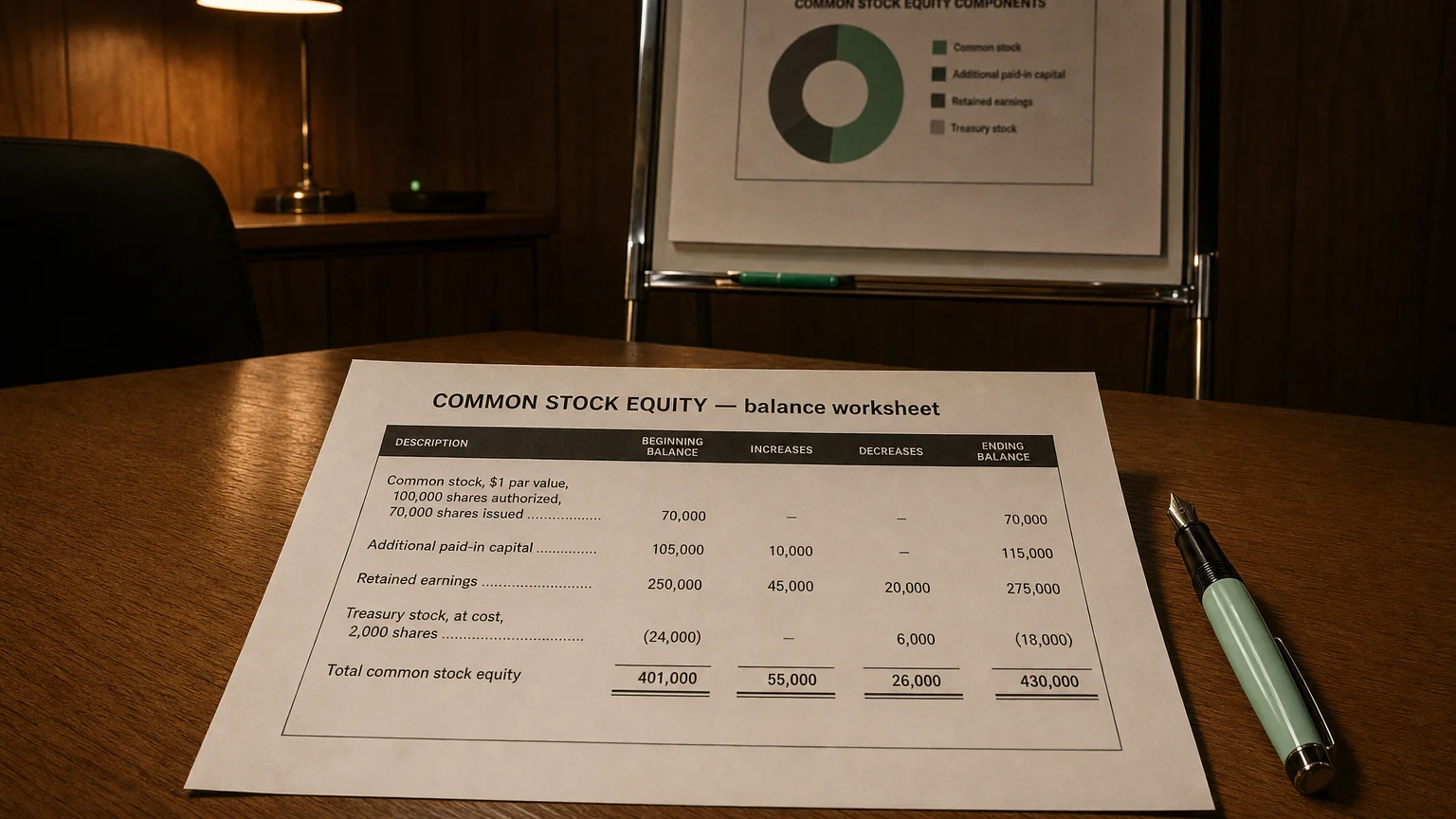

Common stock equity is the residual ownership interest of common shareholders after all liabilities and preferred stock are deducted from total assets. It comprises common stock at par, additional paid-in capital, retained earnings, AOCI, and less treasury stock.

The intelligent investor is a realist who sells to optimists and buys from pessimists.

Common stock equity (often called common shareholders’ equity) represents the ownership interest of common shareholders in a company. It is essentially the portion of the company’s net assets that belongs to common stockholders after all liabilities (and any senior equity like preferred stock) are accounted for. In simple terms, common equity includes all value invested by common shareholders (share capital) plus any profits retained in the business. Common stockholders’ equity is often described as a residual claim on assets because common shareholders are last in line - they only receive value after all debts and preferred shareholders’ claims are satisfied. This higher risk comes with the benefit of full voting rights and potential for greater long-term returns.

Components of Common Stock Equity

“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

— Benjamin Graham, Author, The Intelligent Investor The Intelligent Investor (1949)

Common stock equity on the balance sheet is comprised of several components that together reflect the total interest of common shareholders:

- Common Stock (Par Value): The share capital recorded at the par (or stated) value of each share multiplied by the number of shares issued. This represents the legal capital, not the market value. For example, if a company issues 1 million common shares with a 1 million.

- Additional Paid-In Capital (APIC): Also known as share premium, this is the amount investors paid for shares above their par value. If a share with a 10, 9 goes to APIC.

- Retained Earnings: The accumulated profits that the company has reinvested in the business rather than paid out as dividends. This account grows with net income and shrinks with net losses or dividend payments, often becoming the largest component of common equity over time.

- Accumulated Other Comprehensive Income (AOCI): Includes accumulated gains and losses not captured on the income statement, such as unrealized gains on securities or foreign currency translation adjustments. It is recorded directly in equity.

- Treasury Stock: A contra-equity (negative) account representing the cost of shares the company has repurchased. It reduces total common stock equity. For example, if a company buys back 100,000.

Role in the Overall Equity Section

On the balance sheet, the equity section shows financing from owners. Common stock equity is central to this section. Following the accounting equation (Assets = Liabilities + Equity), it is the residual interest after all liabilities and preferred equity are accounted for.

Formula:

This residual nature means common equity is the company’s net worth from the perspective of its common shareholders. It serves as a cushion for creditors, as a strong common equity base can absorb losses. If common equity is negative, it signals balance sheet insolvency, a serious red flag.

Significance to Investors

Common stock equity is highly significant to investors for several reasons:

- Indicator of Value: Investors compare common equity (book value) to the company’s market value to gauge valuation. A consistently growing common equity often signals a healthy company.

- Return on Equity (ROE): Investors use common equity to assess profitability. Return on Common Equity (ROCE) is a more precise measure when preferred stock exists:

- Book Value per Share: This metric tells an investor how much net asset value each share represents. It is calculated as:

- Assessment of Capital Structure: The proportion of common equity to debt helps investors evaluate financial risk using ratios like the debt-to-equity ratio.

- Dividend Capacity: Retained earnings, a key part of common equity, show the cumulative profits available for reinvestment or future dividend payments.

Common vs. Total vs. Preferred Equity

It’s important to distinguish between these equity classifications:

- Total Equity: The sum of all equity accounts, including both common and preferred stock. If a company has no preferred stock, Total Equity is the same as Common Equity.

- Preferred Equity: Represents a class of ownership with a fixed dividend and priority over common stock in payments and liquidation. Preferred shareholders typically do not have voting rights and their upside potential is limited.

- Common Equity: This is subordinate to preferred equity. Common shareholders are paid only after all obligations to creditors and preferred shareholders are met. They bear more risk but have unlimited upside potential and voting rights.

The Pecking Order

In a liquidation, the order of payment is: 1) Creditors (debt holders), 2) Preferred Shareholders, and 3) Common Shareholders. This makes common equity the true residual claim on the company’s assets.

Q · 01What components make up common stock equity?+

Q · 02How is common equity different from total equity?+

Q · 03Why do investors track return on common equity?+