is a financial concept covered in this article. The Recognition of an Asset's Reduced or Zero Recoverable Value

Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.

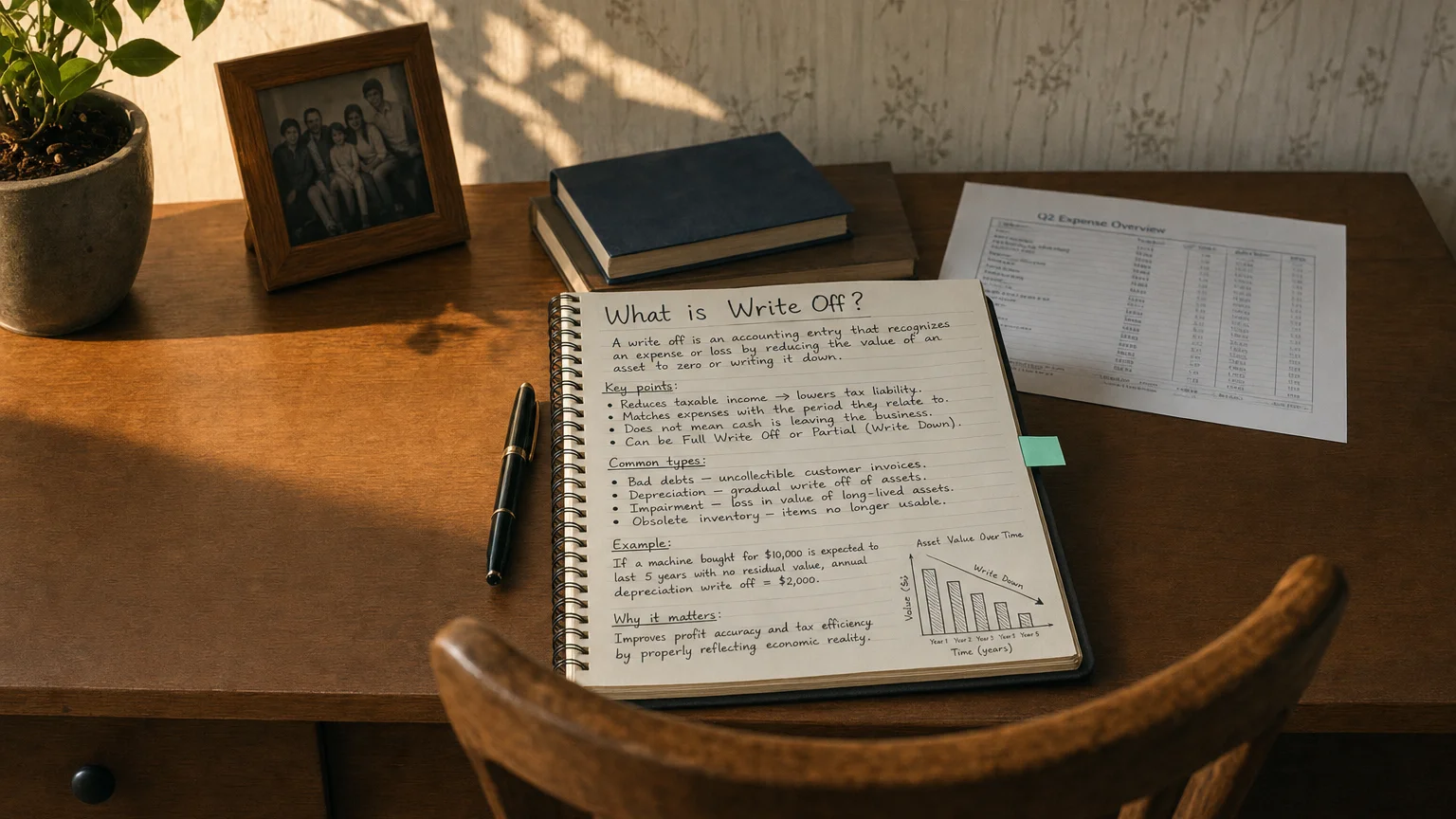

A write-off is the accounting process of reducing the carrying value of an asset on the balance sheet to reflect that it is no longer expected to provide future economic benefits or has become worthless. Common examples include uncollectible receivables (bad debts), obsolete inventory, impaired intangible assets, or damaged fixed assets. Write-offs are typically recorded as an expense in the income statement in the period the loss is identified, reducing reported earnings. While often non-recurring or tied to specific events, they signal potential issues in credit policies, inventory management, or asset utilization, making them important for assessing earnings quality and operational efficiency.

What is a Write-Off?

A write-off occurs when an asset’s recoverable amount falls below its carrying value, or it becomes entirely unrecoverable. The asset is either reduced to its estimated recoverable amount (partial write-off) or removed entirely from the balance sheet (full write-off).

Under US GAAP and IFRS, write-offs are recognized when evidence indicates the loss is probable and estimable. For receivables and inventory, provisions are often made earlier, with actual write-offs occurring later when confirmed.

Write-offs are non-cash expenses but reduce reported earnings and can generate tax benefits if deductible.

Common Types of Write-Offs

Write-offs affect various asset classes:

Major Categories

- Accounts Receivable (Bad Debt): Customer unlikely to pay; direct write-off or allowance method

- Inventory: Obsolete, damaged, or unsalable goods

- Property, Plant & Equipment: Physical damage, technological obsolescence

- Intangible Assets/Goodwill: Failed brands, patents, or acquisition underperformance

- Loans or Investments: Default or permanent decline in value

- Prepaid Expenses: Services no longer to be received

The income statement impact varies—bad debts may hit operating expenses, while others appear as special charges.

“Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

Accounting Treatment and Recognition

Journal entry for a full write-off:

Formula: Dr. Write-Off Expense (or specific charge) XXX Cr. Asset (or Allowance) XXX

For receivables using allowance method:

- Initial provision: Expense increases allowance

- Later write-off: Reduces receivable and allowance (no further expense)

Tip: Direct write-off method (no allowance) is used for immaterial amounts or under certain tax rules.

Examples of Write-Offs

Example 1: Bad Debt Write-Off

Customer files bankruptcy owing $150,000.

Previously provisioned 120,000 (no new expense). Remaining $30,000 charged as additional bad debt expense.

Example 2: Inventory Obsolescence

Tech company has $80M outdated components due to new regulation.

No salvage value. Write-Off Expense = 80M.

Example 3: Fixed Asset Damage

Factory equipment book value $500,000 destroyed in fire.

Insurance recovery 300,000 loss (non-operating or special charge).

Large write-offs often signal operational challenges or changing market conditions.

Importance in Financial Analysis

Write-offs matter because they:

- Reduce reported earnings and book value

- May indicate issues in credit, inventory, or asset management

- Are often added back in adjusted EBITDA/EPS calculations

- Can provide tax shields

Frequent or large write-offs warrant investigation—recurring bad debts suggest lax credit policies; inventory write-offs may reflect poor demand forecasting.

Warning: Aggressive provisioning followed by reversals can manipulate earnings—track allowance trends.