Net Policy Holder Benefits and Claims is a financial concept covered in this article. Net Insurance Payouts to Policyholders After Cessions to Reinsurers

It is all about redundancy. Nature likes to overinsure itself.

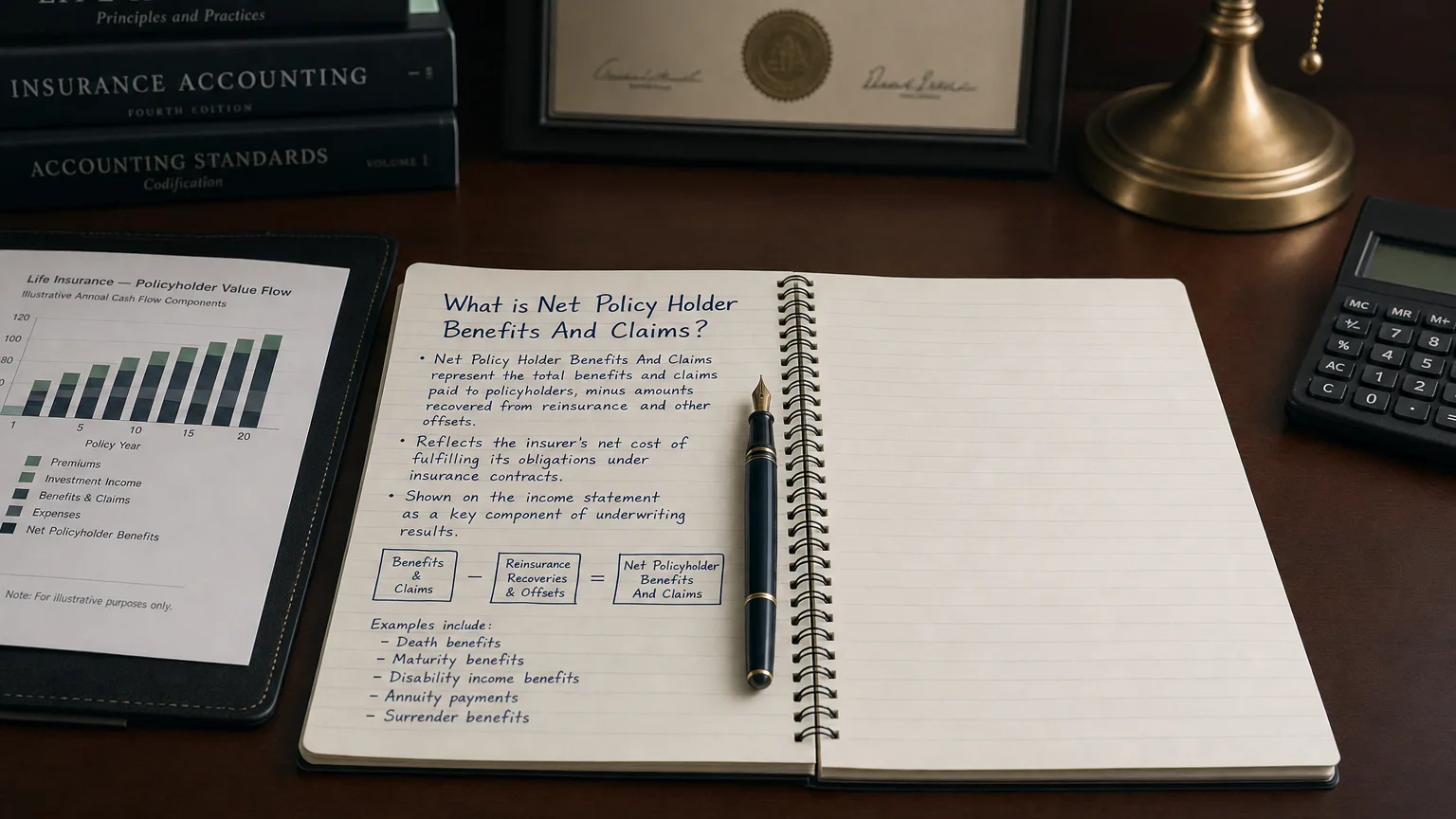

Net Policy Holder Benefits and Claims represents the net amount of insurance benefits and claims paid or reserved for policyholders after deducting amounts ceded (reinsured) to other insurers. This line item is central to insurance company income statements, capturing the core cost of fulfilling policy obligations in property & casualty (P&C), life, health, or other lines. It includes actual claim payments, changes in loss reserves (IBNR), and benefit annuities, net of reinsurance recoveries. High net claims pressure underwriting profitability, while efficient reserving and reinsurance management improves the loss ratio and combined ratio.

What is Net Policy Holder Benefits and Claims?

Net Policy Holder Benefits and Claims is the insurer’s net obligation to pay policyholders for covered losses or benefits, after reinsurance recoveries. It reflects the economic cost of risk transfer inherent in insurance operations.

Under US GAAP (ASC 944) and IFRS 17 (effective 2023), this line includes:

- Direct claim payments

- Increases/decreases in loss reserves (case reserves + IBNR)

- Life/health policy benefits (annuities, death benefits) Net of ceded amounts to reinsurers.

IBNR (Incurred But Not Reported) is a major reserve component—under-reserving leads to future charge-offs.

Calculation and Components

“It is all about redundancy. Nature likes to overinsure itself.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Antifragile: Things That Gain from Disorder (2012)

Formula:

Formula: Net Policy Holder Benefits and Claims = Gross Claims/Benefits − Ceded Reinsurance Recoveries

- Change in Net Loss Reserves

Breakdown

- Gross Claims: Direct payments for covered events

- Ceded: Reinsurer share reimbursed to primary insurer

- Loss Reserves: Estimated future payments (case + IBNR)

- Benefits (life/health): Maturities, surrenders, death benefits

Tip: Reinsurance reduces volatility but ceding commissions offset some expense savings.

Examples

Example 1: P&C Auto Insurer

Gross claims paid: $4B

Gross reserve increase: 800M Ceded reserve decrease: 4B + 800M + 4.4B Loss ratio ~70% on $6.3B net premiums.

Example 2: Life Insurer

Death benefits: $2B

Annuity payouts: 800M Reserve release: (1B Net: $3B (benefits net of reinsurance).

Catastrophes (hurricanes) cause spikes; reinsurance smooths impact.

Presentation in the Income Statement

For insurers:

Typical Placement

- Cost of Revenue or Benefits and Claims line

- Separate Net Policyholder Claims in detailed statements

- Part of Underwriting Expenses with LAE

Reduces underwriting income; key input to combined ratio.

Importance in Financial Analysis

Critical for:

- Loss Ratio (net claims ÷ net premiums; ideal 60-70%)

- Combined Ratio (<100% = underwriting profit)

- Reserve Adequacy (adverse development = under-reserving)

- Reinsurance Dependence (high cessions = risk transfer)

Rising net claims signal pricing inadequacy or catastrophe losses.

Warning: IBNR underestimation leads to ‘reserve strengthening’ charges—watch prior accident year development.