Restructuring and Merger and Acquisition is a financial concept covered in this article. Costs Associated with Organizational Changes and Corporate Transactions

Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.

Restructuring and Merger and Acquisition (M&A) costs encompass the significant expenses incurred when a company undergoes major operational overhauls (restructuring) or engages in corporate transactions like mergers, acquisitions, or divestitures. Restructuring charges typically include employee severance, facility closures, and contract terminations to streamline operations and cut costs. M&A costs cover advisory fees, legal expenses, due diligence, integration efforts, and golden parachutes. These are non-recurring, often large charges reported below operating income as special items, providing a tax-deductible shield while signaling strategic shifts but distorting core earnings in the period incurred.

What are Restructuring and M&A Costs?

Restructuring costs arise from efforts to realign a company’s operations, workforce, or footprint for efficiency, often in response to declining performance, competitive pressures, or economic downturns. M&A costs stem from pursuing growth through acquisitions, mergers, or defensive consolidations.

Under US GAAP (ASC 420 for exit costs, ASC 805 for business combinations) and IFRS (IFRS 3, IAS 37), these are expensed as incurred or accrued when probable and estimable. They are classified as non-operating or special items to separate them from core results.

Restructuring often follows M&A (integration phase) or precedes it (pre-sale cleanup). Both create short-term earnings pressure but aim for long-term value creation.

These charges peaked during crises like 2008 GFC ($100B+ globally) and COVID-19 restructurings.

Breakdown of Restructuring Costs

Restructuring Components

- Employee termination benefits: Severance, early retirement, outplacement (one-time payments)

- Facility exit costs: Lease terminations, asset disposals, relocation

- Contract terminations: Vendor/supplier penalties, onerous contracts

- Other: Training for remaining staff, IT system decommissioning

One-time criterion: Must not recur; ongoing costs classified as operating.

“Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Breakdown of M&A Costs

M&A Transaction and Integration Costs

- Transaction fees: Investment bankers (1-2% of deal value), lawyers, accountants

- Due diligence: Audits, valuations, regulatory filings (antitrust)

- Integration: IT system merging, rebranding, cultural alignment

- Golden parachutes/change-in-control: Accelerated executive compensation

- Retention bonuses: Key employee incentives post-deal

Acquisition-related: Expensed immediately (post-2009); not capitalized into goodwill.

Tip: M&A costs average 1-5% of deal value; mega-deals can exceed $1B.

How These Costs Are Accounted For and Reported

Recognition timing:

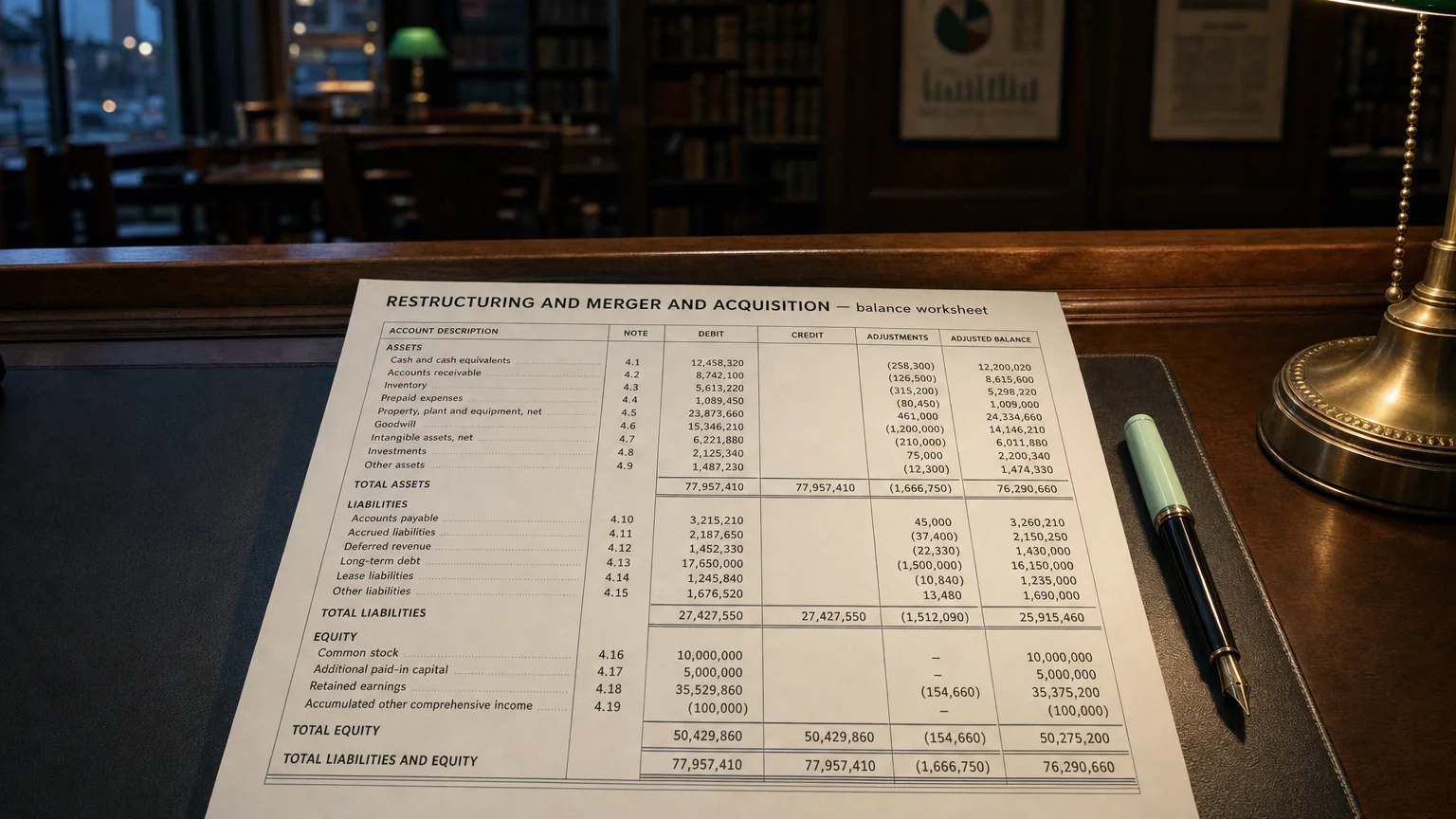

Formula: Restructuring Liability = PV of Expected Future Payments (discounted if >1 year)

Expense = Cash/Accrual + Amortization of Discount

Reporting Nuances

- Accrual: When committed (e.g., layoff notice given)

- Presentation: Below operating income as special charges

- Cash Flow: Operating outflow (non-cash portion added back)

- Tax: Generally deductible, creating deferred tax assets

Detailed Examples

Example 1: Global Restructuring

Tech giant cuts 10% workforce (20,000 jobs) and closes 100 offices.

Severance: 125K/employee) Facility exits: 800M Total Charge: 3B Yr1, $1.5B Yr2 cash).

Example 2: $50B M&A Deal

Pharma acquires rival.

Banker fees: 300M Integration (2 yrs): 200M Total M&A Costs: $2.45B (4.9% of deal).

Example 3: Failed M&A Attempt

Bid rejected after $500M spent on due diligence/advisors.

Charge: $500M as incurred (no asset acquired).

Charges often front-loaded; cash outflows lag over 1-3 years.

Importance in Financial Analysis

Strategic signal: Restructuring/M&A costs indicate transformation—cost cuts for margins, acquisitions for growth.

Earnings normalization: Add back net-of-tax (90%+ of analysts exclude in adjusted EBITDA/EPS).

Key Metrics Impacted

- ROIC/ROA: Improves post-charge (lower asset base)

- Free Cash Flow: Initially negative, then positive from savings

- Payout ratios: Pressured short-term

Red flags: Recurring ‘one-time’ charges (>20% of EBITDA annually) suggest deeper issues.

Warning: Watch liability reversals (unused reserves credited back to earnings).

Q · 01What is Restructuring And Merger And Acquisition?+