Capital lease obligations are balance sheet liabilities representing a lessee’s future payments on a finance lease — treated as debt, not operating expense. They split into current and long-term portions, raising a company’s reported leverage and total debt load.

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

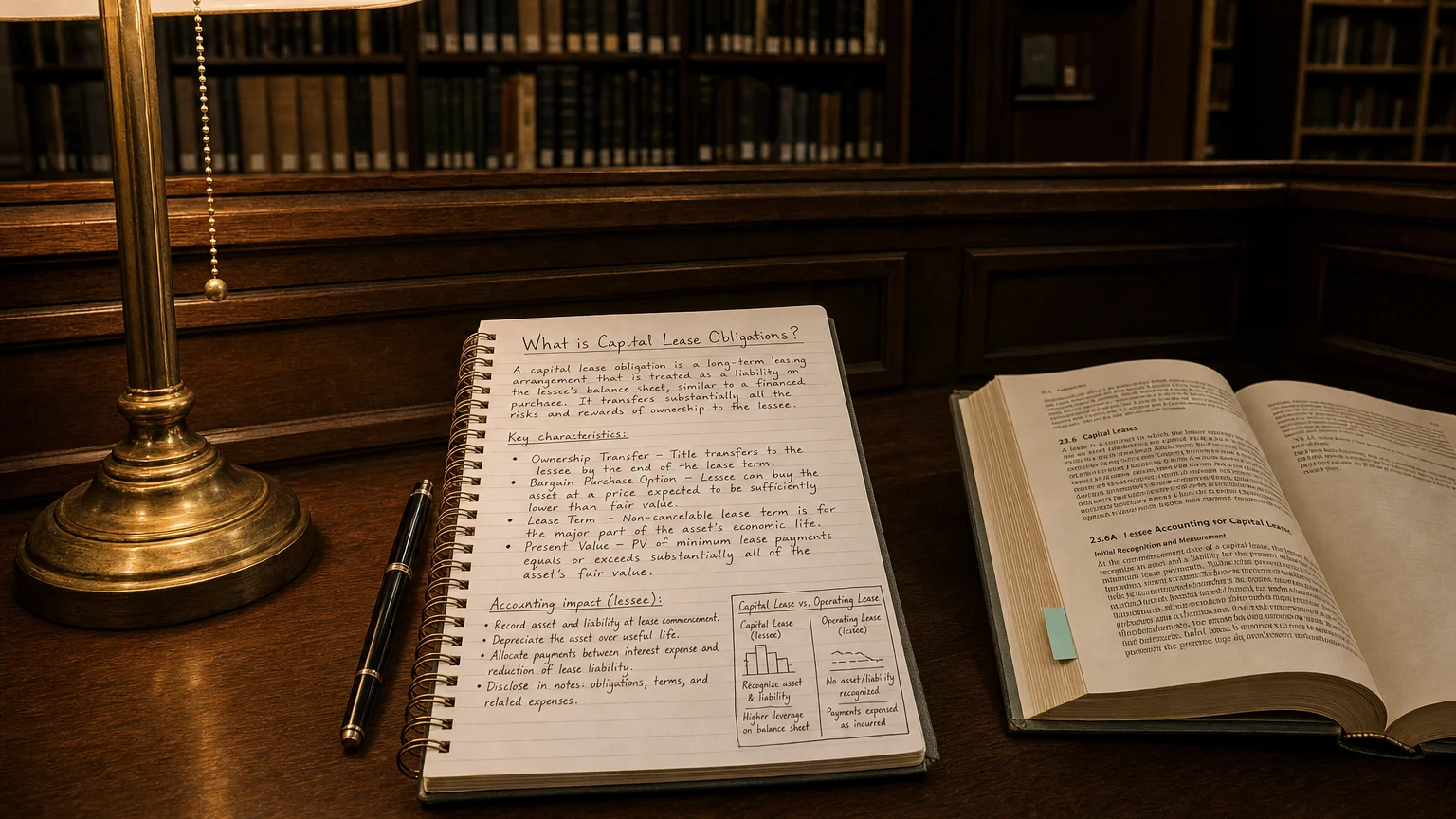

A capital lease (also known as a finance lease) is a lease contract that effectively transfers most of the risks and benefits of ownership of an asset from the lessor to the lessee. In accounting, Capital Lease Obligations refer to the liabilities recorded on a company’s balance sheet for such leases, representing the lessee’s commitment to make future lease payments. In essence, a capital lease is treated as if the company purchased the asset with debt financing - the leased asset is recorded as an owned asset, and the lease payments obligation is recorded as a liability.

Balance Sheet Presentation

On the balance sheet, capital leases impact both the asset and liability sections:

- Assets: The leased item is capitalized as a long-term asset. The company records the asset on its balance sheet (often under Property, Plant & Equipment or as a Right-of-Use asset) at an amount equal to the present value of lease payments. It is then depreciated over time.

- Liabilities: A corresponding Capital Lease Obligation (lease liability) is recorded. This liability equals the present value of the future lease payments and is typically split into a current portion (due within one year) and a long-term portion.

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

Key Characteristics (Capital vs. Operating Lease)

Under historical U.S. GAAP (ASC 840), a lease was classified as a capital lease if it met any one of the following four criteria:

- Transfer of Ownership: The lease transfers ownership of the asset to the lessee by the end of the term.

- Bargain Purchase Option: The lessee has an option to purchase the asset at a bargain price (substantially below fair market value).

- Lease Term Length: The lease term covers the majority of the asset’s useful life (typically 75% or more).

- Present Value of Payments: The present value of lease payments is substantially all of the asset’s fair value (typically 90% or more).

Update to Accounting Standards (ASC 842)

Under current standards (like ASC 842), the distinction has changed. The term ‘capital lease’ is now ‘finance lease’. More importantly, virtually all long-term leases (both finance and operating) must now be recorded on the balance sheet with a right-of-use asset and a lease liability. This enhances transparency by eliminating most ‘off-balance-sheet’ lease financing.

Importance for Financial Health

Capital lease obligations are important for understanding a company’s financial health because they reflect significant long-term commitments:

- Debt and Leverage: Capital lease obligations appear as debt on the balance sheet, increasing total liabilities and impacting leverage ratios like debt-to-equity. This provides a more accurate view of a company’s risk profile.

- Transparency of Obligations: Recognizing these leases on the balance sheet prevents companies from keeping significant commitments ‘off-balance sheet,’ ensuring investors see the full extent of fixed payment obligations.

- Cash Flow and Solvency: Lease payments are contractual obligations similar to loan repayments. A company’s ability to meet these payments is a key indicator of its liquidity and solvency.

- Asset Utilization: Recording the leased item as an asset allows stakeholders to evaluate how effectively it is used to generate revenue, similar to how they would analyze owned assets.

Common Assets Involved in Capital Leases

Capital leases are often used to finance high-value, long-lived assets. Common examples include:

- Heavy Equipment and Machinery: Expensive industrial assets like manufacturing machinery, construction equipment, or medical devices.

- Real Estate: Long-term leases of buildings, warehouses, or retail store locations.

- Vehicles and Aircraft: Company vehicle fleets, commercial airplanes, or specialized transportation equipment.

- Technology Infrastructure: High-cost technology like telecom equipment or large data-center hardware.

Q · 01How do capital lease obligations affect a company’s debt ratios?+

Q · 02What is the difference between a capital lease and an operating lease?+

Q · 03Are capital lease obligations included in total debt calculations?+