Additional Paid-In Capital (APIC) Explained

Additional Paid-In Capital (APIC) is the premium above par that investors pay for new shares. Covers calculation, balance sheet placement, and dilution signals.

Overview

Additional Paid-In Capital (APIC) is the premium above par that investors pay for new shares. Covers calculation, balance sheet placement, and dilution signals.

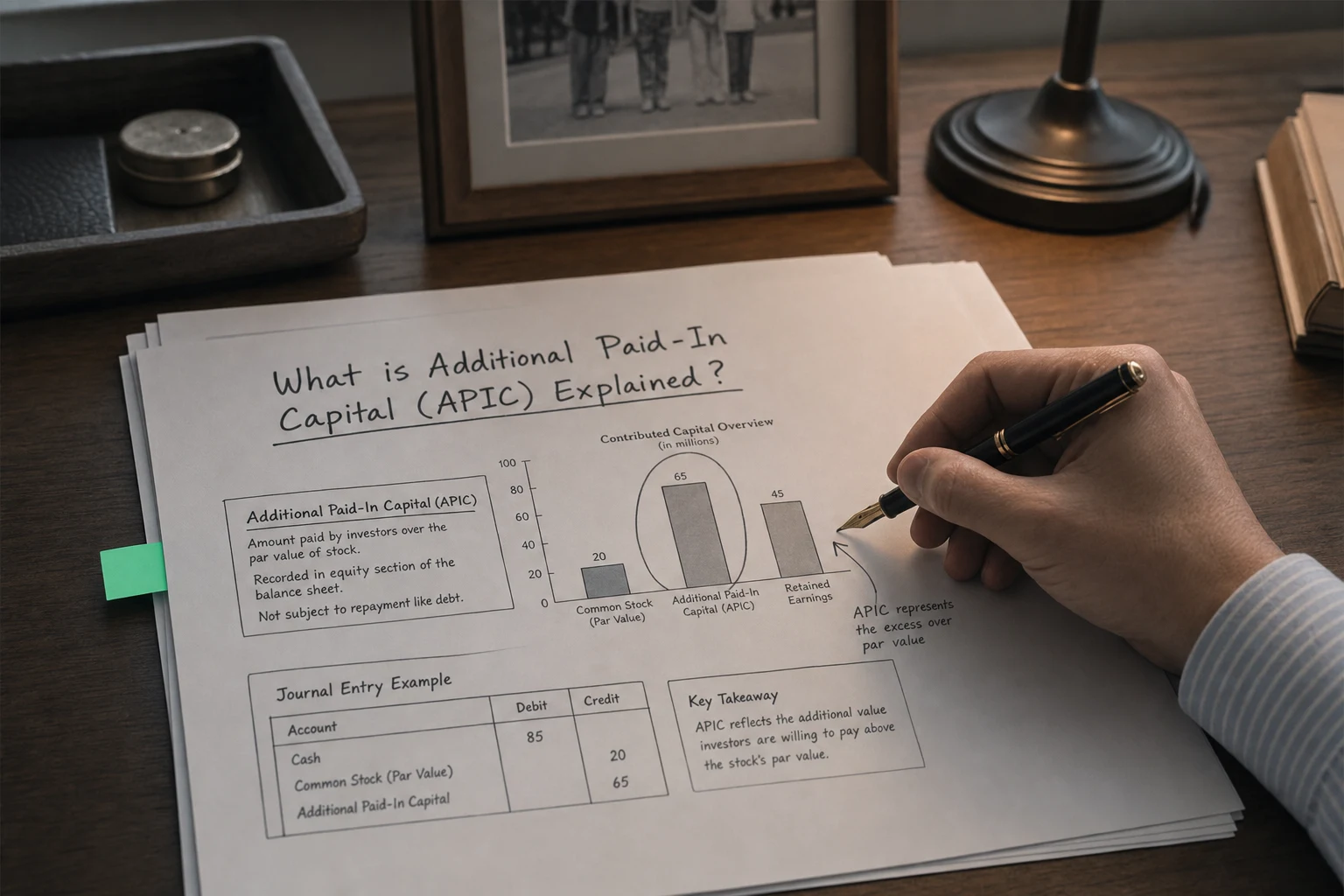

Additional Paid-In Capital (APIC) is the amount of money that shareholders have paid into a company in excess of the stock’s par valueinvestopedia.com. In simple terms, it’s the extra funds investors pay for shares above their nominal price (par value) when those shares are issued by the company. This is why APIC is often called “paid-in capital in excess of par” or share premiuminvestopedia.com. APIC is recorded in the shareholders’ equity section of the balance sheet as part of the company’s contributed capitalinvestopedia.com. It represents a portion of owners’ equity that comes from investors’ cash contributions, rather than from the company’s ongoing business operations.

- How Does Additional Paid-In Capital Arise?

APIC arises when a company issues stock to investors at a price above the stock’s par value. Par value is a nominal dollar amount assigned to each share (often set very low, such as $0.01 per share, to avoid legal issues)investopedia.com. Anytime investors pay more than this nominal par value for a company’s stock, the excess amount is recorded as additional paid-in capital. For example, if a company issues shares with a par value of $1 but investors pay $11 per share in an initial offering, the company would record $1 per share as common stock (par value) and the remaining $10 per share as additional paid-in capital. In this scenario, issuing 1 million shares would generate $11 million in total, recorded as $1 million under common stock and $10 million under APICinvestopedia.com. This APIC reflects the premium investors are willing to pay above the stock’s face value to own a piece of the companycorporatefinanceinstitute.com.

It’s important to note that APIC is generally created through primary market transactions (such as initial public offerings or follow-on stock offerings) where investors buy shares directly from the companycorporatefinanceinstitute.com. Transactions in the secondary market (investors buying from other investors after the stock is publicly traded) do not affect a company’s APIC because the company isn’t receiving any new funds in those tradesinvestopedia.com. Once shares have been issued, the APIC amount remains fixed on the balance sheet for those shares – it does not fluctuate with the market price of the stock. In other words, after the stock issuance, changes in stock price or trading activity don’t change the APIC account; APIC is a permanent entry in equity reflecting the original capital paid in above parqubit.capitalqubit.capital.

- Placement on the Balance Sheet

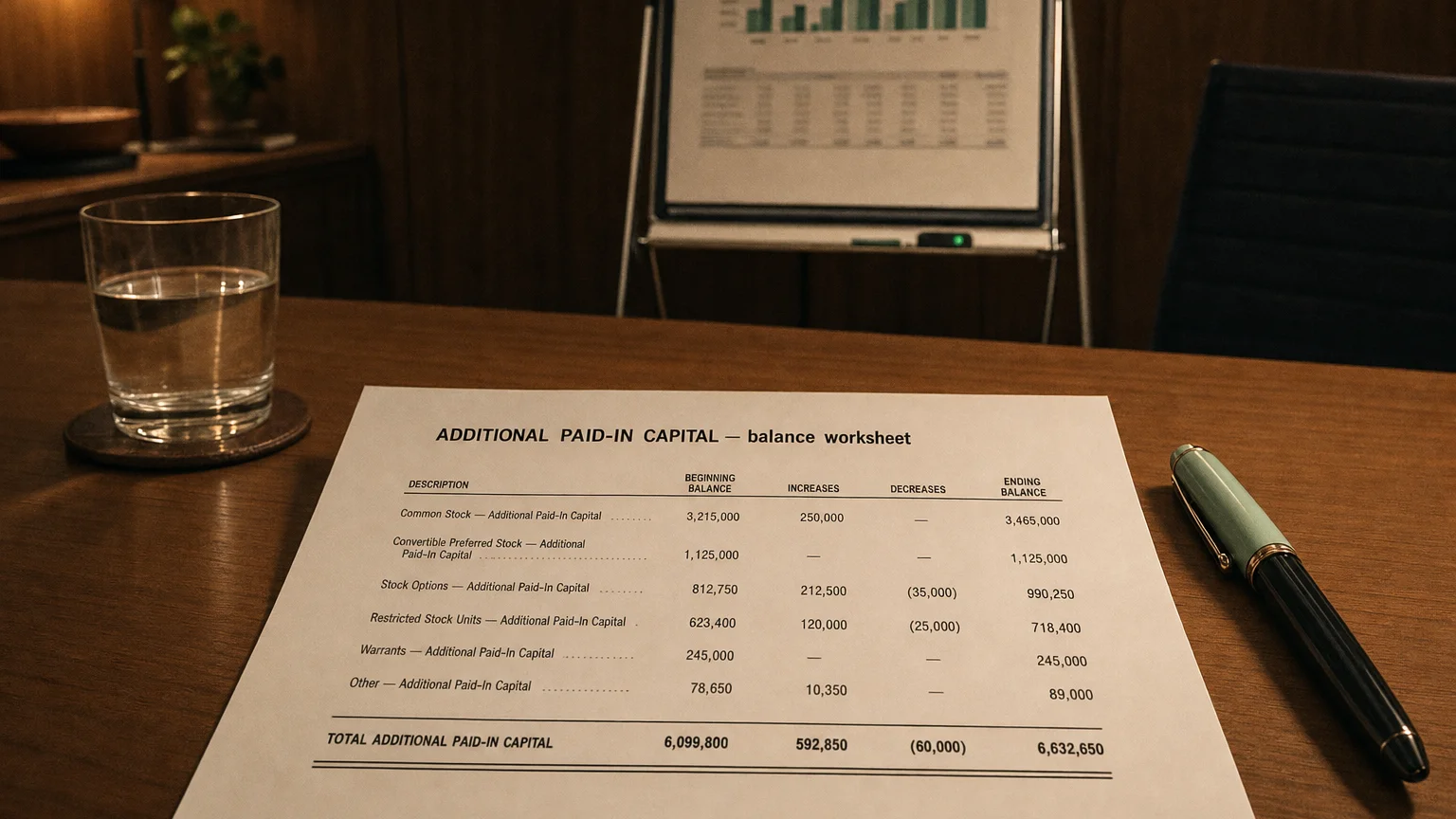

Figure: An excerpt from Facebook’s consolidated balance sheet highlighting the Stockholders’ Equity section, where Additional paid-in capital is listed (as a separate line item below Common stock). This illustrates how APIC appears on an actual balance sheet.

On a balance sheet, additional paid-in capital is listed in the stockholders’ (shareholders’) equity section. It usually appears as a distinct line item, typically right below the line for Common Stock (which is recorded at par value). The common stock line reflects the par value of issued shares, while the APIC line shows the extra amount shareholders paid over that par valueinvestopedia.comthetradinganalyst.com. Together, the common stock and APIC accounts sum up to the total paid-in (contributed) capital from shareholders. For instance, in the figure above, you can see “Common stock” followed by “Additional paid-in capital,” each with their respective dollar amounts – this is a standard presentation. APIC is part of the company’s equity and, along with retained earnings, it is often one of the largest components of equity for many companiescorporatefinanceinstitute.com. In fact, immediately after a company’s IPO or a major stock issuance, APIC typically makes up a large portion of total equity (since the company may not have built up much retained earnings at that point)corporatefinanceinstitute.com.

- APIC vs. Common Stock vs. Retained Earnings

Although APIC, common stock, and retained earnings all reside in the shareholders’ equity section, they represent different things:

Common Stock (Par Value): This represents the legal capital of the company from issued shares, calculated as the par value per share multiplied by the number of shares issued. The common stock account is usually a relatively small amount because par values are often set very low (for example, a penny per share)investopedia.com. It appears on the balance sheet under equity at the par value total, indicating the base value of what shareholders have invested.

Additional Paid-In Capital (APIC): This is the amount shareholders have paid above the par value of the stock. It’s the excess or premium investors contributed when they bought shares from the company. APIC is recorded as a separate equity line item (e.g. “Capital in excess of par” or “Share premium”) and remains fixed once the shares are issuedthetradinganalyst.com. A high APIC balance means the company was able to issue shares at prices far above the nominal par value, reflecting that investors were willing to put in substantial capital beyond the stock’s face value. Together, the common stock and APIC accounts represent the total contributed capital from shareholders’ investments in the company’s stockinvestopedia.com.

Retained Earnings: In contrast to the above two (which come from shareholder contributions), retained earnings are the accumulated net profits that the company has earned over time and kept (retained) in the business instead of paying out as dividends. Retained earnings increase with each year’s profits (or decrease with losses or dividend payouts) and indicate the portion of equity that was generated by the company’s own operations. While APIC and common stock tell us how much money shareholders have put into the company, retained earnings tell us how much wealth the company itself has created and retained. Both APIC and retained earnings contribute to total equity, but they “tell different stories”: APIC reflects investor capital inflows and confidence in the company’s potential, whereas retained earnings demonstrate the company’s ability to generate and accumulate profits through its business activitiesptcpas.com.

In summary, common stock + APIC = total paid-in capital (funds raised from shareholders), whereas retained earnings = internally generated equity (net income kept in the company). All are important parts of equity but come from different sources and have different implications.

- Why APIC Matters in Financial Reporting and to Stakeholders

APIC may just look like a line on the balance sheet, but it has important significance for a company’s financial reporting and for its stakeholders:

Indicator of Investor Confidence: A large APIC balance implies that investors were willing to pay a premium for the company’s shares, signaling strong market confidence in the company’s value and future prospectsthetradinganalyst.comthetradinganalyst.com. For example, if a company’s stock was issued well above par value, stakeholders can infer that at the time of issuance, investors had high expectations for the company. APIC essentially captures the collective vote of confidence (in dollar terms) that shareholders gave by paying more than the minimum price for the stock. This can be reassuring to current investors and can attract further investor interest, as it reflects a history of the company being able to raise funds on favorable termsptcpas.com.

Strengthening the Capital Structure: Additional paid-in capital contributes to a company’s permanent capital base. Because it comes from equity issuances, it does not create any debt or repayment obligation for the company. This strengthens the balance sheet: APIC (and equity in general) provides a cushion against losses since it can absorb unexpected deficits without forcing the company into defaultinvestopedia.com. Creditors and analysts often view a healthy APIC and equity level as a positive sign, as it lowers the company’s leverage (debt-to-equity ratio) and thus financial risk. In financial reporting, APIC combined with other equity is a measure of the company’s net worth which can be used to evaluate solvency and stability. In fact, the funds from APIC can be seen as “patient capital” – money that stays in the company to support growth and operations, unlike loans which must be paid back with interestptcpas.comptcpas.com.

Financial Flexibility and Growth Funding: From management’s perspective, money raised under APIC is an attractive way to finance the business. It brings in cash without incurring debt, interest costs, or obligations to repayinvestopedia.com. The company can use the cash from issuing stock for any strategic needs – such as expanding operations, investing in R&D, acquiring other businesses, or bolstering working capital – all without the burden of monthly payments or collateral that comes with borrowingptcpas.comptcpas.com. In other words, APIC-funded equity provides financial flexibility. Stakeholders benefit because the company can pursue growth opportunities or weather downturns with this extra capital buffer. A robust APIC and equity position can make a company more resilient during economic difficulties, as it has a stronger equity cushion to absorb losses and less pressure from creditorsthetradinganalyst.com.

Transparency and Insight: In financial reporting, clearly disclosing APIC helps stakeholders understand how the company’s equity has been built up. It allows investors to see how much capital came from shareholders versus how much was earned and retained from operations. For instance, comparing APIC to retained earnings gives insight into whether the company’s growth has been funded more by external equity investments or by internal profitsqubit.capital. Significant changes in APIC from one period to another can also indicate major events like new stock issuance or mergers (since issuing new shares at a price above par will boost APIC). This information is valuable to shareholders and prospective investors for assessing dilution and the company’s financing decisions. Proper accounting of APIC (separating it from other equity accounts) also ensures transparency and compliance with reporting standards, so stakeholders can trust the equity section of the balance sheetptcpas.com.

In summary, additional paid-in capital is more than just an accounting figure – it represents shareholders’ collective investment above a stock’s nominal value and serves as a key component of equity that bolsters the company’s financial strength. Whether one is an investor analyzing a firm’s stability, a creditor evaluating risk, or a company executive planning for growth, APIC provides insight into how much capital the company has raised from its owners and how confidently the market has valued the company’s shares. By strengthening the equity base without adding debt, APIC plays an important role in a company’s capital structure and its ability to fund operations and expansionthetradinganalyst.cominvestopedia.com. It matters to stakeholders because it reflects both the financial foundation and the market’s faith in the company’s potential, which are critical factors in long-term success.

Sources:

Investopedia – Definition and explanation of Additional Paid-In Capitalinvestopedia.cominvestopedia.com

Corporate Finance Institute – APIC as part of shareholders’ equity and its calculationcorporatefinanceinstitute.comcorporatefinanceinstitute.com

Investopedia – Example of how APIC is calculated during a stock issuanceinvestopedia.com

Investopedia – Recording of common stock and APIC on the balance sheet (shareholders’ equity section)investopedia.com

Patten & Company CPAs – APIC vs. Retained Earnings (distinguishing contributed capital from earned capital)ptcpas.com

Corporate Finance Institute – APIC and retained earnings as major components of equity, especially post-IPOcorporatefinanceinstitute.com

TheTradingAnalyst – Significance of a high APIC (investor confidence and strengthening the balance sheet)thetradinganalyst.comthetradinganalyst.com

Investopedia – Benefits of APIC for a company’s capital structure (no collateral or fixed payments required)