Dividends Received Direct is a financial concept covered in this article. Cash Dividends from Investments in Direct Method Operating Activities

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

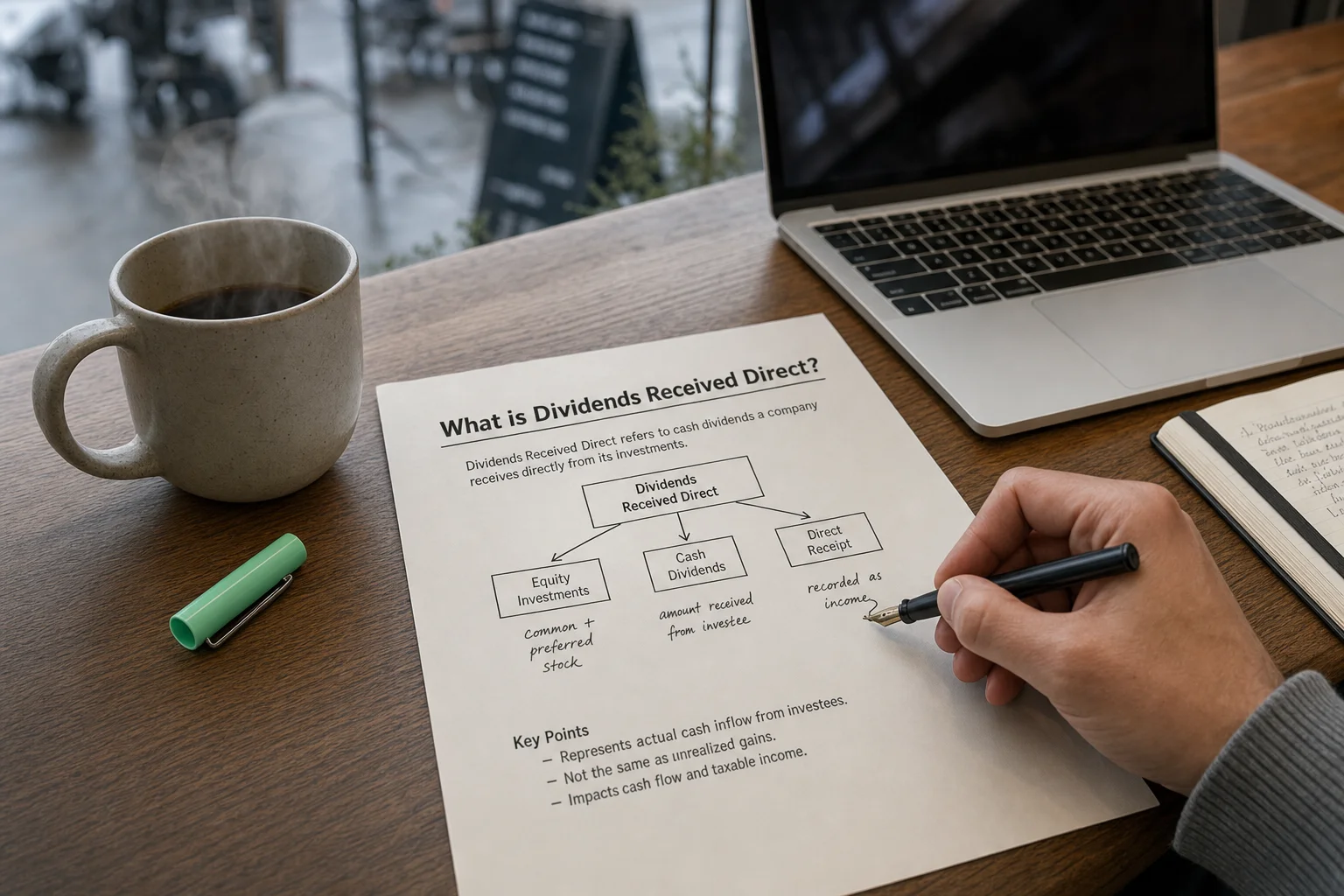

Dividends Received Direct is the actual cash inflow from dividends distributed by equity investments (associates, joint ventures, or other holdings) that is explicitly reported as a gross cash receipt in the direct method presentation of operating cash flows. This line treats dividend income as a core operating cash inflow, providing clear visibility on cash returns from strategic investments.

What It Represents

Dividends Received Direct shows the real cash coming in from dividend payments on equity stakes.

In the direct method, major operating cash receipts are listed gross, so dividends get their own line when significant.

Indirect method hides this in net income or supplemental notes—no gross view.

Common Sources

- Dividends from equity-method associates or joint ventures

- Dividends from other long-term equity holdings

- Distributions from investment funds or partnerships

- Dividend income from strategic minority stakes

Companies with significant equity investments show meaningful amounts.

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

A Practical Example

Company owns 30% of PartnerCo.

- PartnerCo declares $20M dividend

- Company receives $6M cash

- Direct method: ‘Dividends Received Direct’ +$6M

- Clear visibility on cash return from investment

Shows actual cash timing vs. equity-method earnings recognition.

Direct Method Context

In direct method operating section:

- Cash receipts from customers

- Dividends Received Direct

- Interest Received Direct

- Other operating receipts

- Minus payments to suppliers, employees, etc.

- = Net operating cash flow

Gross transparency—see dividend cash separate.

Why It Matters

- Actual cash return from equity investments

- Timing differences vs. equity earnings

- Contribution to operating cash

- Better insight for companies with strategic stakes

- Comparability challenge (most use indirect)

What to Watch For

- Growth vs. equity investment balance

- Cash yield on investments

- Seasonality or lumpiness (declaration timing)

- Link to investee profitability

- Comparison to equity-method earnings

Lower cash vs. earnings may signal low payout by investee.