differs from Other Equity Accounts

vs. Retained Earnings

Retained Earnings accumulates a company’s net income over time. In contrast, Other Equity Adjustments (AOCI) accumulates items from Other Comprehensive Income. These items bypass net income entirely, so they never mix with retained earnings until they are realized.

vs. Additional Paid-In Capital (APIC)

APIC represents contributed capital from shareholders (money paid for stock above its par value). In contrast, Other Equity Adjustments arise from economic events and accounting adjustments (like market price changes or currency fluctuations), not from transactions with owners.

Treatment under IFRS vs. US GAAP

Both IFRS and US GAAP require these items to be reported separately from net income, though terminology can differ.

- U.S. GAAP: The accumulated balance is presented as Accumulated Other Comprehensive Income (AOCI), typically as a single line in the equity section. It does not permit upward revaluation of fixed assets.

- IFRS: The accumulated balance is often included under “Other Components of Equity” (OCE). IFRS allows for additional OCI items, most notably the asset revaluation surplus from revaluing property, plant, and equipment.

Impact on Net Income vs. Equity

Crucially, Other Equity Adjustments do not impact net income in the period they are first recorded. They affect only the shareholders’ equity section and the total comprehensive income figure.

The Holding Pen for Unrealized Items

AOCI acts like a holding pen. An unrealized loss on a security, for example, would reduce equity via OCI but would not appear as a loss on the income statement. Therefore, it does not reduce retained earnings. Only when the security is sold and the loss is ‘realized’ would the amount be reclassified from AOCI to net income, affecting retained earnings in that future period.