A detailed guide to a company's major long-term financing sources, explaining their accounting treatment, key differences, and impact on financial analysis.

Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.

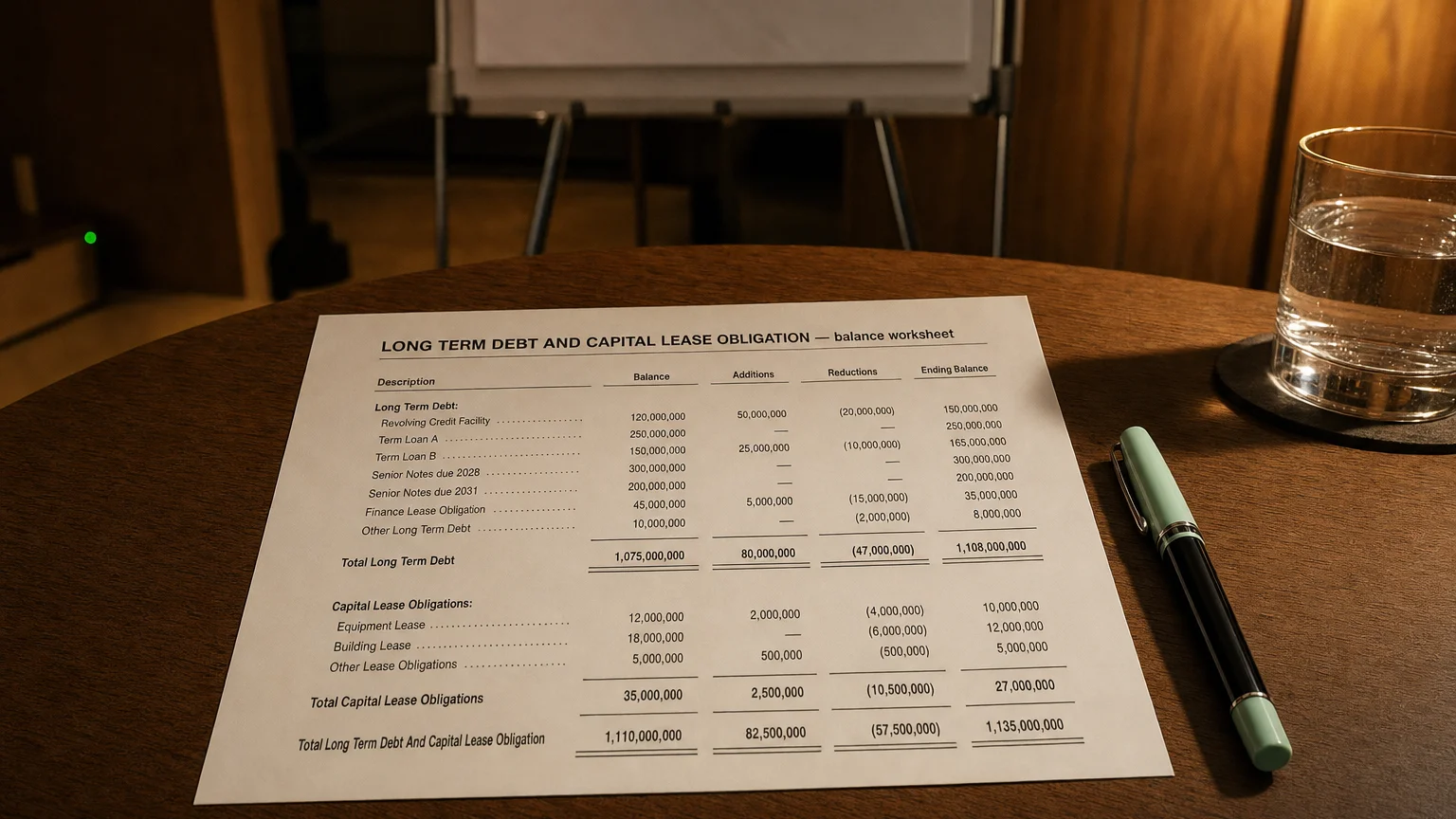

Companies often finance their operations and assets through various long-term liabilities. Two common items seen on the balance sheet are long-term debt and capital lease obligations. Long-term debt refers to traditional borrowings like loans and bonds, while capital lease obligations arise from lease contracts that are economically similar to a financed purchase of an asset. Both represent significant financial commitments that are crucial for understanding a company’s leverage and overall financial health.

Defining the Components

Long-term debt (LTD) refers to borrowings that are due in more than one year’s time. It is classified as a non-current liability on the balance sheet and can include items like corporate bonds, bank term loans, mortgages, and debentures.

A capital lease obligation is the liability recorded for a lease contract that transfers most of the risks and benefits of ownership to the lessee. It represents the present value of future lease payments. In essence, the lease is treated as if the company purchased the asset with debt financing. Under modern standards, this is more commonly called a ‘finance lease’.

Accounting Treatment under GAAP and IFRS

“Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 2014 (2014)

Under both U.S. GAAP and IFRS, long-term debt is recorded as a liability and measured at amortized cost, with interest expense recognized over time. Any portion due within 12 months is reclassified as a current liability.

Lease Accounting: Old vs. New Standards

The accounting for leases was significantly updated around 2019 with the introduction of ASC 842 (GAAP) and IFRS 16.

Legacy Rules (ASC 840/IAS 17): Leases were classified as either ‘capital’ (on-balance sheet) or ‘operating’ (off-balance sheet). A lease was capitalized if it met specific criteria (e.g., transfer of ownership, bargain purchase option).

New Rules (ASC 842/IFRS 16): These standards require that virtually all long-term leases be recorded on the balance sheet with a ‘Right-of-Use’ asset and a corresponding ‘Lease Liability’. This was done to eliminate off-balance-sheet financing and increase transparency. The term ‘capital lease’ was replaced with ‘finance lease’.

Key Differences: Long-Term Debt vs. Capital Lease Obligations

While both are long-term liabilities, there are important differences:

- Nature of the Obligation: Debt is a borrowing of funds, while a lease obligation arises from a contract to use a specific asset.

- Underlying Asset: A capital lease is directly tied to a specific leased asset (e.g., a building or airplane) that appears on the balance sheet. Debt proceeds are fungible and can be used for any corporate purpose.

- Legal Form: Debt is a formal debtor-creditor relationship. A lease is legally a rental agreement, but it is treated like debt for accounting purposes due to its economic substance.

- Accounting Presentation: While both are liabilities, they are often presented on separate lines on the balance sheet (e.g., ‘Long-term debt’ and ‘Lease liabilities’).

Use in Financial Analysis: Leverage and Risk Assessment

Analysts almost always aggregate long-term debt and lease obligations to evaluate a company’s true financial leverage and risk:

- Leverage Ratios: Both are included in the numerator for key metrics like the Debt-to-Equity and Debt-to-Assets ratios. The new lease standards caused many companies’ reported leverage to increase significantly.

- Coverage Ratios: Fixed-charge coverage ratios are used to assess a company’s ability to meet all its fixed payments, including both interest on debt and lease payments.

- Liquidity and Cash Flow Impact: Scheduled repayments for both debt and leases are critical cash outflows that must be factored into any liquidity or free cash flow analysis.

- Risk Assessment: High levels of both debt and lease obligations increase a company’s fixed costs and financial risk, making it more vulnerable during economic downturns.

Q · 01What is Long Term Debt And Capital Lease Obligation?+