A key corporate finance action where a company uses its cash to buy back its own shares from the market, impacting cash flow, financial metrics, and shareholder

If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes.

A repurchase of capital stock, also known as a share repurchase or stock buyback, is when a company buys back its own shares from the marketplace using company cash. In effect, the company is re-acquiring ownership that was previously held by public shareholders, reducing the total number of shares outstanding. Share repurchases are a primary method for a company to return cash to shareholders, similar to paying dividends. Companies typically undertake buybacks when they have excess cash and believe their stock is a good investment, often because management considers the stock undervalued and has confidence in the company’s future.

Accounting and Financial Statement Presentation

On the statement of cash flows, stock buybacks are a core component of the Cash Flow from Financing Activities section. This section tracks all cash transactions between the company and its owners (shareholders) and creditors. A repurchase of capital stock is always recorded as a cash outflow (a negative number), as the company is spending its cash to buy back equity from the public. It is treated similarly to paying a dividend or repaying debt—money is flowing out of the company to capital providers. You will typically find a line item labeled “Repurchase of stock,” “Share buybacks,” or “Purchase of treasury stock” in this section.

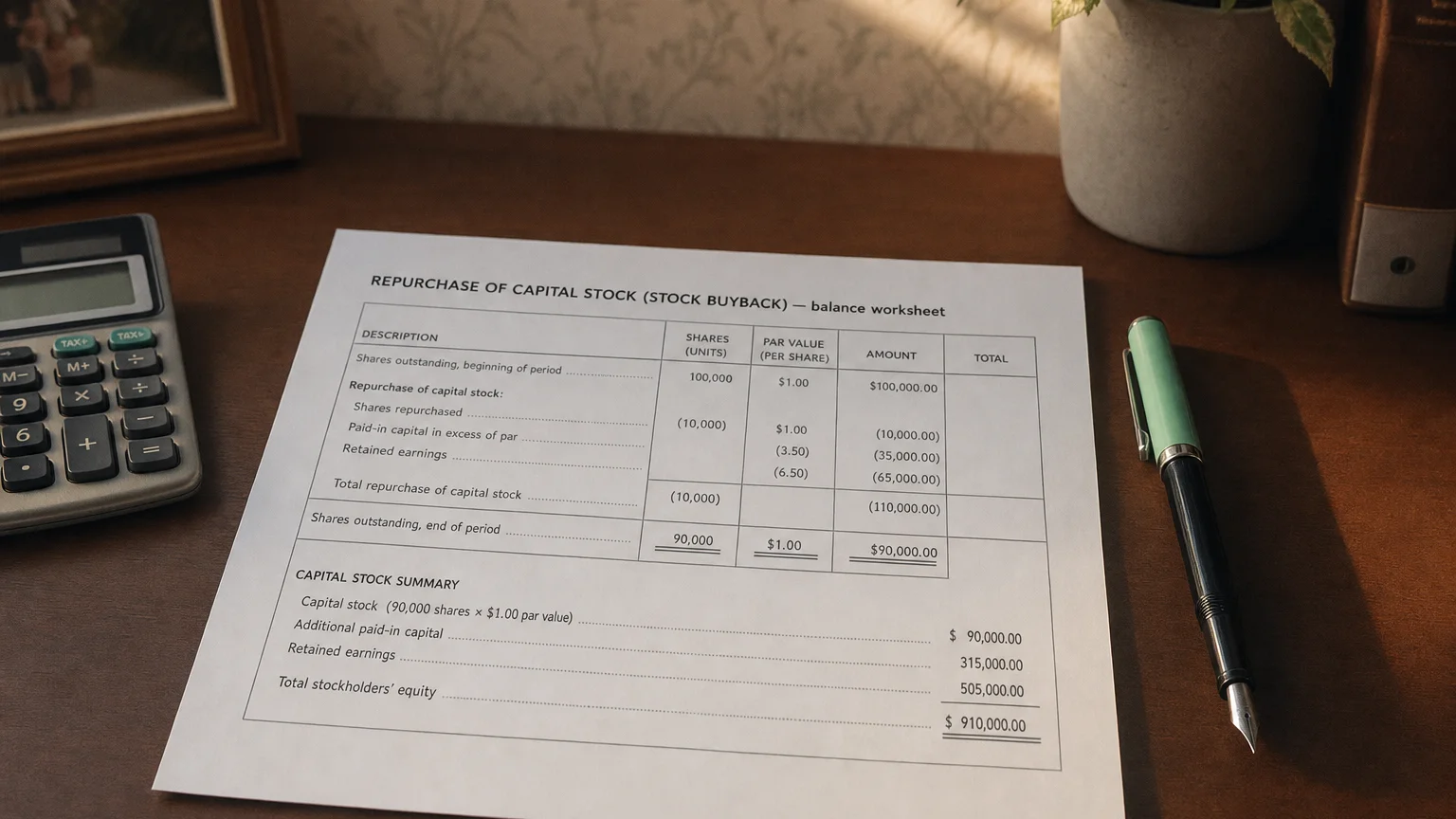

A stock repurchase has a dual impact on the balance sheet: it reduces both assets and shareholders’ equity. The cash used for the buyback decreases the ‘Cash and Cash Equivalents’ asset account. Simultaneously, shareholders’ equity is reduced by the same amount. When shares are repurchased, they are often held by the company as treasury stock. Treasury stock is a contra-equity account, meaning it carries a negative balance and directly reduces total shareholders’ equity.

Not an Expense

Crucially, a share repurchase is not an expense and does not affect the income statement’s net income. The transaction bypasses the income statement entirely. This is why net income remains unchanged, but per-share metrics like Earnings Per Share (EPS) improve, as the same earnings are divided by a smaller number of shares.

The Strategic Rationale Behind Stock Buybacks

Companies repurchase their own shares for several strategic and financial reasons:

- Return Excess Cash to Shareholders: Buybacks are a flexible alternative to dividends for returning capital. If a company has more cash than it needs for operations or attractive investments, buying back stock provides value to shareholders without the long-term commitment of a fixed dividend.

- Signal Confidence and Undervaluation: A buyback often serves as a powerful signal from management to the market. It implies that insiders believe the stock is undervalued and are confident in the company’s future prospects. Essentially, the company is investing in itself.

- Improve Financial Metrics: By reducing the number of shares outstanding, buybacks mechanically boost important per-share metrics. Earnings Per Share (EPS) increases because total earnings are divided by fewer shares. Return on Equity (ROE) can also improve because the denominator (shareholders’ equity) shrinks.

- Consolidate Ownership and Prevent Dilution: Repurchases increase the ownership percentage of the remaining shareholders. This is often done to offset the dilutive effect of issuing new shares for employee compensation plans or acquisitions. It can also make a hostile takeover more difficult by reducing the number of shares available on the open market.

- Optimize Capital Structure: Management may use buybacks to adjust the company’s mix of debt and equity. If a company feels it is over-equitized, it might repurchase shares, potentially lowering its overall cost of capital, especially in a low-interest-rate environment.

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

Why Analysts and Investors Closely Monitor Buybacks

Stock buybacks are a focal point for financial analysis because they reveal much about a company’s strategy, financial health, and management’s priorities.

A Window into Management’s Thinking

Analysts scrutinize buybacks to understand a company’s capital allocation strategy. The decision to spend billions on buybacks instead of on R&D, acquisitions, or debt reduction reveals how management perceives the best use of capital and its outlook on future growth.

- Indicator of Confidence and Health: A significant buyback program suggests the company is generating strong, sustainable cash flow and is confident enough in its future to invest in its own stock.

- Impact on Share Price: Repurchases can boost a stock’s price in the short term by reducing supply and creating buying pressure. This often attracts investors who anticipate price appreciation.

- Total Shareholder Yield: Many investors look beyond dividend yield to shareholder yield, which combines dividends and the value of buybacks. A large buyback program significantly increases this total return to shareholders.

- Magnitude and Trend: The scale of a buyback is important. A consistent, long-term buyback program is often viewed as a sign of a shareholder-friendly company. For example, Apple’s repurchase of $95.0 billion of its stock in fiscal 2024 sent a powerful message about its massive cash generation and management’s confidence.

Q · 01What is Repurchase Of Capital Stock?+