Policy Holder Benefits Gross is a financial concept covered in this article. Total Insurance Benefits and Claims Before Reinsurance Recoveries

Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.

Policy Holder Benefits Gross represents the total amount of benefits, claims, and reserves an insurance company recognizes for policyholders before deducting any recoveries from reinsurance arrangements. This gross figure includes actual claim payments, changes in loss reserves (including IBNR - Incurred But Not Reported), death benefits, annuities, surrenders, and other policy obligations across property & casualty (P&C), life, and health lines. Reported in the income statement as a primary cost of revenue for insurers, it reflects the full scale of underwriting risk before risk transfer via reinsurance. Comparing gross to net (after cessions) reveals reinsurance dependence and true risk retention.

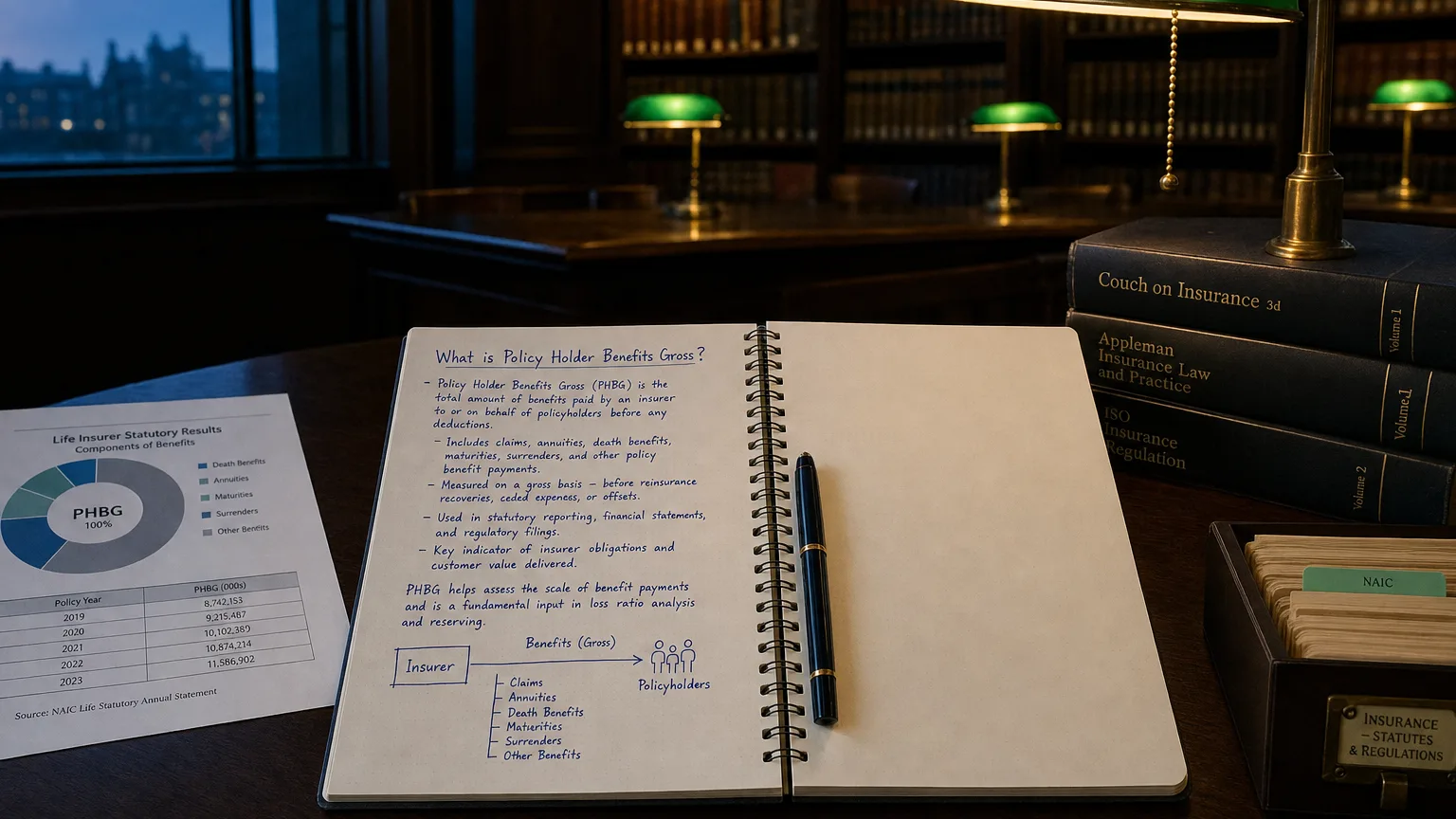

What is Policy Holder Benefits Gross?

Policy Holder Benefits Gross is the aggregate obligation an insurer records for policyholder claims and benefits prior to any offset from reinsurance recoveries.

Under US GAAP (ASC 944) and IFRS 17 (effective 2023), it includes all direct and assumed claims/benefits, plus changes in technical reserves. This gross view shows the full volume of risk underwritten before risk-sharing arrangements.

It is the starting point for calculating net policy holder benefits (gross minus ceded) and is essential for understanding gross underwriting exposure.

High gross benefits relative to premiums indicate adverse loss experience or reserve strengthening.

“Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Components of Gross Benefits and Claims

Major elements typically include:

Key Components

- Paid Claims: Actual settlements to policyholders

- Case Reserves: Known claims with estimated future payments

- IBNR Reserves: Incurred But Not Reported claims (actuarial estimate)

- Reserve Development: Prior year reserve releases (+) or strengthening (-)

- Life/Health Benefits: Death, maturity, annuity, surrender payments

- Policy Dividends: Participating policy returns

Excludes Loss Adjustment Expenses (LAE), which are separate.

Relationship to Net Benefits

Formula: Net Policy Holder Benefits = Gross Benefits & Claims − Ceded Recoveries − Change in Ceded Reserves

High reinsurance cessions reduce net benefits, lowering volatility but also premium retention.

Tip: Gross-to-net ratio reveals reinsurance strategy—low net/gross = heavy reinsurance dependence.

Examples

Example 1: P&C Insurer Normal Year

Gross claims paid: $5B

Gross reserve increase: 0.3B) Policy Holder Benefits Gross: 1.2B Net Benefits: $4.5B.

Example 2: Catastrophe Impact

Major storm year:

Gross claims paid: 3B Gross Benefits: 6B Net Benefits: $5B (reinsurance caps impact).

Example 3: Life Insurer

Death/surrender benefits: $4B

Annuity payments: 0.5B Gross Benefits: 2B Net: $5.5B.

Reserve releases from prior years can offset current claims, improving results.

Presentation in the Income Statement

For insurers:

Common Placement

- Cost of Revenue or Benefits and Losses line

- Separate Gross Claims Incurred or Policyholder Benefits

- Part of underwriting result calculation

Reduces gross underwriting income; net version used for combined ratio.

Importance in Financial Analysis

Analysts use gross benefits to:

- Assess full risk volume underwritten

- Evaluate reinsurance effectiveness (gross vs. net)

- Detect reserve adequacy (adverse prior year development)

- Compare gross loss ratios across peers

Spikes indicate catastrophe losses or reserve strengthening; consistent growth reflects premium volume.

Warning: Over-reliance on reinsurance (low net/gross) may hide underlying risk pricing issues.