An essential guide to the cumulative profits a company has reinvested in its business, and its role as a key component of shareholders' equity.

The stock market is filled with individuals who know the price of everything but the value of nothing.

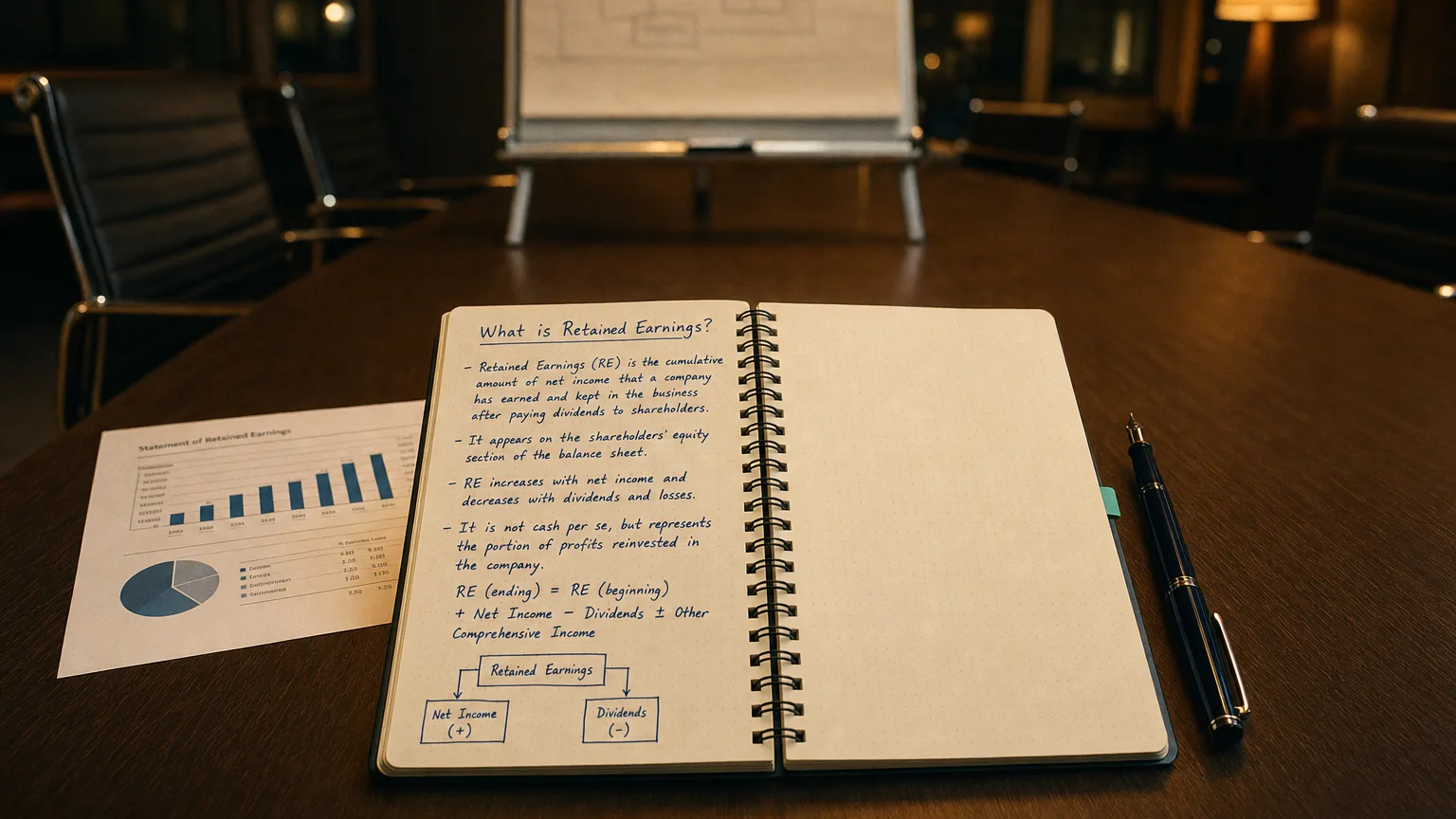

Retained earnings are the cumulative net profits that a company has earned and kept in the business after paying out any dividends to shareholders. In other words, it is the total amount of earnings retained since the company’s inception, as opposed to being distributed to owners. These retained funds are often reinvested into the business or held as a reserve for future use. “Retained” simply means the earnings were not paid out – they were kept in the company. Because retained earnings accumulate over time, you can think of this balance as a running total of profits that the company has retained in the business rather than paid out.

It’s important to note that retained earnings can be negative if a company has incurred losses or paid out more in dividends than it has earned. A negative balance of retained earnings is called an accumulated deficit. This situation might occur for a startup in its early years or any company that has experienced sustained net losses or exceptionally large dividend payouts. In summary, retained earnings (sometimes called earnings surplus or retained surplus) represent the portion of profit that remains in the company after all expenses, obligations, and shareholder payouts have been accounted for.

How Are Retained Earnings Calculated?

Retained earnings are updated each accounting period (e.g. monthly, quarterly, or annually) using a simple formula. The calculation starts with the prior period’s retained earnings, adds the current period’s net income (or subtracts a net loss), and then subtracts any dividends declared for that period. The basic formula for retained earnings is:

Ending Retained Earnings = Beginning Retained Earnings + Net Income – Dividends

This formula captures how profits and shareholder distributions affect the retained earnings balance. To compute retained earnings for a given period, follow these steps:

-

Start with Beginning Retained Earnings: Determine the retained earnings balance at the start of the period. This is usually the ending retained earnings from the previous period’s balance sheet. For a newly formed company, the beginning retained earnings would be $0 (since no past earnings exist).

-

Add Net Income (or Subtract Net Loss): Add the company’s net income for the current period (or subtract the net loss if the period was unprofitable). Net income is taken from the income statement and represents the profit after all expenses and taxes. If the company earned a profit, retained earnings will increase by that amount; if the company had a loss, retained earnings will decrease.

-

Subtract Dividends Paid Out: Subtract any dividends the company paid to its shareholders during the period. Dividends can be paid in cash or in additional stock. Cash dividends reduce the retained earnings because they are a direct payout of accumulated profits to shareholders. Stock dividends also reduce retained earnings, but instead of cash leaving the company, a portion of retained earnings is reclassified into paid-in capital accounts (this doesn’t affect total equity, but it does decrease the retained earnings balance). If no dividends were distributed, then this step has no effect on retained earnings.

After these steps, the result is the ending retained earnings for that period. This ending balance will be reported on the balance sheet and will carry over as the beginning retained earnings for the next period. Because of this running total, retained earnings provide a link between the income statement and the balance sheet over time.

Where Do Retained Earnings Appear on the Balance Sheet?

Retained earnings (highlighted) shown as a line item under the shareholders’ equity section of a balance sheet.

In financial statements, retained earnings are reported in the shareholders’ equity section of the balance sheet. They typically appear below contributed capital (common stock, additional paid-in capital) and above other equity items. In the figure above, for example, the retained earnings line is highlighted as part of shareholders’ equity. This placement reflects the nature of retained earnings: they represent equity attributable to the owners of the company. In essence, retained earnings are the portion of shareholders’ equity that was earned through company operations, rather than from issuing stock.

It’s important to clarify that retained earnings are not a physical stash of cash or a separate asset — they are an equity account. On the balance sheet, assets = liabilities + equity, and retained earnings fall on the equity side of this equation. Retained earnings are categorized as equity, not as an asset or liability. However, having high retained earnings can strengthen a company’s ability to acquire assets or pay dividends, since it indicates past profitability that has been retained in the business. The dollar amount of retained earnings reflects profits that have been reinvested or held in reserve; those funds may be deployed into assets like inventory, equipment, or other investments, but until they are used, they remain as part of equity on the balance sheet.

Typically, on a balance sheet you will see “Retained Earnings” listed under equity, often following other equity accounts. Some companies also prepare a separate Statement of Retained Earnings (or Statement of Shareholders’ Equity) that details the changes in retained earnings during the period (starting balance, plus net income, minus dividends, resulting in ending balance). This statement provides additional insight into how the retained earnings balance evolved, but the ending figure ultimately appears on the balance sheet itself.

Why Retained Earnings Matter (Significance for Companies)

Retained earnings provide insight into a company’s financial health and its strategy for using profits. Here are a few reasons why retained earnings are significant:

-

Reinvestment and Growth: Retained earnings are a primary source of internal financing for companies. Instead of raising new capital, a firm can use retained earnings to fund new projects, purchase equipment, invest in research and development, hire more staff, or expand operations. For example, a growing tech startup might retain most of its earnings to fuel rapid expansion, resulting in a growing retained earnings balance over time. Using retained profits for reinvestment can help a company generate even more earnings in the future, ideally creating a positive cycle of growth.

-

Debt Reduction and Reserves: Companies might also retain earnings to pay down debt obligations or build up a cash reserve. Paying off high-interest debt with retained earnings can strengthen the balance sheet and save on interest costs in the long run. Additionally, a healthy retained earnings balance can provide a cushion for economic downturns or unexpected expenses, improving the company’s financial stability. Firms in stable or cyclical industries might retain more earnings as a safeguard against tough times.

-

Dividend Policy and Shareholder Value: The level of retained earnings reflects a company’s dividend policy and stage of maturity. A growth-focused company often pays little to no dividends, preferring to reinvest profits, which leads to higher retained earnings accumulation. In contrast, a mature company with fewer high-return growth opportunities might distribute a larger portion of its profits as dividends, resulting in slower growth of retained earnings or even a drawdown of retained earnings over time. Neither approach is inherently good or bad – it’s a strategic decision. Shareholders in growth companies expect the retained earnings to be used to produce higher future returns, whereas shareholders in mature companies might prioritize regular dividends. Most companies strike a balance, paying some dividends while keeping the remainder of earnings for reinvestment.

-

Indicator of Cumulative Profitability: Retained earnings serve as an indicator of a company’s cumulative profitability and how those profits have been managed. Investors and analysts look at retained earnings to understand how much money a company has effectively saved over its lifetime after all obligations and shareholder payments. Consistently growing retained earnings indicate that a company has been profitable and prudent in managing its profits. On the other hand, if retained earnings are consistently low or not growing, it could mean the company is distributing most profits as dividends, or it may be struggling to grow its profits. If retained earnings are negative (accumulated deficit), it’s a warning sign that the company has experienced substantial losses or paid out more than it earned historically.

-

Link Between Financial Statements: Retained earnings provide a crucial link between the income statement and the balance sheet. Net income from the income statement (which reflects performance over a period) flows into retained earnings on the balance sheet (which reflects the cumulative outcome over time). This link means that retained earnings connect a company’s profitability with its financial position. A high retained earnings balance by itself isn’t necessarily good or bad – what matters is how those funds are utilized. Investors often evaluate how effectively a company uses retained earnings to generate additional profit or shareholder value. For instance, one metric (retained earnings to market value) compares how each dollar of retained earnings translates into market value growth. In general, retained earnings offer internally generated capital, which is usually the cheapest source of funding for a company’s activities.

In summary, retained earnings matter because they show how much of the company’s profits have been kept in the business and how those funds might enable future opportunities. Companies with strong retained earnings have the flexibility to invest in themselves, reduce debt, or return value to shareholders. Meanwhile, analyzing retained earnings in context (industry norms, company life-cycle, and alternative uses of cash) helps stakeholders understand whether the company’s retention of earnings is contributing to its long-term success.

Example: Retained Earnings Evolving Over Time

To illustrate how retained earnings work, let’s consider a simple example of a hypothetical company over several periods:

-

Year 1: The company is new and starts with $0 retained earnings (no prior profits). In its first year, it earns $50,000 in net income and does not pay any dividends. By the end of Year 1, retained earnings equal $50,000. This comes directly from the formula: Beginning RE $0 + Net Income $50,000 – Dividends $0 = Ending RE $50,000. All $50,000 of the year’s profit is retained in the business (since none was paid out to shareholders).

-

Year 2: The company has a beginning retained earnings of $50,000 (carried over from Year 1). In Year 2, it earns $30,000 in net income and the board decides to pay $10,000 in dividends to shareholders. Using the formula: Beginning RE $50,000 + Net Income $30,000 – Dividends $10,000 = Ending RE $70,000. The retained earnings grow to $70,000 by the end of Year 2. In this period, the company retained a portion of its profits after sharing some earnings with shareholders. (We can also see that the $10,000 dividend equals the difference between profit and the increase in retained earnings: $30,000 profit led to a $20,000 increase in retained earnings, meaning $10,000 was paid out as dividends.)

-

Year 3: The company starts Year 3 with retained earnings of $70,000. Suppose this year the company experiences a small net loss of $5,000 (perhaps due to an unusual expense or downturn) and pays no dividends. Applying the formula: Beginning RE $70,000 + Net Loss ($5,000) – Dividends $0 = Ending RE $65,000. The retained earnings decrease to $65,000 because the loss for the year has absorbed some of the previously retained profits. This highlights that retained earnings will fall if a company has a net loss (or if dividends exceed the period’s net income). Even after the loss, the company still has positive retained earnings overall, since over its lifetime it has accumulated $65,000 of net profits that remain invested in the company.

This simple timeline shows how retained earnings accumulate and change: they increase with profits and decrease when the company incurs losses or distributes cash to shareholders. Each year’s ending retained earnings becomes the starting balance for the next year, so retained earnings capture the history of earnings retention in the business. A steadily rising retained earnings balance over multiple periods generally signals that a company is profitable and reinvesting its earnings, whereas fluctuations can indicate dividend payments, periods of losses, or changes in financial strategy.

Key Takeaway: Retained earnings, as shown on the balance sheet, tell the story of a company’s cumulative profitability and what management has done with those profits. By understanding retained earnings, even those new to accounting can get insight into how a company balances growing the business versus returning profits to shareholders. It’s a fundamental concept that links a company’s past financial performance with its current financial position, providing a window into the company’s long-term value creation and financial strategy.