is a financial concept covered in this article. The Non-Cash Charge for Reduced Recoverable Value of Long-Term Assets

When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.

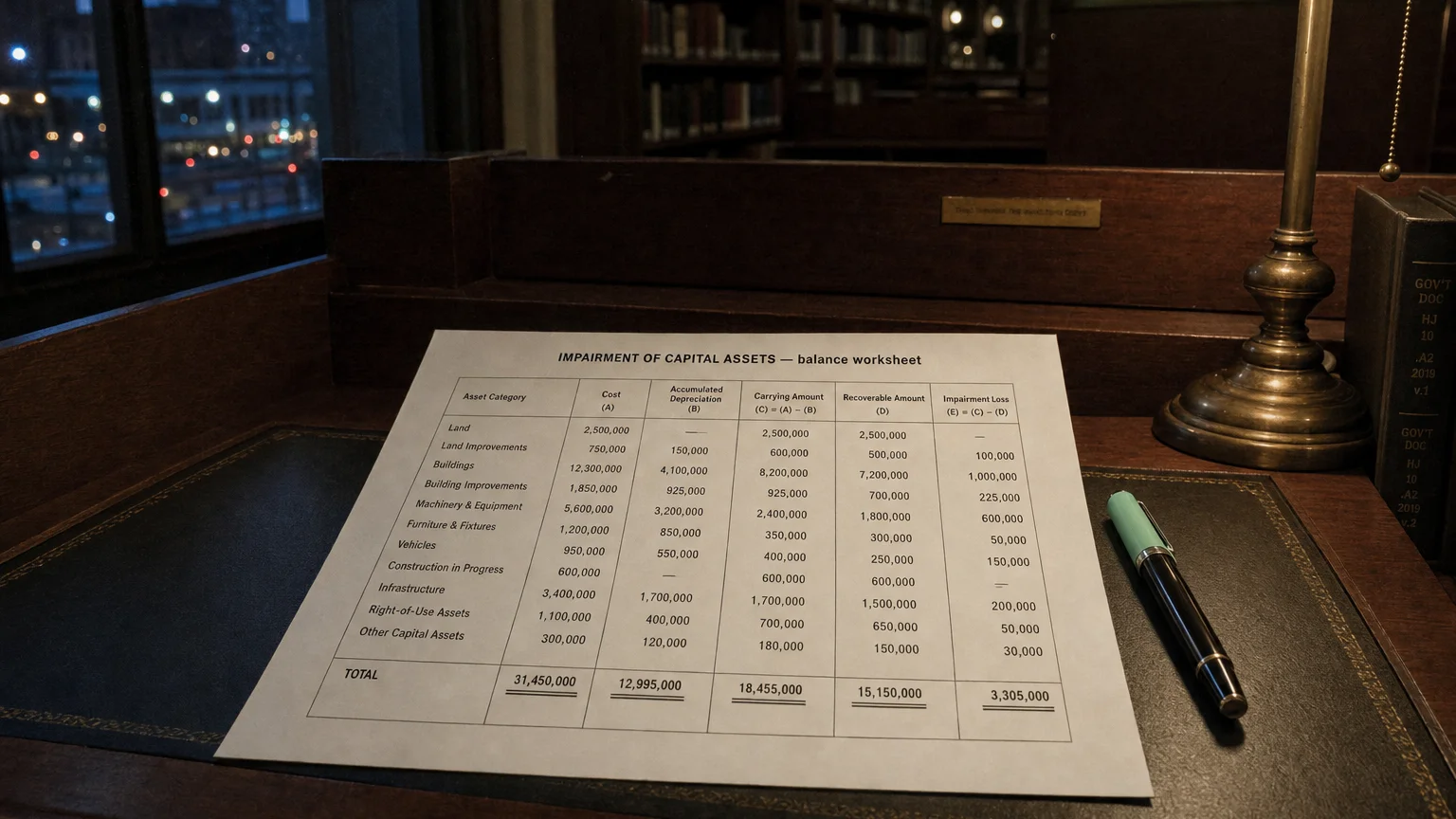

Impairment of Capital Assets occurs when the carrying value of long-term tangible or intangible assets (such as property, plant, equipment, goodwill, or other intangibles) exceeds their recoverable amount or fair value. Companies must recognize an impairment loss to write down the asset to its current recoverable value, resulting in a non-cash expense that reduces reported earnings. This charge reflects a permanent decline in the asset’s economic benefit and is a key indicator of potential overinvestment, changing market conditions, or strategic missteps. While non-recurring in nature, impairments are critical for understanding asset quality and true economic profitability.

What is Impairment of Capital Assets?

An impairment of capital assets is the accounting recognition that an asset’s carrying amount on the balance sheet exceeds its recoverable amount—the higher of fair value less costs to sell or value in use (future cash flows discounted).

Impairments apply to long-lived assets (PP&E, intangibles) and goodwill. They are non-cash charges that reduce the asset’s book value and flow through the income statement as an expense, lowering pretax income and net earnings.

US GAAP (ASC 360 for tangible, ASC 350 for intangibles/goodwill) and IFRS (IAS 36) require periodic impairment testing when indicators exist (e.g., market decline, obsolescence, legal changes).

Goodwill impairments are permanent and irreversible under both standards; other asset impairments can be reversed under IFRS (but not US GAAP).

Impairment Testing Process

The process differs slightly by standard and asset type:

Key Steps (Simplified)

- Identify indicators: Market value drop, adverse changes, obsolescence

- Recoverability test (US GAAP for long-lived assets): Undiscounted future cash flows < carrying amount → impaired

- Measurement: Write down to fair value (US GAAP) or recoverable amount (IFRS)

- Goodwill: Annual test or triggered; compare carrying value of reporting unit to fair value

- Recognition: Impairment loss = Carrying Amount − Recoverable/Fair Value

Tip: Fair value often uses market comparables, discounted cash flows, or appraisals.

“When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Annual Report (1985)

Examples of Impairment Charges

Real-world cases illustrate triggers and magnitude.

Example 1: PP&E Impairment

Oil company has refinery with book value $800M.

Declining demand and low margins → undiscounted cash flows 550M. Impairment Charge = 550M = $250M (non-cash expense).

Example 2: Goodwill Impairment

Tech firm acquires startup for 700M goodwill).

Product fails → reporting unit fair value 1B). Goodwill Impairment = $600M (full goodwill write-down possible).

Example 3: Intangible Asset

Brand valued at $200M impaired due to scandal.

Revised fair value 120M (reversible under IFRS if conditions improve).

Impairments often cluster in downturns or after aggressive acquisitions.

Presentation in Financial Statements

Impairment charges typically appear as:

Common Locations

- Operating expenses (if asset group related to operations)

- Special or non-operating charges (especially large or goodwill)

- Part of Total Unusual Items in detailed breakdowns

They reduce pretax income; tax effects vary by jurisdiction and deductibility.

Importance in Financial Analysis

Impairments are critical signals:

- Overpayment in acquisitions (goodwill heavy)

- Changing industry dynamics (obsolescence)

- Asset quality issues (poor capital allocation)

- Non-cash but reduce book value and future depreciation

Analysts usually add back impairments (net of tax) for normalized earnings and EBITDA, but scrutinize recurrence and underlying causes.

Warning: Frequent impairments may indicate systematic overinvestment or delayed recognition—review capex trends and ROIC.

In valuation, adjust historical metrics and assess remaining asset base durability.

Q · 01What is Impairment Of Capital Assets?+