Taxes Refund Paid is a financial concept covered in this article. Cash Outflows for Tax Refunds Issued to Customers or Employees

It does not matter how frequently something succeeds if failure is too costly to bear.

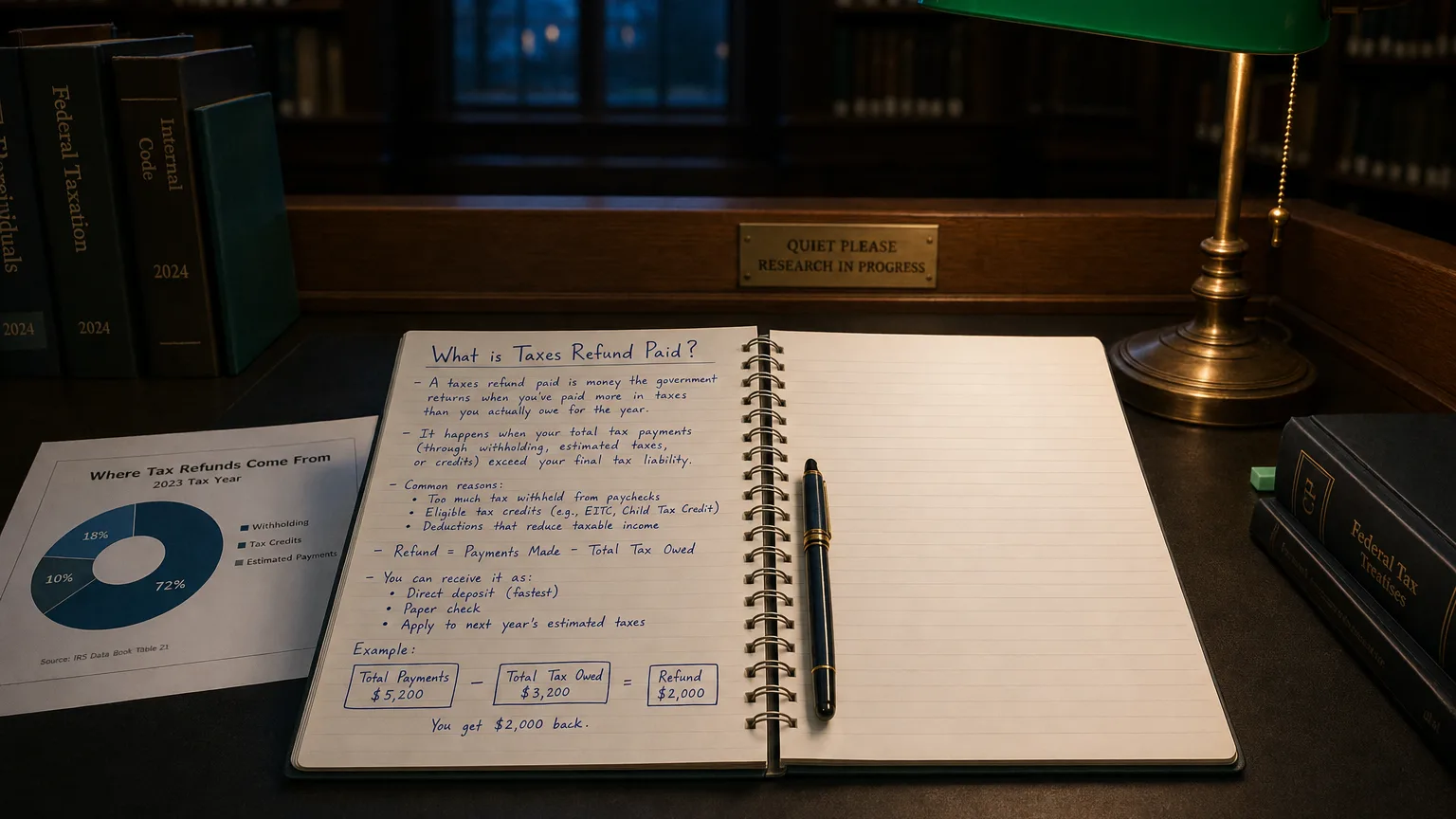

Taxes Refund Paid represents cash outflows when a company issues refunds for overcollected taxes—typically sales tax, VAT/GST, or withholding tax—to customers, employees, or other parties. This line appears in the cash flow statement (usually operating activities) and reflects the return of taxes previously collected or withheld that were later determined to be overpaid or eligible for refund.

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

What It Represents

Taxes Refund Paid is cash the company returns when it has collected too much tax from customers or withheld excess from employees/payees.

The company acts as a collection agent for the government—when refunds are due, it pays out from amounts previously gathered.

Not the company’s own corporate tax refund—that’s usually netted with payments.

Common Scenarios

- Customer returns goods → refund sales tax/VAT collected

- Exempt customer (e.g., government, charity) → refund previously charged tax

- Over-withheld payroll taxes corrected

- VAT input credit exceeds output → refund from tax authority (sometimes routed through company)

- Export sales qualifying for zero-rating → refund input tax

Retailers and e-commerce see this most from returns; exporters from VAT regimes.

A Simple Example

Online retailer collects 8% sales tax on 80k tax collected.

- Customers return 16k tax refund due

- Company pays $16k cash back to customers

- Cash flow statement: -$16k Taxes Refund Paid

- Remits net $64k to tax authority

Cash leaves, reducing operating cash flow.

Accounting Treatment

- Tax initially collected → liability (Tax Payable)

- Refund due → reduce liability, record cash outflow

- Usually operating activity (core business collection)

- Direct method: explicit line

- Indirect method: embedded in changes

Matches timing of original tax collection.

Presentation in Cash Flow

In operating activities as:

- ‘Taxes Refund Paid’

- ‘Cash Paid for Tax Refunds’

- Direct method: separate line

- Indirect: part of working capital or other adjustments

Supplemental disclosure common.

What It Signals

- Return volume (high refunds = high returns)

- Customer exemption processing

- Export or zero-rated sales activity

- Working capital drag from tax cycle

- Operational efficiency in tax handling

Large/spiking refunds may indicate quality issues or aggressive sales tactics.