Reconciled Depreciation What It Is and How to Read It on

Reconciled depreciation adjusts reported depreciation to remove non-cash line-item differences between financial statements. Learn how to read and interpret it.

Overview

Reconciled depreciation adjusts reported depreciation to remove non-cash line-item differences between financial statements. Learn how to read and interpret it.

What Is Reconciled Depreciation?

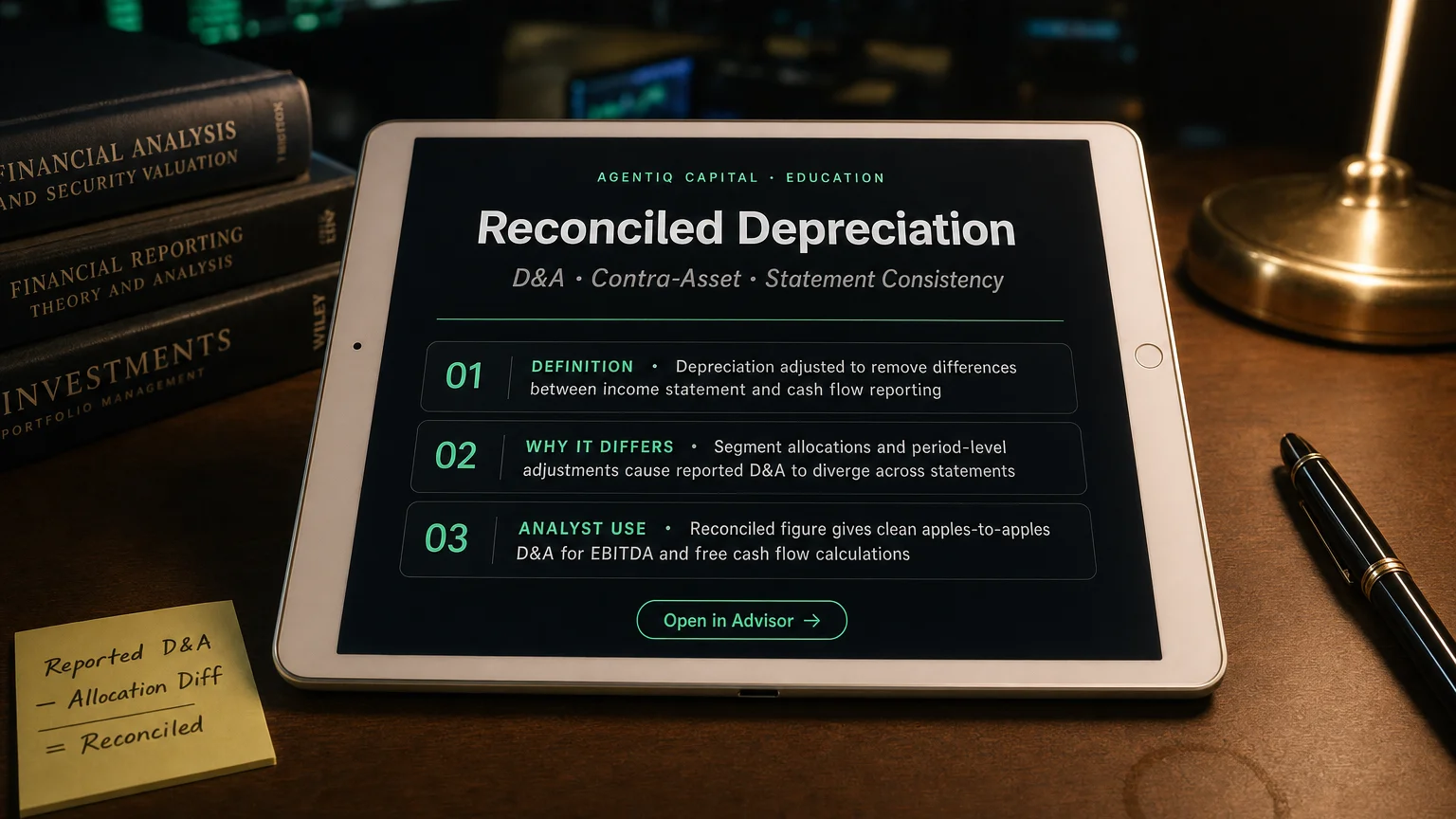

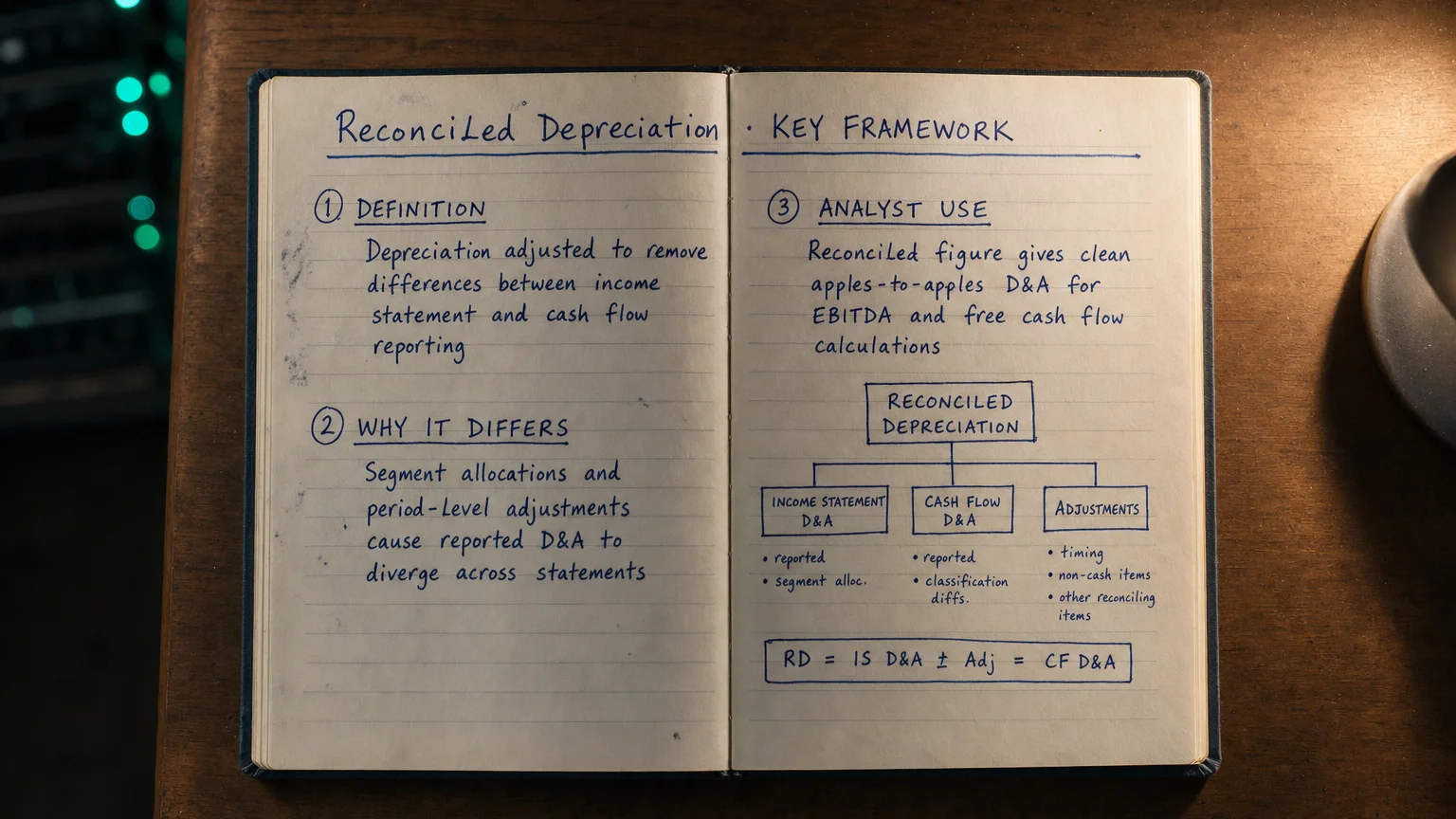

Reconciled depreciation refers to the depreciation charge that has been adjusted or reconciled across a company's financial statements to ensure internal consistency. Unlike the headline D&A figure reported on the income statement, reconciled depreciation accounts for differences that arise from segment reporting, capitalised costs, and accounting policy choices.

Analysts tracking earnings quality or building discounted cash flow models rely on reconciled figures to avoid double-counting or under-counting non-cash charges.

Why Reconciliation Is Necessary

Companies report depreciation in multiple places:

- Income Statement — as part of operating expenses or cost of goods sold

- Cash Flow Statement — as an add-back to net income under operating activities

- Notes to Financial Statements — broken out by asset class or segment

These figures can differ due to:

- Accelerated vs straight-line depreciation applied in different segments

- Capitalised interest rolled into PP&E and depreciated over asset life

- Asset impairments that flow through depreciation in some periods

- Lease accounting (ASC 842 / IFRS 16) creating right-of-use asset depreciation

Reconciled depreciation takes the starting figure and adds or removes these differences to arrive at a clean, comparable number.

"In the short run, the market is a voting machine. In the long run, it is a weighing machine."

— Benjamin Graham, Author, The Intelligent Investor Security Analysis (1934)

How to Identify Reconciled Depreciation in Filings

In a 10-K or 10-Q, look for:

- The Supplemental Cash Flow Disclosures section, which discloses non-cash investing and financing activities

- Segment reporting footnotes, which may show depreciation by segment that does not add up to the consolidated figure without reconciling items

- The MD&A section, where management often discusses D&A as a percentage of revenue with reconciling commentary

Key Takeaways

- Reconciled depreciation adjusts the reported D&A figure for cross-statement differences

- It is most relevant when comparing companies within capital-intensive industries

- Analysts use it to build accurate free cash flow models and quality-of-earnings assessments

- Always cross-reference the income statement D&A with the cash flow statement add-back before modelling