A comprehensive guide to the short-term portion of a company's borrowings and lease financing, and their impact on liquidity and risk analysis.

It does not matter how frequently something succeeds if failure is too costly to bear.

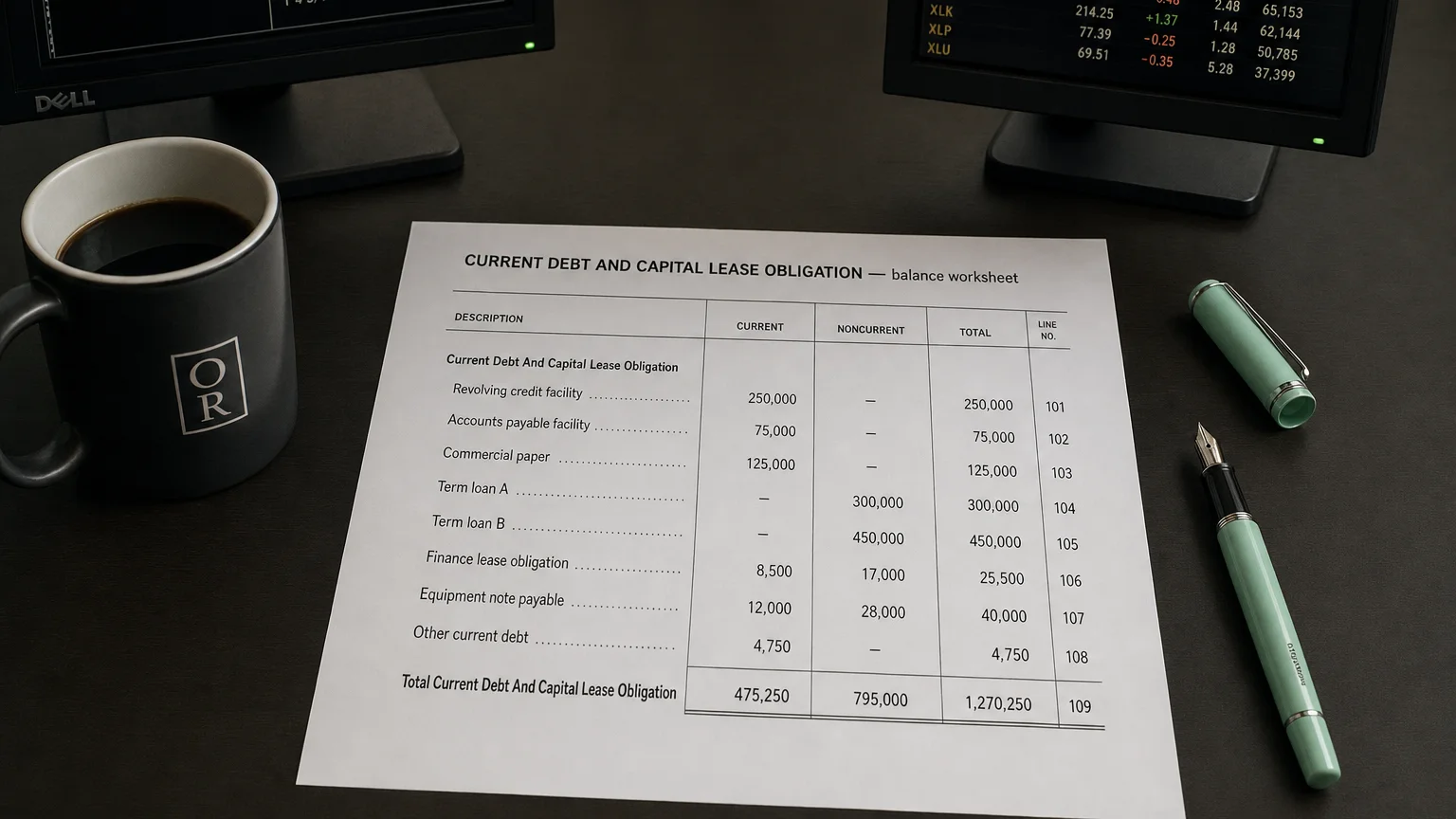

Current debt refers to the portion of a company’s formal borrowings that is due to be paid within the next 12 months. A capital lease obligation is the liability recorded for a lease contract that is treated like a financed asset purchase. The term ‘Current Debt and Capital Lease Obligation’ represents the sum of these short-term liabilities, reflecting immediate financial commitments from both traditional loans and debt-like lease agreements.

Defining the Components

Current debt (or short-term debt) includes obligations like short-term bank loans, overdrafts, notes payable due within a year, and, most commonly, the current portion of long-term debt. This is the principal amount of any long-term loan or bond that must be paid in the coming year.

A capital lease obligation arises from a lease that transfers most risks and benefits of ownership to the lessee. The liability represents the present value of future lease payments. The portion of these payments due within one year constitutes the current capital lease obligation.

Accounting Treatment of Capital Leases (Old vs. New Standards)

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

The accounting for leases has undergone a major transformation to increase transparency.

Legacy Standards (ASC 840 / IAS 17)

Previously, only leases meeting specific criteria (e.g., lease term >75% of asset life, bargain purchase option) were ‘capitalized’ on the balance sheet. Other leases, called ‘operating leases,’ were kept off-balance sheet, which could understate a company’s true liabilities.

Modern Standards (ASC 842 / IFRS 16)

Implemented around 2019, these new rules require companies to recognize virtually all leases longer than 12 months on the balance sheet. This creates a Right-of-Use (ROU) asset and a corresponding lease liability. The term ‘capital lease’ is now formally known as a ‘finance lease’. This change ensures that lease obligations are transparently reported alongside traditional debt.

Why These Obligations Matter to Investors

Both current debt and current lease obligations are critical for financial analysis:

- Liquidity and Short-Term Risk: These liabilities are key components of Total Current Liabilities. Analysts use them to calculate the Current Ratio () to assess if a company can meet its near-term obligations. A high amount of debt due soon can signal a liquidity crunch.

- Leverage and Solvency: While the focus is on the short-term portion, these obligations are part of a larger debt structure that affects a company’s overall leverage. Analysts include total lease liabilities with total debt to get a complete picture of a company’s indebtedness when calculating ratios like Debt-to-Equity.

- Cash Flow Impact: Scheduled debt and lease payments are predictable and significant cash outflows. Analysts review these commitments to forecast a company’s future cash needs and its capacity to invest or pay dividends.

- Transparency: The mandatory capitalization of leases under new standards gives investors a much clearer and more accurate view of a company’s total financial commitments, preventing liabilities from being ‘hidden’ in footnotes.

Q · 01What is Current Debt And Capital Lease Obligation?+