A detailed guide to the long-term portion of lease liabilities on the balance sheet, including historical and current accounting treatments under ASC 842 and IF

In the short run, the market is a voting machine. In the long run, it is a weighing machine.

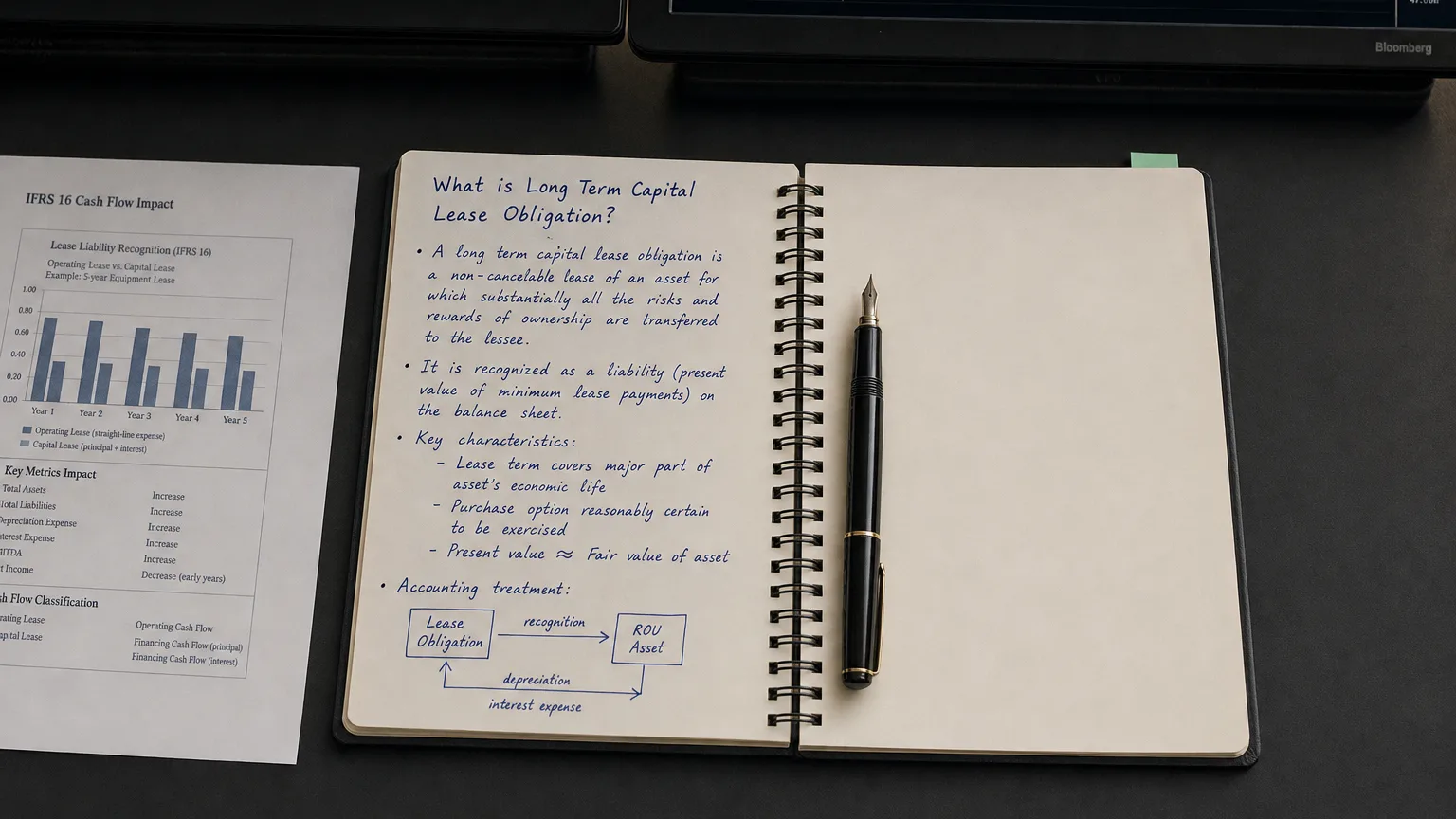

A Long-Term Capital Lease Obligation is a liability representing the portion of payments owed under a capital (or finance) lease contract that is payable beyond one year from the balance sheet date. This obligation arises when a lease is economically equivalent to a financed asset purchase. It is treated much like long-term debt, carrying an interest component and often being grouped with other debt for analysis. The portion due within the next year is classified as a short-term liability, while the remainder is shown as this long-term liability.

Historical Accounting Treatment (Pre-ASC 842 / IFRS 16)

Under older accounting standards, only leases meeting specific criteria were capitalized. Under U.S. GAAP (ASC 840), a lease was classified as a capital lease if it met any of four ‘bright-line’ tests:

- Transfer of Ownership: Ownership transferred to the lessee at the end of the lease.

- Bargain Purchase Option: The lessee could buy the asset at a price well below fair value.

- Lease Term: The lease term was for 75% or more of the asset’s estimated economic life.

- Present Value of Payments: The present value of payments was 90% or more of the asset’s fair value.

If none of these were met, it was an operating lease, which remained off-balance sheet. This practice was criticized for lacking transparency about a company’s true obligations.

Current Accounting Treatment (ASC 842 and IFRS 16)

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.”

— Benjamin Graham, Author, The Intelligent Investor Security Analysis (1934)

Accounting standards implemented around 2019 now require nearly all leases to be recorded on the balance sheet to increase transparency.

U.S. GAAP (ASC 842)

Replaces ‘capital lease’ with ‘finance lease’. Leases are classified as either finance or operating. Critically, both types now result in a Right-of-Use (ROU) asset and a lease liability on the balance sheet. The main difference lies in how the expense is recognized on the income statement.

IFRS (IFRS 16)

Eliminates the operating lease classification for lessees entirely. All leases (with minor exceptions) are treated like finance leases, using a single accounting model. This results in an ROU asset and a lease liability on the balance sheet for all leases.

Balance Sheet Presentation and Measurement

A lease obligation appears on the balance sheet because it represents a liability (an obligation to make future payments) and creates an asset (the right to use the leased item).

The lease liability is initially measured as the present value of all future lease payments, discounted at the lease’s implicit interest rate or the lessee’s incremental borrowing rate. Over time, the liability is reduced by the principal portion of each payment, similar to a loan.

The total lease liability is split into two parts on the balance sheet:

- Current Portion: The amount due within the next 12 months, listed under Current Liabilities.

- Long-Term Portion: The remaining balance due after one year, listed under Non-Current Liabilities. This is the Long-Term Capital (or Finance) Lease Obligation.

Impact on Financial Ratios and Analysis

Bringing all lease obligations onto the balance sheet significantly affects key financial ratios:

- Leverage Ratios: Ratios like Debt-to-Equity and Debt-to-Assets increase because lease liabilities are now included with total debt, making companies appear more leveraged.

- Asset Turnover Ratios: Ratios like Fixed Asset Turnover () decline because the asset base (the denominator) is larger due to the addition of Right-of-Use assets.

- Profitability & Coverage Ratios: EBITDA increases because rent expense is replaced by interest and depreciation (which are excluded from EBITDA). However, Interest Coverage ratios can be negatively impacted because interest expense also increases. Net income is often lower in the early years of a lease due to higher front-loaded interest costs.

Q · 01What is Long Term Capital Lease Obligation?+