Capital stock is the total shares of ownership a company has issued to shareholders, comprising common and preferred stock. It is recorded at par value in the shareholders' equity section of the balance sheet, with any premium above par captured in additional paid-in capital.

The intelligent investor is a realist who sells to optimists and buys from pessimists.

Capital stock represents the total shares of ownership in a company, encompassing both common and preferred stock. It is essentially the share capital that the company has issued to shareholders in exchange for funding. Capital stock is listed in the shareholders’ equity section of the balance sheet, reflecting the owners’ stake in the company. The amount recorded is typically based on the par value (a nominal value) of the issued shares, not their market price.

Components of Capital Stock: Common vs. Preferred Shares

Capital stock can consist of different classes of shares, primarily common and preferred stock, each with distinct characteristics:

- Common Stock: These are the ordinary shares representing basic ownership. Common shareholders typically have voting rights and a residual claim on assets, meaning they are paid last in a liquidation. This higher risk is offset by the potential for greater returns through capital appreciation.

- Preferred Stock: This is a special class of stock that usually has no voting rights but gives shareholders preferential treatment. They are entitled to a fixed dividend that must be paid before any common stock dividends and have priority in claims on assets during liquidation. It is often considered a hybrid of equity and debt.

“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

— Benjamin Graham, Author, The Intelligent Investor The Intelligent Investor (1949)

Purpose and Implications of Capital Stock

Issuing capital stock is a primary way companies raise money and structure ownership:

- Raising Capital: It allows a company to receive cash to fund operations or growth without incurring debt or needing to make interest payments.

- No Fixed Obligations: Unlike debt, capital stock does not require mandatory payments. Dividends on common stock are optional, providing the company with financial flexibility.

- Ownership and Control: Each share represents fractional ownership. Issuing new shares spreads ownership among more investors, which dilutes the ownership percentage and control of existing shareholders.

- Dilution of Value: Issuing many new shares can also dilute value on a per-share basis, as earnings and assets are spread across a larger number of shares, potentially reducing metrics like earnings per share.

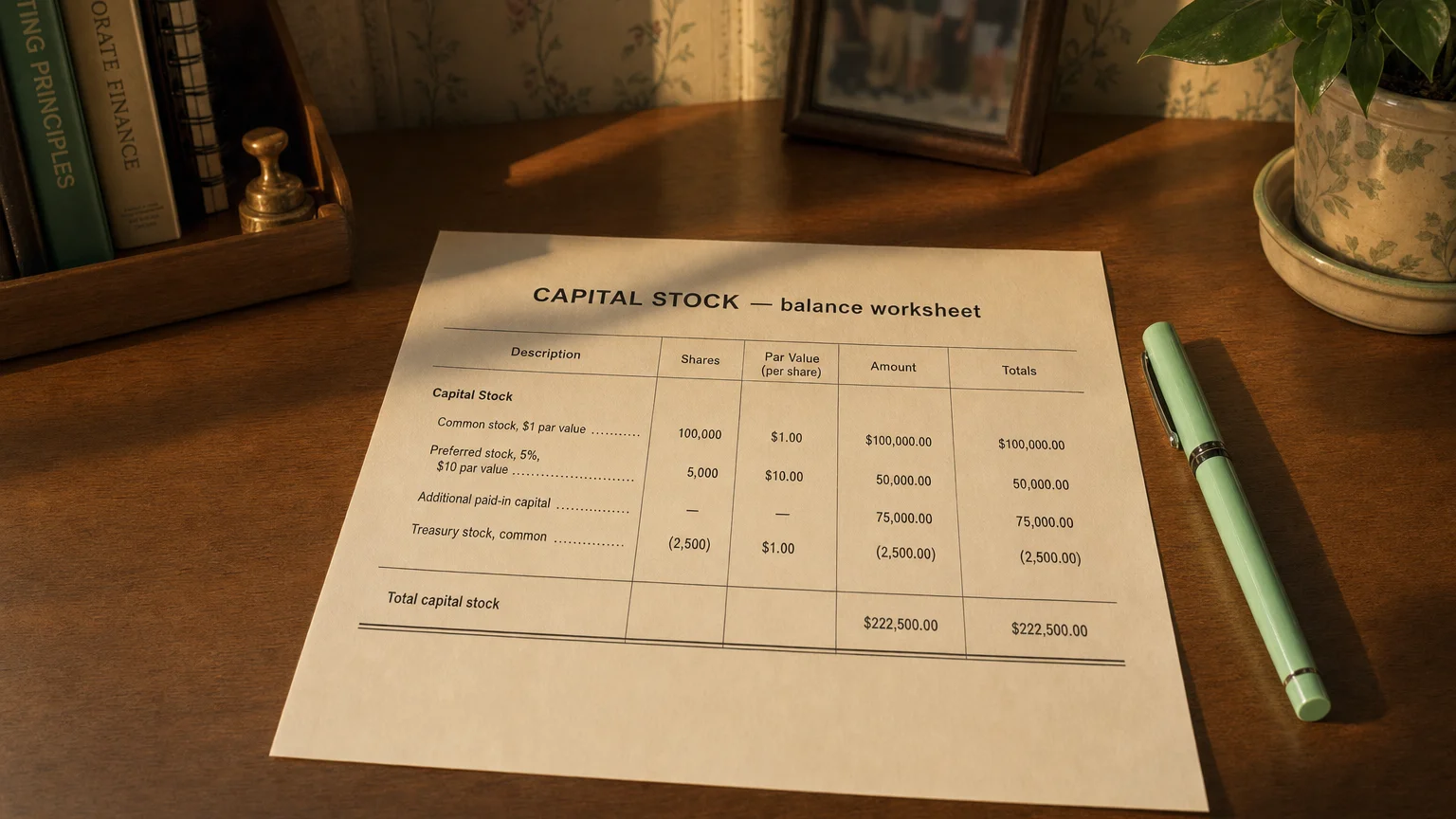

Capital Stock in the Shareholders’ Equity Section

On the balance sheet, capital stock appears at the top of the shareholders’ equity section, broken down into its key parts:

- Preferred and Common Stock Accounts: Each class of stock is listed separately, recorded at its par value multiplied by the number of shares issued. The number of authorized, issued, and outstanding shares is often disclosed here.

- Additional Paid-In Capital (APIC): This account, also known as share premium, represents the total amount investors paid above the par value of the stock. The Capital Stock account plus APIC equals the total cash raised from issuing shares.

- Retained Earnings: This is listed separately below the contributed capital accounts (Stock and APIC). It represents the cumulative profits earned by the company, not capital contributed by shareholders.

Simplified Equity Section

A company sells 2 million shares at 1 par value. The equity section would show:

- **Common Stock (2,000,000

- Additional Paid-In Capital: $18,000,000

- Retained Earnings: (e.g., $5,000,000)

- Total Shareholders’ Equity: $25,000,000

Capital Stock vs. APIC vs. Retained Earnings

Distinguishing Equity Components

All three are part of shareholders’ equity but have different origins:

- Capital Stock: Represents contributed capital recorded at the par value of issued shares.

- Additional Paid-In Capital (APIC): Represents contributed capital from the premium paid by investors above the par value.

- Retained Earnings: Represents earned capital from the company’s accumulated, reinvested profits.

Q · 01What is the difference between common and preferred stock?+

Q · 02How is capital stock recorded on the balance sheet?+

Q · 03What does issuing capital stock mean for existing investors?+