Investments in Other Ventures Under Equity Method is a financial concept covered in this article. Accounting for Stakes with Significant Influence but Not Full Control

You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.

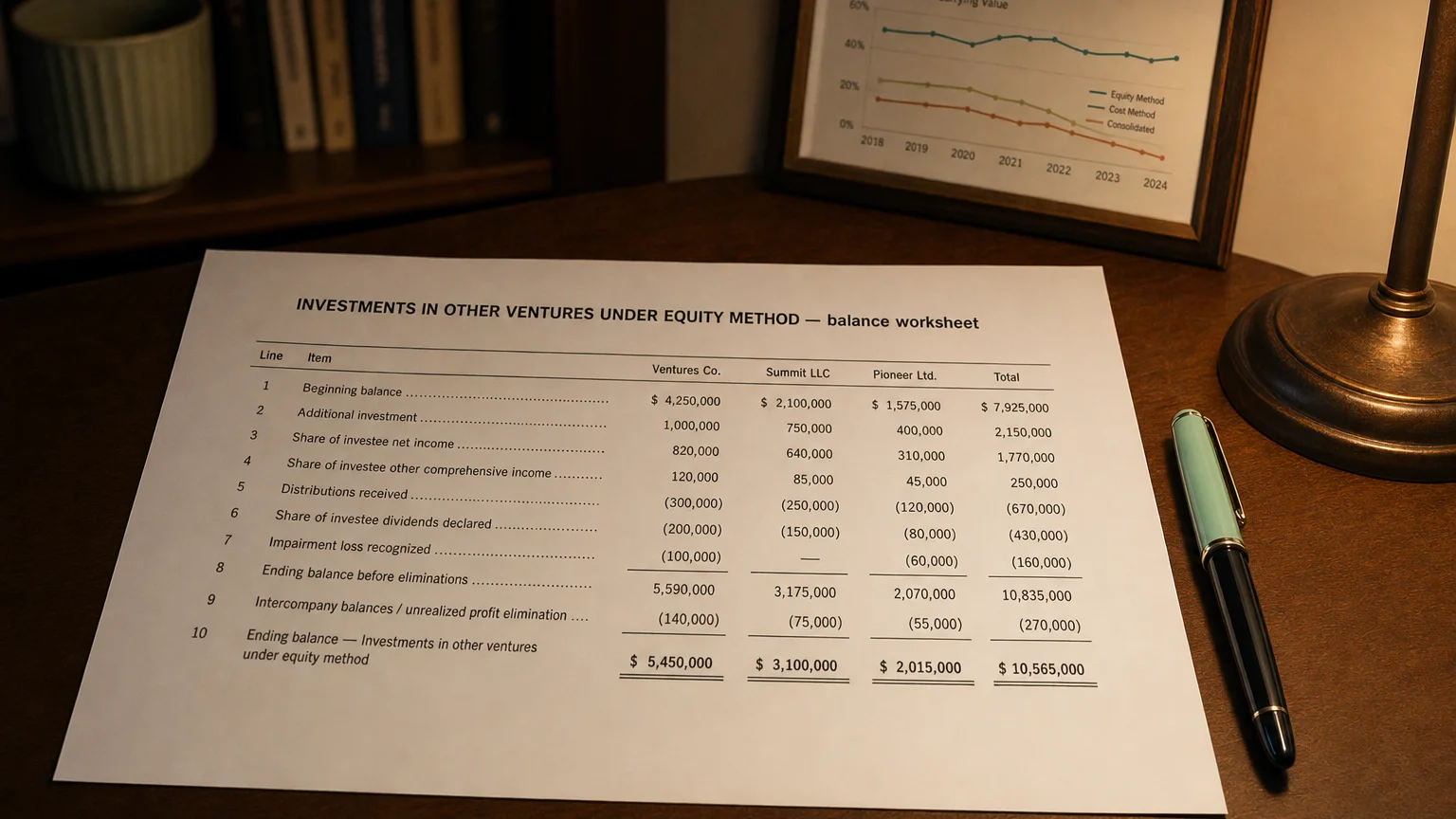

Investments in Other Ventures Under Equity Method covers ownership stakes in companies where you have significant influence—usually 20% to 50% of voting shares—but not outright control. Instead of just sitting at cost or fair value, the investment moves up or down each year based on your share of the venture’s profits or losses. It’s a way to show the real economic tie you have without consolidating the whole company onto your books.

Why the Equity Method Exists

When you own enough of another company to sway its decisions but not run it completely, plain cost accounting would hide what’s really happening. The equity method fixes that by letting your investment balance reflect your portion of the venture’s success or struggles.

Think of it as a middle ground: you don’t consolidate (which would add 100% of their assets and debts), but you also don’t treat it like a passive stock holding.

“You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

How It Works – A Simple Example

Imagine you invest $10 million for a 30% stake in TechCo, a growing software firm.

- Year 1: TechCo earns 1.5 million. You add 11.5M) and record $1.5M income.

- TechCo pays 600k cash received. You subtract 10.9M).

- Year 2: TechCo loses 900k loss. Reduce investment to $10M and record the loss.

Your books now show the real economic exposure: the investment grows with profits and shrinks with losses or dividends.

Dividends aren’t income—they’re just returning part of your original investment.

Key Mechanics

- Start at cost (what you paid)

- Add your share of venture’s post-acquisition earnings

- Subtract your share of dividends/distributions

- Adjust for your share of other comprehensive income items

- Test for impairment if signs of value drop

No upward adjustments beyond your share of profits unless basis differences (like fair value step-ups) amortize.

Where It Shows Up

On the balance sheet, you’ll see a line under non-current assets like:

- ‘Investments in Other Ventures Under Equity Method’

- ‘Equity Method Investments’

- ‘Investments in Associates’

Income statement shows ‘Share of profit/loss from equity-method investments’—often below operating income.

Real-World Situations

- A beverage giant owning 30% of a bottling partner

- An oil company with 25% in an exploration joint venture

- A retailer holding 40% of a logistics provider

- Tech firms taking meaningful minority stakes in suppliers or startups

These stakes give strategic input—board seats, supply priority—without full consolidation complexity.

What to Watch For

- Earnings from equity investments can be non-cash—check if venture actually pays dividends

- Large balances mean hidden exposure to the venture’s risks

- Impairments hit hard and suddenly

- Related-party flavor: transactions with the venture need scrutiny

- Growth in line item often signals active partnership strategy

Equity-method income boosts reported profit but may not translate to cash—always look at the venture’s dividend policy.

Q · 01What is Investments In Other Ventures Under Equity Method?+