A comprehensive guide to how leases are defined, classified, and reported on the balance sheet under modern standards like ASC 842 and IFRS 16.

Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.

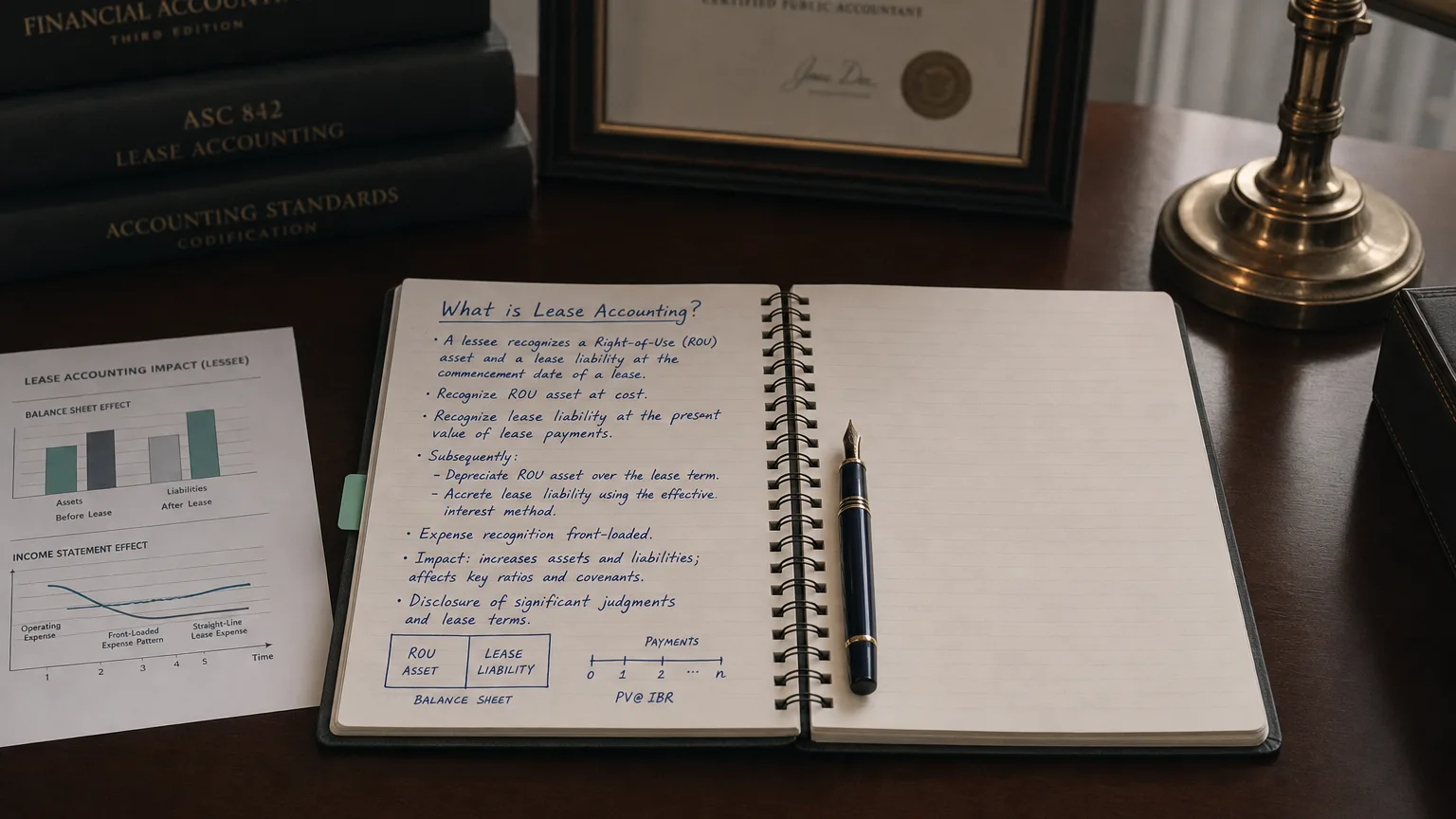

In accounting, a lease is a contract that conveys the right to use an identified asset for a period of time in exchange for consideration. In other words, the lessee (user) pays the lessor (owner) to use an asset for an agreed term. Under modern accounting, the lessee’s primary asset is this intangible right-to-use, not the physical asset itself. This ‘right-of-use’ approach is fundamental to how leases are now reported on the balance sheet.

Types of Leases: Operating vs. Finance

Leases are broadly classified into two types based on whether they transfer the risks and rewards of ownership to the lessee.

- Finance Lease (formerly Capital Lease): This lease is economically similar to a financed purchase of an asset. It effectively transfers substantially all the risks and rewards of ownership to the lessee. Historically, these have always been recorded on the balance sheet.

- Operating Lease: This is any lease other than a finance lease, more akin to simple renting. Historically, these were kept off the balance sheet, which obscured a company’s true financial obligations and led to major accounting rule changes.

The New Era: Bringing Leases onto the Balance Sheet

“Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Annual Letter (1985)

Under the new standards (ASC 842 in U.S. GAAP and IFRS 16 internationally), the distinction between lease types has less impact on the balance sheet. For the lessee, almost all leases must now be recognized.

The ROU Asset and Lease Liability

At the start of a lease, the lessee records two new items:

- A Right-of-Use (ROU) Asset, representing the right to use the asset over the lease term.

- A Lease Liability, representing the obligation to make future lease payments. Both are measured at the present value of the lease payments, meaning a company’s total assets and total liabilities increase significantly.

This change provides greater transparency, showing investors and creditors the true extent of a company’s commitments. The only common exceptions are for short-term leases (≤ 12 months) and, under IFRS, leases of low-value assets.

Key Differences: GAAP (ASC 842) vs. IFRS (IFRS 16)

While both standards bring leases onto the balance sheet, their approaches for lessees differ in a critical way:

- U.S. GAAP (ASC 842): Maintains a dual-model approach. Leases are still classified as either Operating or Finance. While both appear on the balance sheet, their classification affects how expenses are reported on the income statement and how cash flows are classified.

- IFRS (IFRS 16): Uses a single-model approach for lessees. It eliminated the operating lease classification. All leases are accounted for as finance leases, simplifying the process but affecting key metrics like EBITDA differently than GAAP.

Impact on Income Statement and Cash Flow

The classification of a lease under U.S. GAAP determines its impact on a company’s reported earnings and cash flows.

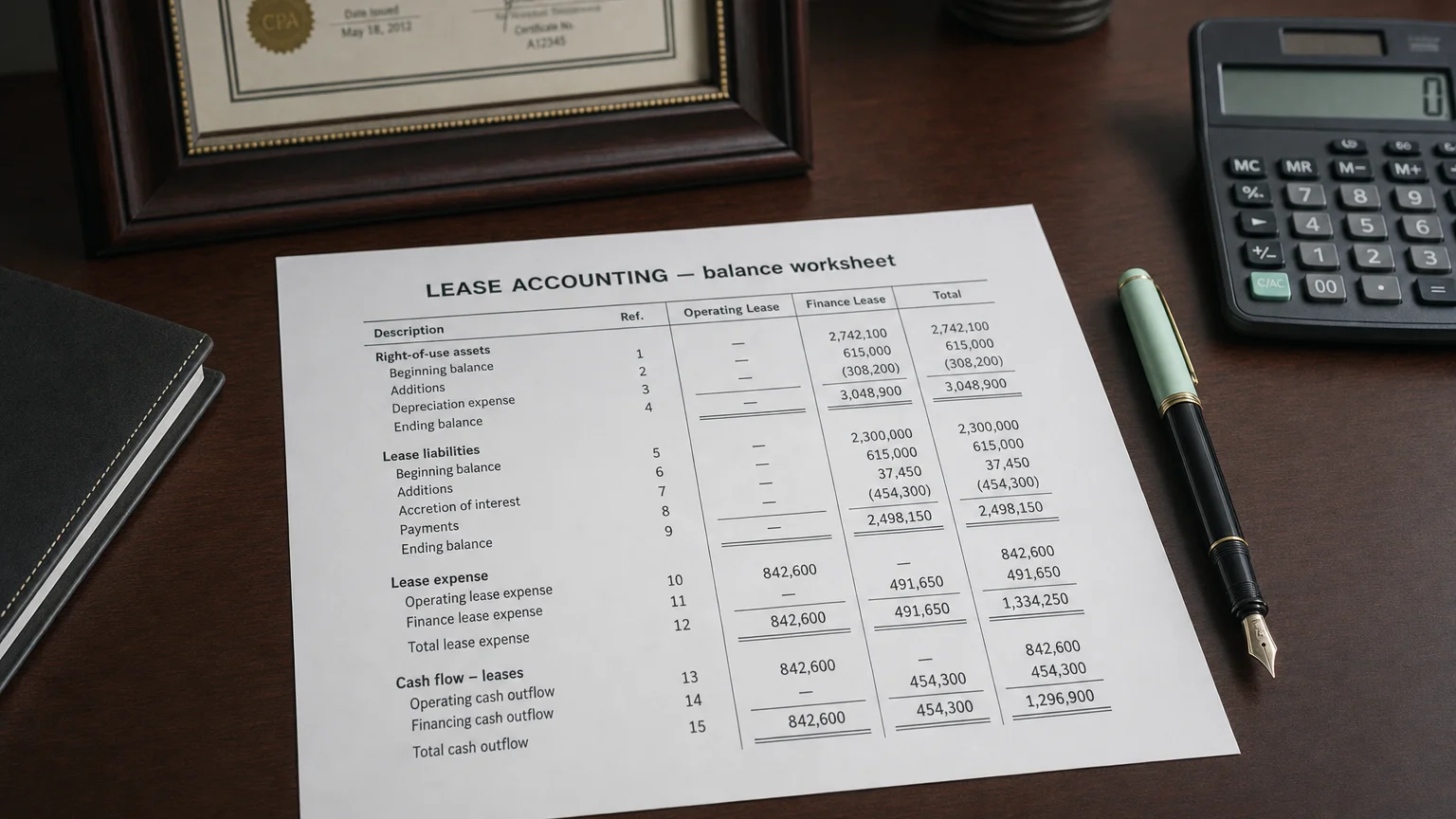

Finance Lease vs. Operating Lease (U.S. GAAP)

Income Statement:

- Finance Lease: Shows separate interest expense and amortization expense. The total expense is front-loaded (higher in early years).

- Operating Lease: Shows a single, straight-line lease expense each period, resulting in a smooth, predictable cost.

Cash Flow Statement:

- Finance Lease: Payments are split between principal (a financing outflow) and interest (an operating outflow).

- Operating Lease: The entire lease payment is classified as an operating cash outflow.

These differences are significant for analysis. For example, a finance lease results in higher reported EBITDA because interest and amortization are often excluded from the EBITDA calculation.

Example: How a Lease Appears on a Balance Sheet

Lease Capitalization Scenario

Suppose a company enters a 5-year equipment lease where the present value of its future payments is $50,000. The initial impact on its balance sheet is:

Assets:

- Right-of-Use Asset: +$50,000 (Non-Current Asset)

Liabilities:

- Lease Liability: +$50,000 (Split between current and non-current portions)

Equity:

- No immediate change. Equity is reduced over time as lease expenses are recognized on the income statement.

This single transaction significantly increases the company’s reported assets and liabilities, making it appear more leveraged.

Q · 01What is Leases?+