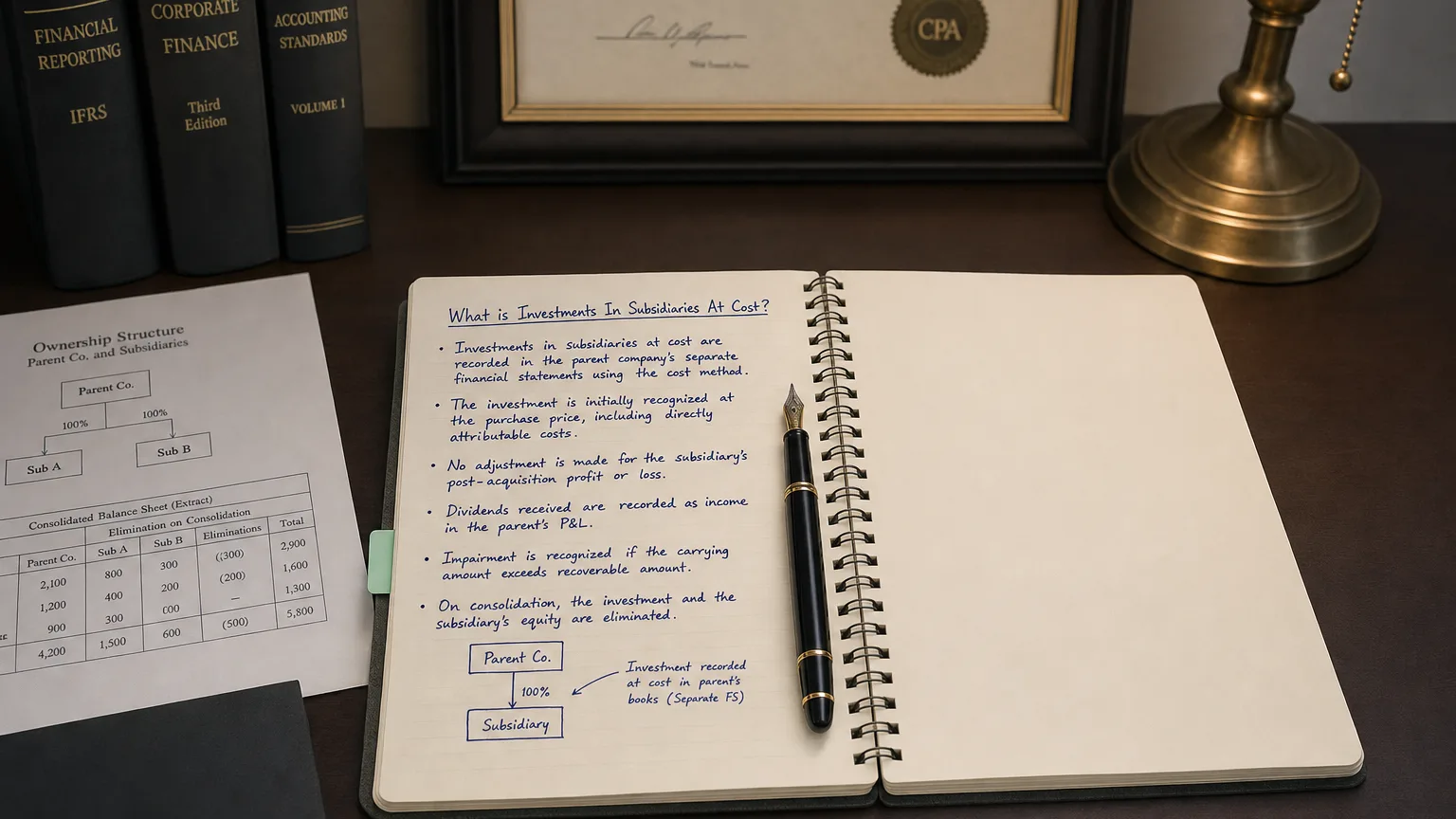

is a financial concept covered in this article. Parent-Only Accounting for Controlled Entities in Separate Financial Statements

Survival comes first, truth, understanding, and science later.

Investments in Subsidiaries at Cost shows up in a parent company’s standalone (separate) financial statements when it records its ownership in subsidiaries simply at the original purchase price or cost, instead of consolidating them or using the equity method. Even though the parent controls these companies (usually >50% ownership), separate statements often keep things simple by treating the investment like a fixed asset held at cost.

Why Separate Statements Use Cost Method

In the big consolidated group accounts, you see 100% of every subsidiary’s assets, liabilities, and profits. But many countries require or allow a parent company to publish its own solo financials. In those solo statements, the parent treats its subsidiaries like any other long-term investment.

Keeping them at cost makes the parent’s own balance sheet clean and focused on what it directly owns, without all the detail from dozens of subs.

“Survival comes first, truth, understanding, and science later.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Skin in the Game: Hidden Asymmetries in Daily Life (2018)

A Quick Example to See the Difference

ParentCo buys 100% of SubCo for $50 million cash.

- In consolidated statements: You add all of SubCo’s assets/liabilities line-by-line, eliminate the $50M investment, and show group totals.

- In ParentCo’s separate statements: You just show ‘Investment in Subsidiary’ at $50 million. No SubCo details appear.

Later, SubCo earns 4 million dividend to ParentCo.

- Consolidated: Group profit includes the full $10M.

- Separate (cost method): Investment stays 4M dividend as income, no share of the remaining profit.

The parent’s solo books stay simple and stable.

Only dividends hit income—big undistributed sub profits never show up.

How the Numbers Behave

- Start at cost (cash paid + fair value of anything else given)

- Stay at cost forever unless impaired

- Dividends received → income (or return of capital if excessive)

- Test for impairment if sub struggles (write down if needed, no write-ups)

- No adjustment for sub’s ongoing profits/losses

It’s quiet accounting—the balance rarely moves.

Where You’ll Spot It

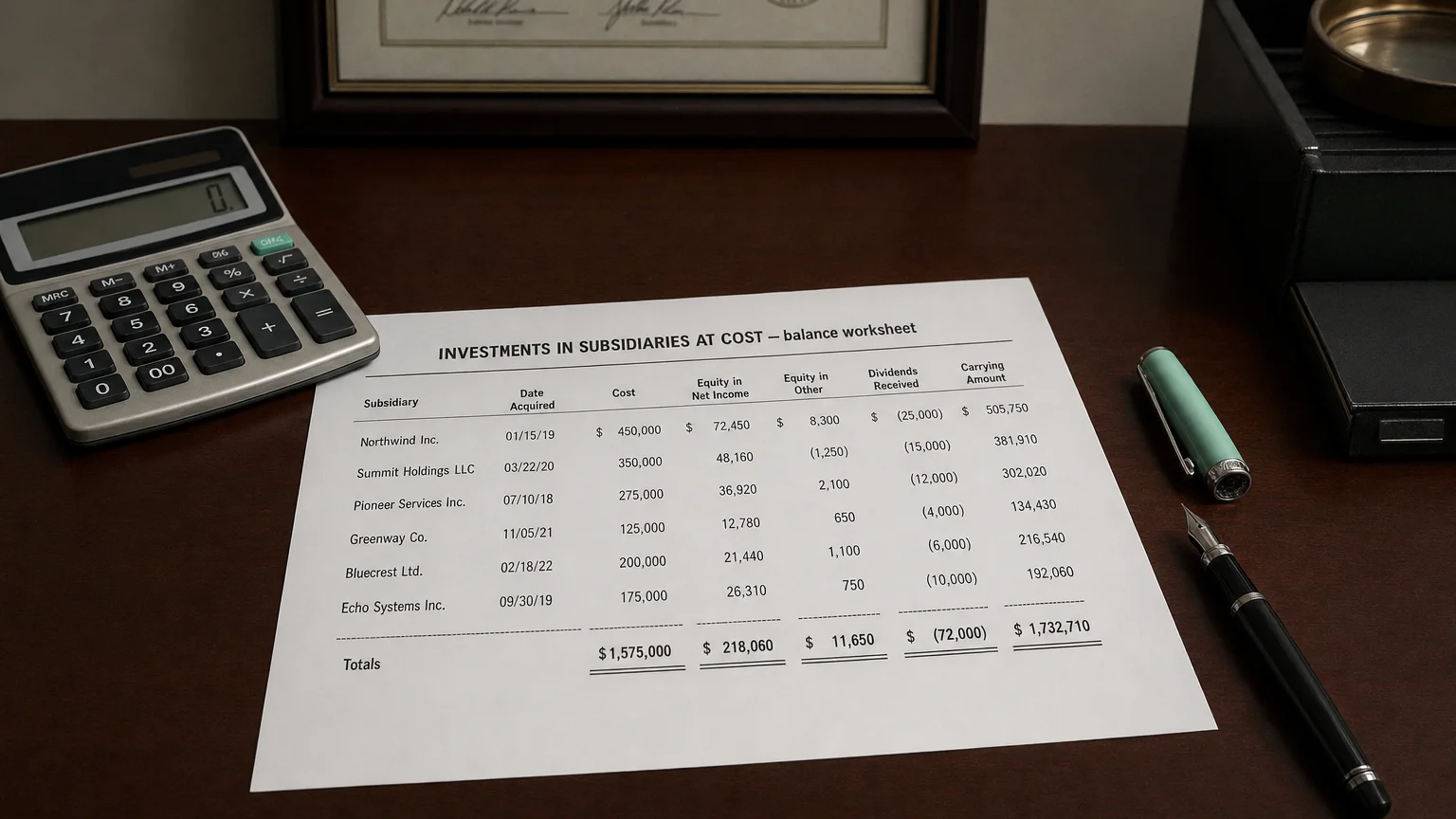

In the parent-only balance sheet under non-current assets:

- ‘Investments in Subsidiaries at Cost’

- ‘Investment in Controlled Entities’

- Often the biggest single asset for holding companies

Notes list each subsidiary, ownership %, and sometimes summarized financials.

Who Uses This Approach

- Holding companies with many subs

- European parents under IFRS (IAS 27 allows cost or equity method in separates)

- Private companies filing local parent-only statements

- Groups where consolidated view is primary, solo is legal requirement

US GAAP public companies rarely show separate statements, so you see this more in international filings.

What It Tells You (and What It Hides)

- Clean view of parent’s direct position

- Historical cost of building the group

- Dividend flow from subs to parent

- But hides sub growth/value creation until dividends or sale

- Impairment charges can appear suddenly if sub falters

A 200M from sub growth—but cost method won’t show it.

Q · 01What is Investments In Subsidiaries At Cost?+