A detailed guide to the short-term portion of a company's lease liabilities, explaining its calculation, presentation, and impact on liquidity analysis.

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

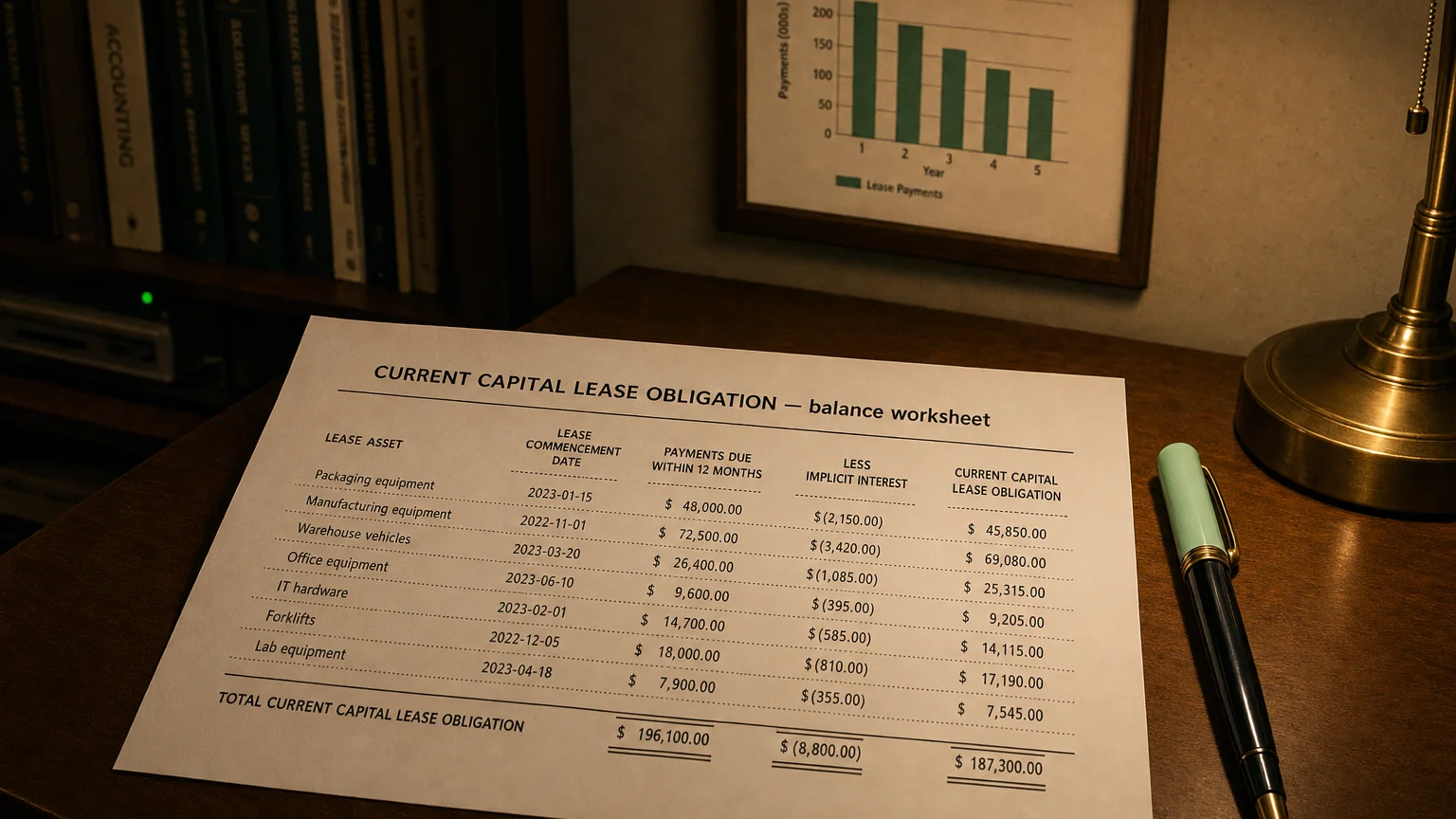

A Current Capital Lease Obligation refers to the portion of a capital lease liability that is due within the next 12 months from the balance sheet date. When a company enters a lease that is economically similar to a financed purchase (a capital or finance lease), it records a liability for the total obligation. The ‘current’ portion is the part of that liability that must be paid in the upcoming year, and it is reported under current liabilities on the balance sheet.

Calculation and Balance Sheet Presentation

The total capital lease obligation is calculated as the present value of all remaining lease payments. To determine the current portion, a company uses a lease amortization schedule to identify the total principal amount of payments that will be made in the next 12 months. This sum is the Current Capital Lease Obligation.

On the balance sheet, this amount is listed under Current Liabilities, often with a label like “Current portion of capital lease obligations.” The remaining principal balance due beyond one year is shown under Non-Current Liabilities. This presentation clearly informs stakeholders about the timing of the company’s obligations.

Historical vs. Current Accounting Treatment

“No asset is so good that it can’t become a bad investment if bought at too high a price, and there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Historical Standards (ASC 840 / IAS 17)

Under older rules, only leases that met specific ‘bright-line’ tests (e.g., covering >75% of an asset’s life or having a bargain purchase option) were capitalized. Other leases, called operating leases, were kept off-balance sheet, which could obscure a company’s true leverage.

Modern Standards (ASC 842 / IFRS 16)

Implemented around 2019, these new standards require that virtually all leases longer than 12 months be recorded on the balance sheet. This involves recognizing a Right-of-Use (ROU) asset and a corresponding lease liability. The term ‘capital lease’ has been formally replaced by ‘finance lease’ under U.S. GAAP. This change dramatically increased transparency by making most lease obligations visible as liabilities.

Comparison with Other Liabilities

A current capital lease obligation is similar in nature to other forms of current debt, but with some key distinctions:

- vs. Accounts Payable: While both are current liabilities, a lease obligation is a financing arrangement that includes an interest component and is secured by the leased asset. Accounts payable are typically non-interest-bearing operational liabilities owed to suppliers.

- vs. Short-Term Loans: Both are interest-bearing debts due within a year. A key difference is that a lease obligation is tied to a specific physical asset, whereas a loan provides cash that can be used for general purposes.

- vs. Operating Leases (Historical): Previously, operating lease commitments were hidden in footnotes. The ‘Current Capital Lease Obligation’ was distinct because it was one of the few lease types shown on the balance sheet. Today, this distinction is less relevant as nearly all leases create a current liability.

Impact on Financial Ratios and Analysis

Recognizing lease obligations on the balance sheet has notable effects on financial analysis:

- Leverage and Solvency: Capitalizing leases increases reported liabilities, causing leverage ratios like Debt-to-Equity to appear higher. This provides a more accurate view of a company’s risk.

- Liquidity: The current portion of the lease liability is a key input for the Current Ratio. The new accounting rules increased the reported current liabilities for many firms, making their liquidity position appear tighter.

- Profitability: For finance leases, the expense is front-loaded because of higher interest in the early years. This can result in lower net income initially compared to the old operating lease method. However, it also leads to higher EBITDA, as the former rent expense is replaced by interest and depreciation, which are excluded from EBITDA.

Example of a Capital Lease Obligation

Suppose a company enters a 5-year finance lease for equipment. The present value of all future payments is 80,000. If the principal payments scheduled for the second year total $20,000, then on its year-end balance sheet, the company will report:

- Current Capital Lease Obligation: $20,000

- Long-Term Lease Obligation: $60,000

This clearly shows that $20,000 of the ‘lease loan’ must be paid within the next 12 months.

Q · 01What is Current Capital Lease Obligation?+