Restricted Common Stock is a financial concept covered in this article. Common Shares Subject to Transfer or Forfeiture Restrictions

You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.

Restricted Common Stock refers to shares of common stock that are issued to individuals (typically employees, executives, or founders) but are subject to vesting conditions, transfer restrictions, or forfeiture risks. These shares are fully paid and issued but ‘restricted’ until certain conditions (e.g., continued employment or performance milestones) are met, at which point they become unrestricted.

What Is Restricted Common Stock?

Restricted Common Stock is actual common stock issued to recipients but encumbered by restrictions. Unlike stock options (which give a right to buy), restricted stock is granted outright—recipients own the shares immediately but risk forfeiture if conditions aren’t met.

Once vested, restrictions lapse and shares become freely transferable (subject to securities laws).

Also called ‘restricted stock awards’ (RSAs) to distinguish from restricted stock units (RSUs), which settle in shares later.

Common Restrictions

- Time-based vesting (e.g., 4-year cliff or graded)

- Performance-based vesting (milestones, stock price targets)

- Company repurchase right at cost/lower price upon termination

- Transfer prohibitions (no sale until vested)

- Legend on stock certificate noting restrictions

Early exercise options sometimes allow purchase before vesting, creating restricted stock.

“You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

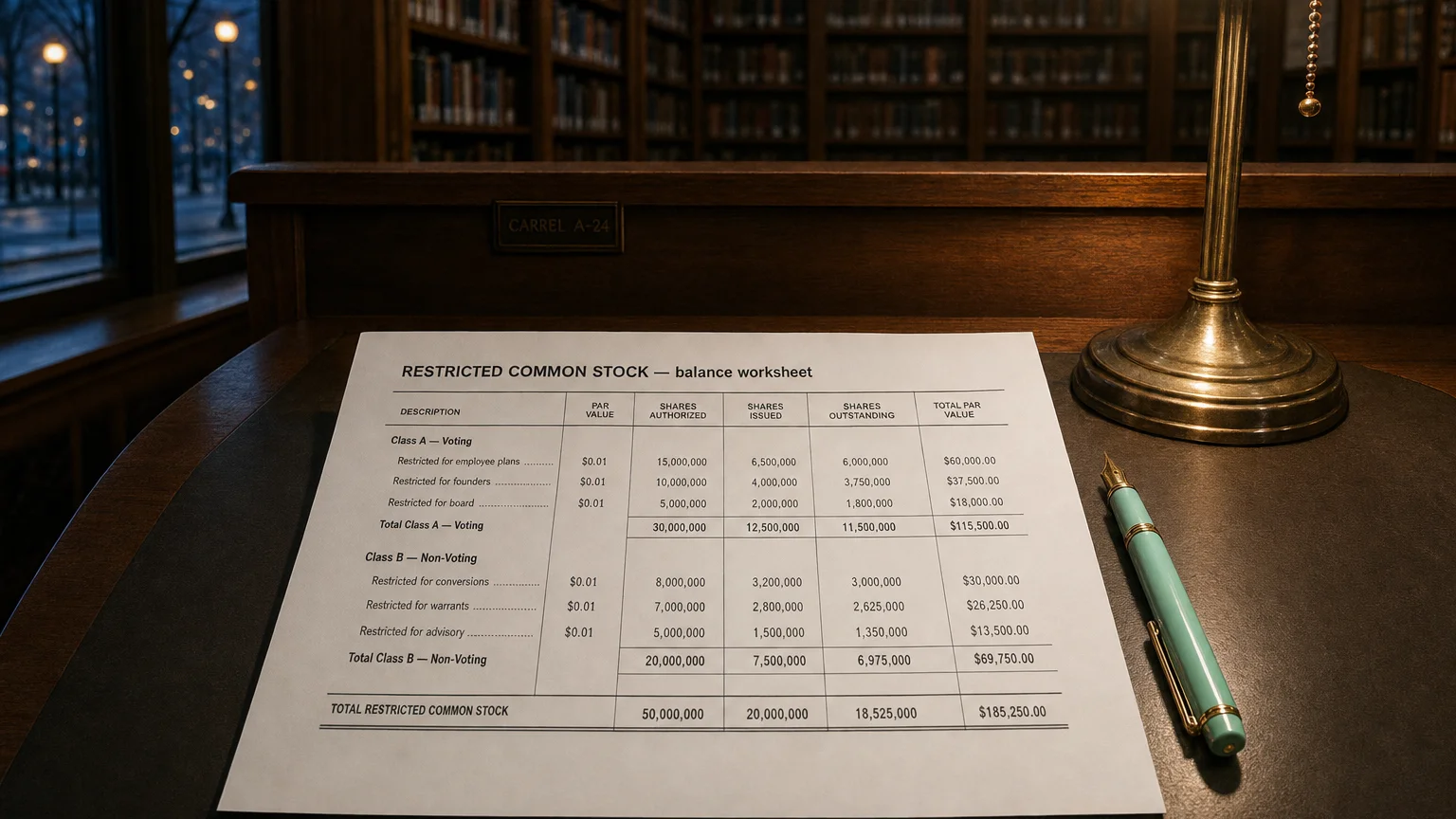

Accounting and Balance Sheet Impact

Treatment:

- Issued at grant: Credit Common Stock (par) + Additional Paid-In Capital

- Unvested shares often shown as contra-equity or disclosed separately

- Compensation expense recognized over vesting period (fair value at grant)

- Forfeited shares reverse expense and return to company (treasury or canceled)

ASC 718 (US GAAP) / IFRS 2 govern stock-based compensation accounting.

Presentation in Financial Statements

On balance sheet:

- Unvested restricted stock typically not deducted from equity (unlike treasury)

- Disclosed in footnotes: number of unvested shares, weighted-average grant price

- Sometimes shown as ‘Restricted Common Stock’ contra-equity line

- Vested shares fully in Common Stock equity

Statement of equity shows grants, vesting, forfeitures.

Why Companies Use Restricted Stock

- Align employee/executive interests with shareholders

- Retention tool (forfeiture on departure)

- Lower dilution vs. options (no exercise price premium)

- Immediate ownership motivates performance

- Tax advantages in some jurisdictions

Analytical Considerations

Restricted stock impacts analysis via:

- Future dilution upon vesting (increases outstanding shares)

- Non-cash compensation expense (reduces reported earnings)

- Retention strength (high unvested balances suggest lock-in)

- Burn rate and overhang metrics in equity compensation

- Tax implications for recipients (83(b) election in US)

Heavy reliance on restricted stock can signal aggressive compensation or dilution risk.

Q · 01What is Restricted Common Stock?+