Loss Adjustment Expense is a financial concept covered in this article. Costs Incurred to Investigate and Settle Insurance Claims

It does not matter how frequently something succeeds if failure is too costly to bear.

Loss Adjustment Expense (LAE) represents the costs an insurance company incurs to investigate, evaluate, adjust, and settle claims made by policyholders. These expenses include salaries and fees for internal adjusters and external experts, legal defense costs, appraisal fees, and other administrative expenses directly tied to claim handling. LAE is a critical component of an insurer’s underwriting expenses and is typically divided into allocated (directly assignable to specific claims) and unallocated (general overhead). High LAE can erode profitability, while efficient management improves the combined ratio and overall underwriting performance.

What is Loss Adjustment Expense?

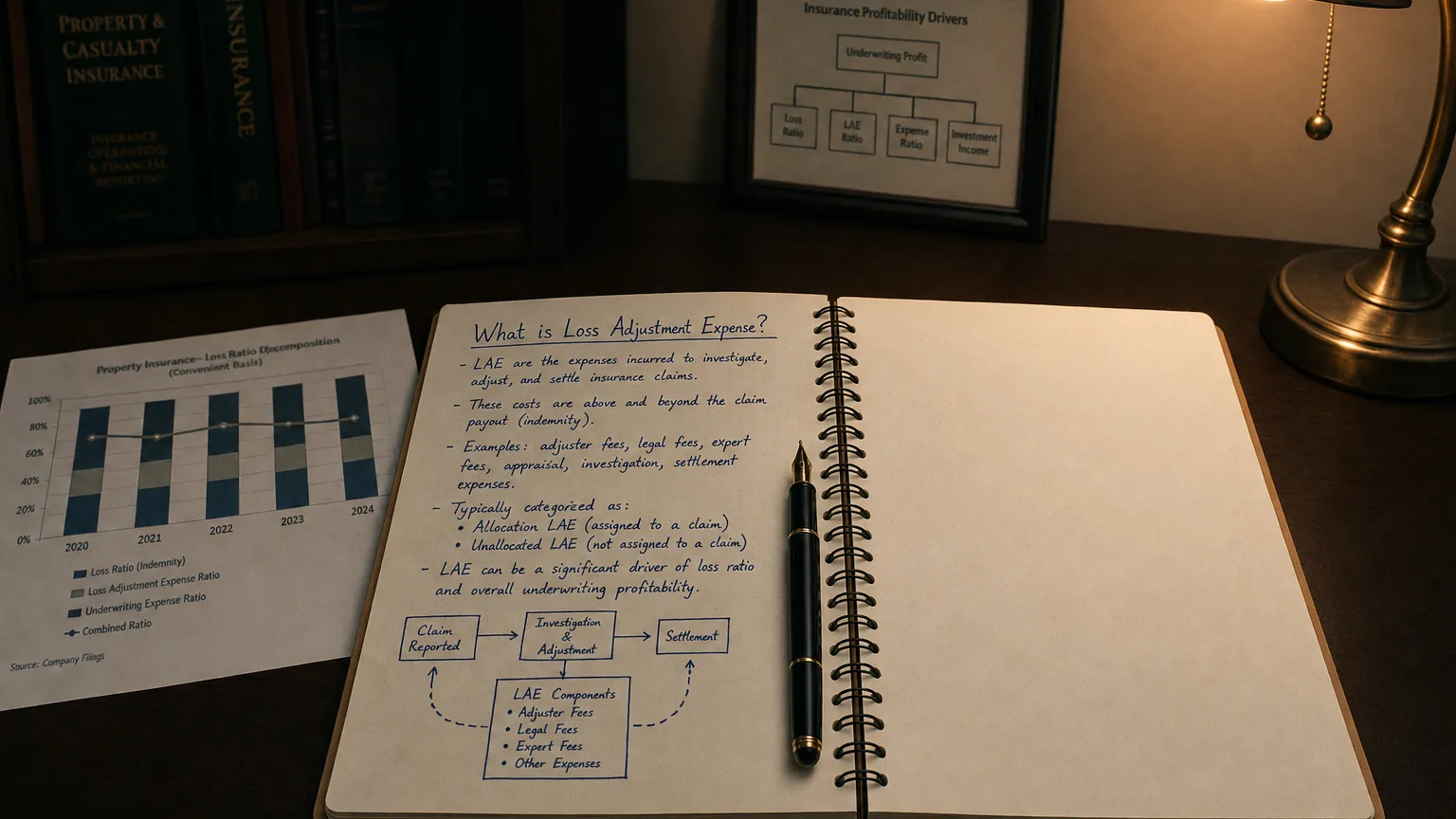

Loss Adjustment Expense (LAE) encompasses all costs associated with processing and settling insurance claims, separate from the actual claim payments (losses) themselves.

Under US GAAP (ASC 944) and IFRS (IFRS 17/4), LAE is an operating expense for insurers, typically classified within underwriting expenses. It is crucial for calculating the loss ratio (losses/premiums) and expense ratio (underwriting expenses/premiums), which combine into the combined ratio.

Efficient LAE management (e.g., through technology or in-house adjusters) improves profitability; high LAE often signals complex claims or inefficiencies.

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness (2001)

LAE is material in property & casualty (P&C) insurance; less so in life/health.

Types of Loss Adjustment Expense

LAE is commonly divided into two categories:

LAE Breakdown

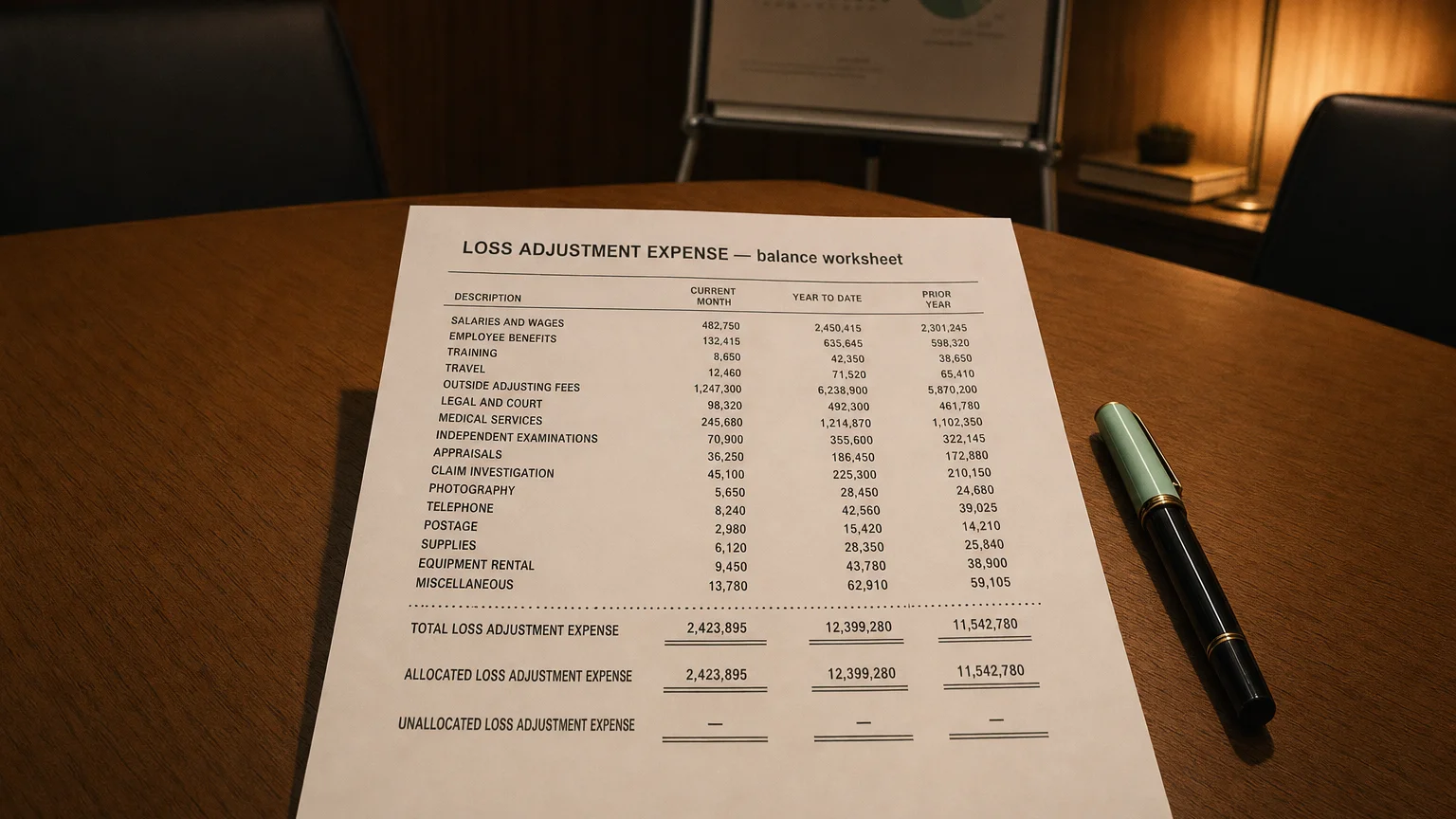

- Allocated Loss Adjustment Expense (ALAE): Directly attributable to specific claims (e.g., external adjuster fees, legal defense, appraisals)

- Unallocated Loss Adjustment Expense (ULAE): General overhead not tied to individual claims (e.g., internal adjuster salaries, office costs)

Regulators and analysts often track ALAE separately as it correlates with claim complexity.

How LAE Appears in the Income Statement

For insurance companies:

Formula: Underwriting Expenses = Loss Adjustment Expenses

- Acquisition Costs (commissions)

- Other Underwriting Expenses

LAE is expensed as incurred (or accrued for IBNR-related) and reduces underwriting income.

Tip: Combined Ratio = (Losses + LAE + Other UW Expenses) ÷ Earned Premiums; <100% = underwriting profit.

Examples

Example 1: Property & Casualty Insurer

Earned premiums: $2B

Claim payments: 150M ULAE (internal staff/overhead): 250M LAE Ratio = 2B = 12.5%.

Example 2: Catastrophe Event

Major hurricane triggers surge in claims.

Extra external adjusters: +30M ULAE Incremental LAE: $110M (spikes expense ratio temporarily).

Complex lines (liability, workers’ comp) have higher LAE ratios (15-25%).

Importance in Financial Analysis

Analysts track LAE to:

- Evaluate claim handling efficiency (lower LAE = better)

- Assess reserve adequacy (high ALAE may signal under-reserving)

- Calculate combined ratio components

- Compare operational leverage across insurers

Rising LAE without premium growth erodes underwriting margins; technology (AI adjusters) aims to reduce it.

Warning: Catastrophes or litigation waves can cause volatile LAE spikes—normalize for underlying trends.

Q · 01What is Loss Adjustment Expense?+