is a financial concept covered in this article. Cost-Method Accounting for Joint Venture Investments

Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.

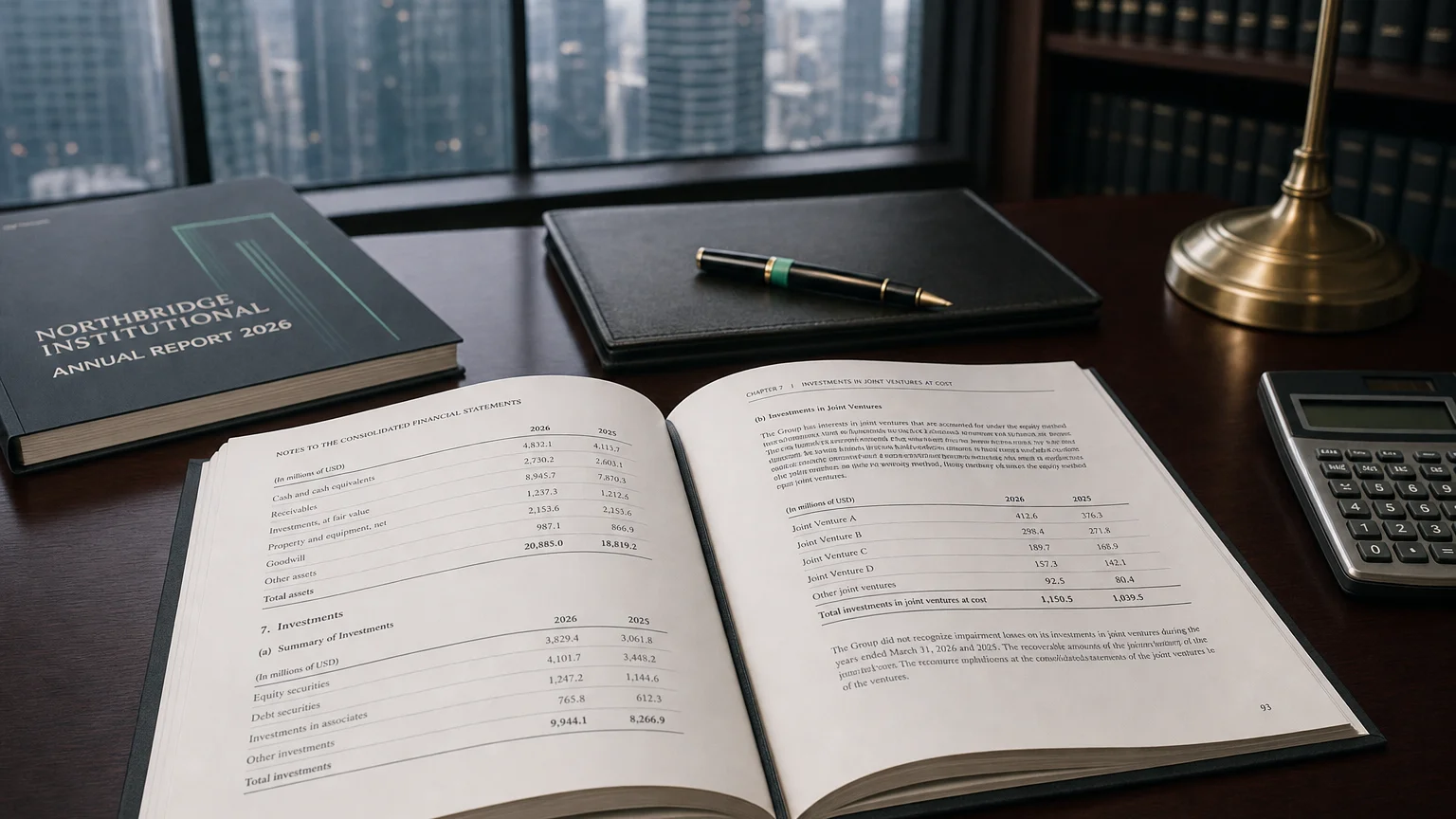

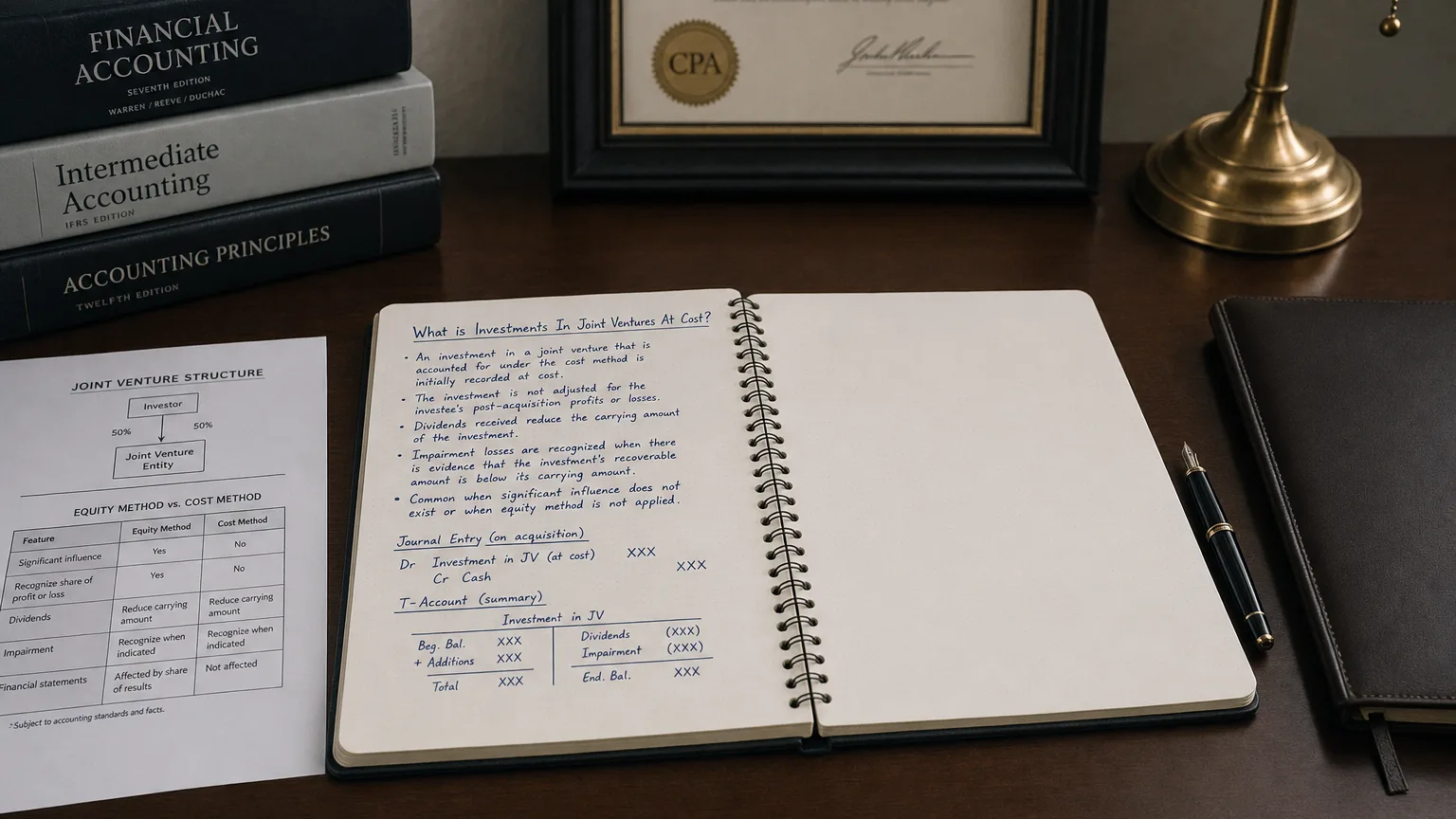

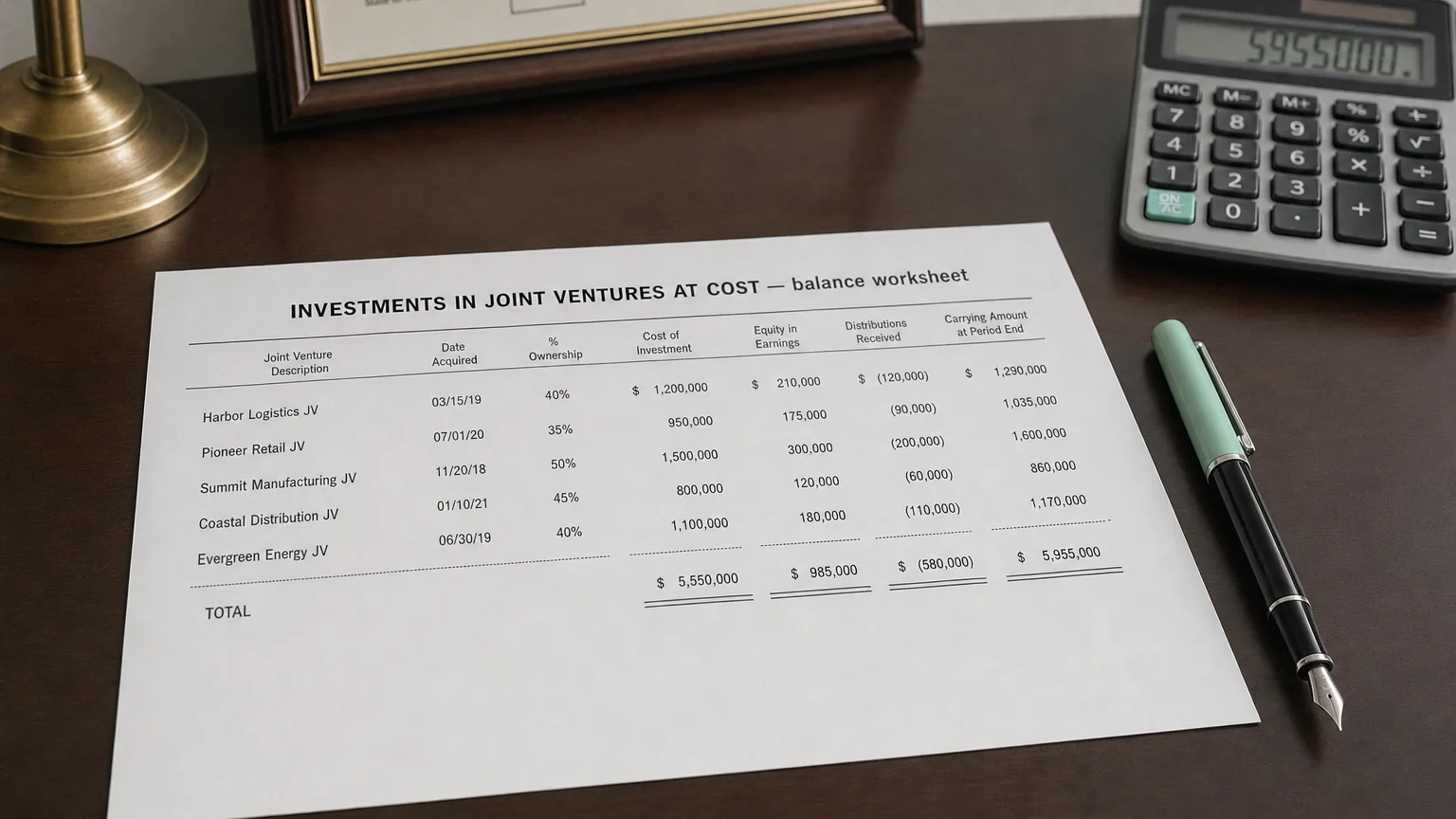

Investments in Joint Ventures at Cost refers to investments in joint ventures (entities under joint control) that are accounted for using the cost method rather than the more common equity method. This occurs when the investor does not have significant influence (or the JV is not material), or under specific standards/electives (e.g., certain IFRS options for venture capital entities). The investment is carried at historical cost (or impaired cost) on the balance sheet.

What Is a Joint Venture?

A joint venture (JV) is an entity jointly controlled by two or more parties (venturers) under a contractual arrangement. Control requires unanimous consent on key decisions.

Normally accounted for using the equity method (investor recognizes share of JV profits/losses).

Cost method is an exception—used when equity method not required/applicable.

“Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

When Cost Method Is Applied

- Venture capital, mutual funds, or investment companies elect fair value (IFRS) or cost (rare)

- Investor lacks significant influence despite JV structure

- JV held for sale (IFRS 5)

- Immaterial investment

- Certain unlisted JVs where fair value not reliably measurable (legacy)

Under US GAAP, joint ventures almost always use equity method.

Accounting Treatment (Cost Method)

- Initial recognition at cost (cash + fair value of assets contributed)

- Carried at cost less accumulated impairment

- No adjustment for post-acquisition JV profits/losses

- Dividends/distributions recognized as income (or return of capital if > earnings)

- Impairment tested if indicators exist (recoverable amount < carrying)

No share of JV OCI or comprehensive income recognized.

Balance Sheet Presentation

Under non-current assets as:

- ‘Investments in Joint Ventures at Cost’

- ‘Cost-Method Joint Ventures’

- Sometimes grouped in ‘Long Term Equity Investment’ or ‘Other Investments’

- Separate from equity-method investments

Footnotes disclose ownership %, nature of JV, and any commitments/restrictions.

Comparison with Equity Method

Cost Method

- Static carrying amount

- Income only from distributions

- Simpler accounting

Equity Method

- Adjusted for share of profits/losses

- Reflects economic performance

- More informative

Analytical Implications

Cost-method JV investments:

- Understate investor’s economic interest (no profit share)

- Hide JV performance and volatility

- May indicate immateriality or special-purpose entity

- Distributions provide limited income visibility

- Impairment risk if JV struggles

Large cost-method JVs may obscure significant off-balance exposure.

Q · 01What is Investments In Joint Ventures At Cost?+