Investments in Associates at Cost is a financial concept covered in this article. Holding Significant Stakes Without Adjusting for Ongoing Profits or Losses

I don't want a lot of good investments; I want a few outstanding ones.

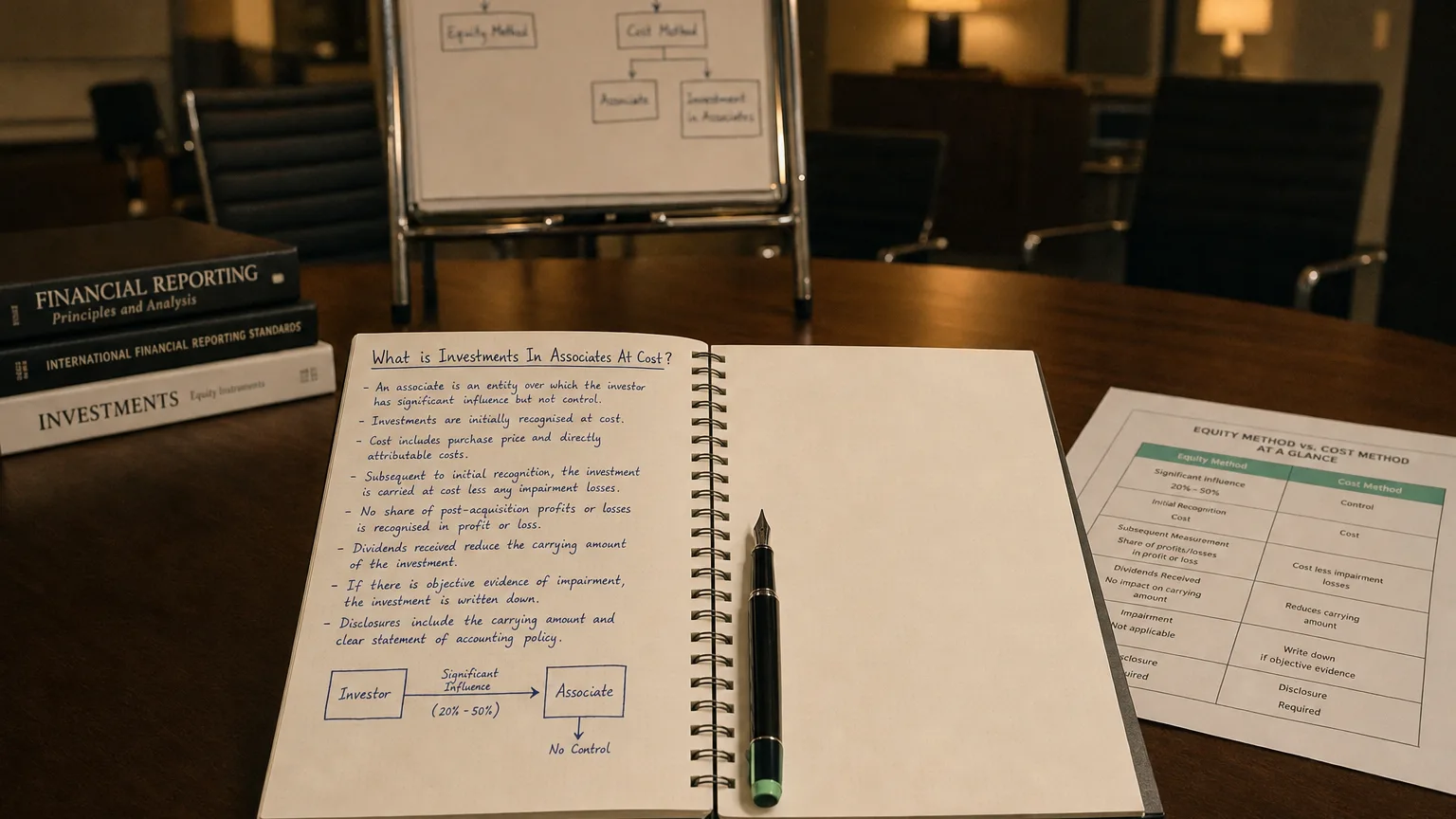

Investments in Associates at Cost means you own a meaningful chunk of another company—enough for significant influence, usually 20-50%—but you keep the investment on your books at what you originally paid, rather than tweaking it each year for your share of their earnings. This simpler approach is used in specific situations, like when you’re a venture capital firm or when fair value is hard to pin down.

When You’d See This Instead of Equity Method

Normally, if you own 20-50% of a company, you use the equity method—your investment goes up and down with their profits and dividends. But sometimes companies stick with plain cost accounting.

The main reasons: you’re a venture capital or private equity investor who elects fair-value-like treatment (IFRS allows this), the stake is immaterial, or reliable ongoing info is tough to get.

“I don’t want a lot of good investments; I want a few outstanding ones.”

— Philip Fisher, Author, Common Stocks and Uncommon Profits Common Stocks and Uncommon Profits (1958)

A Real-Life Example to Make It Clear

Say a big retail chain buys 25% of a logistics startup for $20 million. That stake gives them a board seat and real say in strategy—a classic associate.

- If they used equity method: Year 1 the startup makes 2M to investment and books 22M.

- But with cost method: Investment stays frozen at 4M dividend → retailer gets 1M income, investment still $20M.

The books look calmer—no swinging with the startup’s ups and downs—but you miss seeing the growing (or shrinking) economic value.

VC firms love this because their portfolio companies can be wildly profitable on paper without forcing income recognition before an exit.

How the Numbers Move (or Don’t)

- Start at what you paid (cost)

- Add nothing for profits the associate earns

- Record dividend cash when received as income

- Only subtract if you get back more than cumulative earnings (return of capital)

- Test for impairment—if value clearly drops, write down (can’t write back up)

It’s simple bookkeeping, but it can make the investment look stale compared to reality.

Where It Shows Up

You’ll spot it under non-current assets, often labeled:

- ‘Investments in Associates at Cost’

- ‘Cost-Method Investments in Associates’

- Sometimes just rolled into broader ‘Long-Term Investments’

Notes will list the associate names, your ownership %, and maybe summarized financials.

Who Uses This and Why

- Venture capital and private equity funds (avoid volatility before exits)

- Investment companies electing fair value options (IFRS)

- Holding companies with many small associates

- Cases where equity-method data is unreliable or costly to obtain

Regular operating companies almost always use equity method—cost is the exception.

What It Means When You See It

- Income statement misses the associate’s ongoing performance

- Balance sheet understates (or overstates) true economic value

- Less volatility quarter-to-quarter

- Big gap possible between book value and real worth

- Often flags a portfolio-style or financial investor

A 50M+—but your books won’t show it until sale or impairment.

Q · 01What is Investments In Associates At Cost?+