Other Equity Interest is a financial concept covered in this article. Miscellaneous Equity Components Not Classified Elsewhere

In the short run, the market is a voting machine. In the long run, it is a weighing machine.

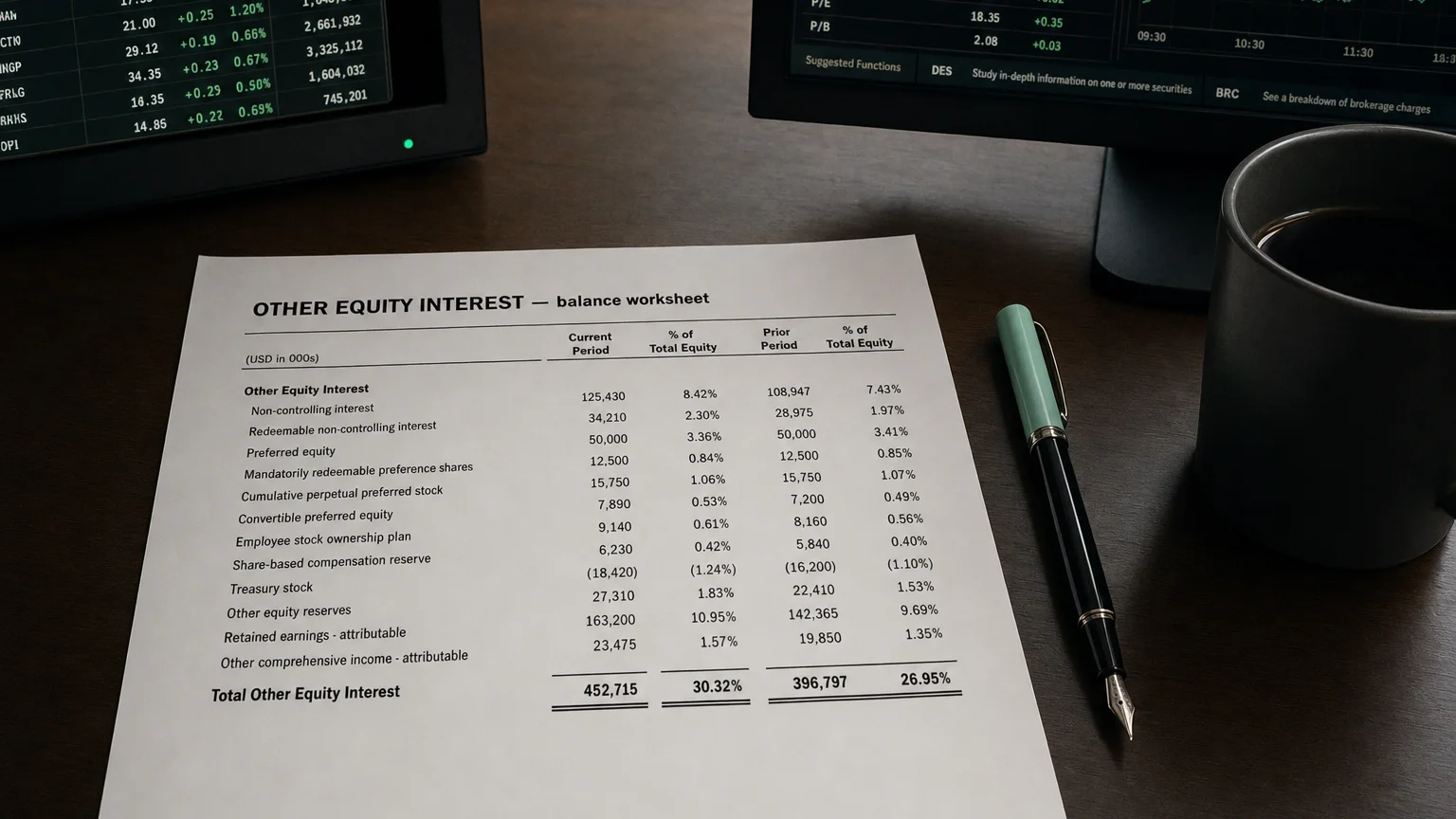

Other Equity Interest is a balance sheet line item in the shareholders’ equity section that captures equity-related amounts not fitting into standard categories such as common stock, preferred stock, additional paid-in capital, retained earnings, or treasury stock. It serves as a catch-all for various instruments, adjustments, or interests that represent ownership claims but require separate presentation due to their unique nature.

What Is Included in Other Equity Interest?

The exact composition varies by company and accounting framework, but common items include:

- Equity components of compound financial instruments (e.g., convertible debt equity portion)

- Certain hybrid instruments or perpetual securities classified as equity

- Equity issued in business combinations or complex transactions

- Non-controlling interests in some legacy or simplified presentations (though modern standards place NCI separately)

- Puttable instruments or obligations classified as equity under exceptions

- Equity reserves not shown elsewhere (e.g., statutory reserves in some jurisdictions)

- Adjustments related to employee share schemes or equity-settled payments

- Other ownership interests not fitting standard categories

It acts as a residual bucket to ensure total equity reconciles properly.

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.”

— Benjamin Graham, Author, The Intelligent Investor Security Analysis (1934)

Accounting Treatment

Under IFRS and US GAAP:

- Items must meet equity classification criteria (no obligation to deliver cash/other assets)

- Compound instruments split: liability at fair value, residual to equity (often in ‘Other Equity Interest’)

- IAS 32 governs classification—strict rules for puttable shares, perpetual instruments

- Changes in this line usually bypass income statement (directly to equity)

Movements disclosed in statement of changes in equity or notes.

Balance Sheet Presentation

Typically appears in shareholders’ equity as a separate line, often near the bottom before total equity.

Example presentation:

- Common stock

- Additional paid-in capital

- Retained earnings

- Treasury stock

- Accumulated other comprehensive income

- Other equity interest

- Total equity

Sign can be positive (equity contributions) or negative (certain obligations classified as equity).

Why Companies Use This Category

- Complex capital structures requiring separate tracking

- Issuance of hybrid/perpetual instruments

- Accounting for convertible securities or warrants

- Compliance with equity classification exceptions

- Consolidated entities with unusual ownership instruments

Provides transparency while maintaining clean primary categories.

Analytical Considerations

Analysts should:

- Review footnotes for composition—nature affects risk profile

- Assess if items are permanent equity or have redemption features

- Consider impact on total equity and leverage ratios

- Monitor changes for unusual transactions or dilutions

- Compare across peers (presentation varies)

Large or volatile ‘Other Equity Interest’ may signal complex financing or accounting choices.

Q · 01What is Other Equity Interest?+