is a financial concept covered in this article. Miscellaneous Non-Recurring or Unusual Expenses Below Operating Income

The stock market is filled with individuals who know the price of everything but the value of nothing.

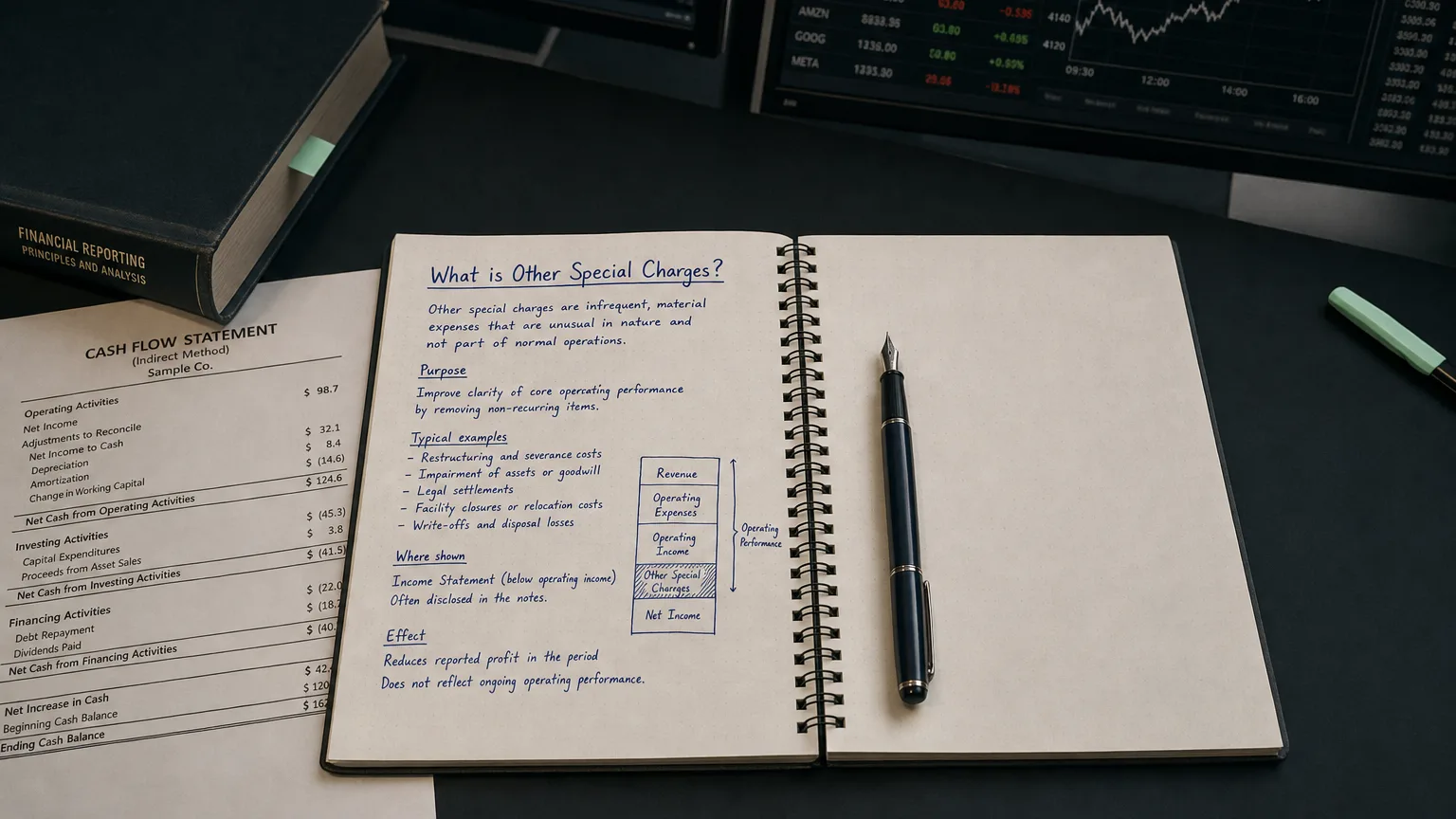

Other Special Charges is a catch-all category for significant, non-recurring, or unusual expenses that do not fit into more specific line items like restructuring, impairments, or litigation settlements. These charges are presented separately in the income statement (usually below operating income) to highlight their one-time or infrequent nature and to allow investors to better assess core ongoing profitability. Examples include environmental remediation costs, inventory obsolescence write-downs tied to specific events, certain regulatory fines, or other atypical expenses. While material, they are often excluded when companies or analysts calculate adjusted or normalized earnings.

What are Other Special Charges?

Other Special Charges represent a residual category for material expenses that are deemed outside normal operating activities but do not fall under more commonly labeled special items (e.g., restructuring or asset impairments).

Financial data providers and companies use this line to aggregate miscellaneous unusual costs, ensuring transparency while separating them from recurring operating expenses. These charges are pre-tax and reduce pretax income directly.

The category’s broad nature means contents vary significantly by company and industry—always review footnotes for specifics.

“The stock market is filled with individuals who know the price of everything but the value of nothing.”

— Philip Fisher, Author, Common Stocks and Uncommon Profits Common Stocks and Uncommon Profits (1958)

Common Items Classified as Other Special Charges

Typical examples include:

Frequent Components

- Environmental cleanup or remediation costs (e.g., site contamination)

- Regulatory fines or penalties not tied to litigation

- Inventory obsolescence or write-downs due to specific events (e.g., product recall)

- Contract termination fees outside restructuring programs

- Donations or charitable contributions of unusual size

- Relocation costs not part of broader restructuring

- One-time professional fees (e.g., special audits, investigations)

- Losses from natural disasters (if not classified elsewhere)

The unifying trait is that they are infrequent, material, and not expected to recur in the normal course of business.

How Other Special Charges Impact the Income Statement

They are deducted in the non-operating section:

Formula: Pretax Income = Operating Income − Other Special Charges − Specific Special Items (e.g., restructuring)

- Other Non-Operating Income − Net Interest Expense

The tax benefit from these charges appears in the tax provision, often providing a shield that partially offsets the pre-tax hit.

Tip: Companies commonly add back these charges (net of tax) when presenting non-GAAP adjusted earnings.

Examples

Example 1: Environmental Remediation

Manufacturing firm discovers legacy contamination at a closed site.

Estimated cleanup cost: 45M. This reduces pretax income but is highlighted as non-recurring.

Example 2: Regulatory Fine

Company settles with regulator over compliance issue (non-litigation).

Penalty: 60M.

Example 3: Product Obsolescence

Tech firm writes down inventory due to sudden regulatory ban on a component.

Write-down: 35M.

These examples show how unpredictable events can create material charges outside standard categories.

Importance in Financial Analysis

Analysts scrutinize other special charges to:

- Identify truly one-time costs for normalization

- Assess exposure to regulatory, environmental, or product risks

- Evaluate earnings quality—frequent charges may indicate underlying issues

- Forecast cleaner future profitability

Persistent appearance of ‘other’ charges can erode credibility of adjusted earnings if perceived as recurring costs being masked.

Warning: Overuse of broad ‘special charges’ categories can obscure operating trends—demand detailed disclosure.