Policy Holder Benefits Ceded is a financial concept covered in this article. Benefits and Claims Transferred to Reinsurers for Risk Sharing

It is all about redundancy. Nature likes to overinsure itself.

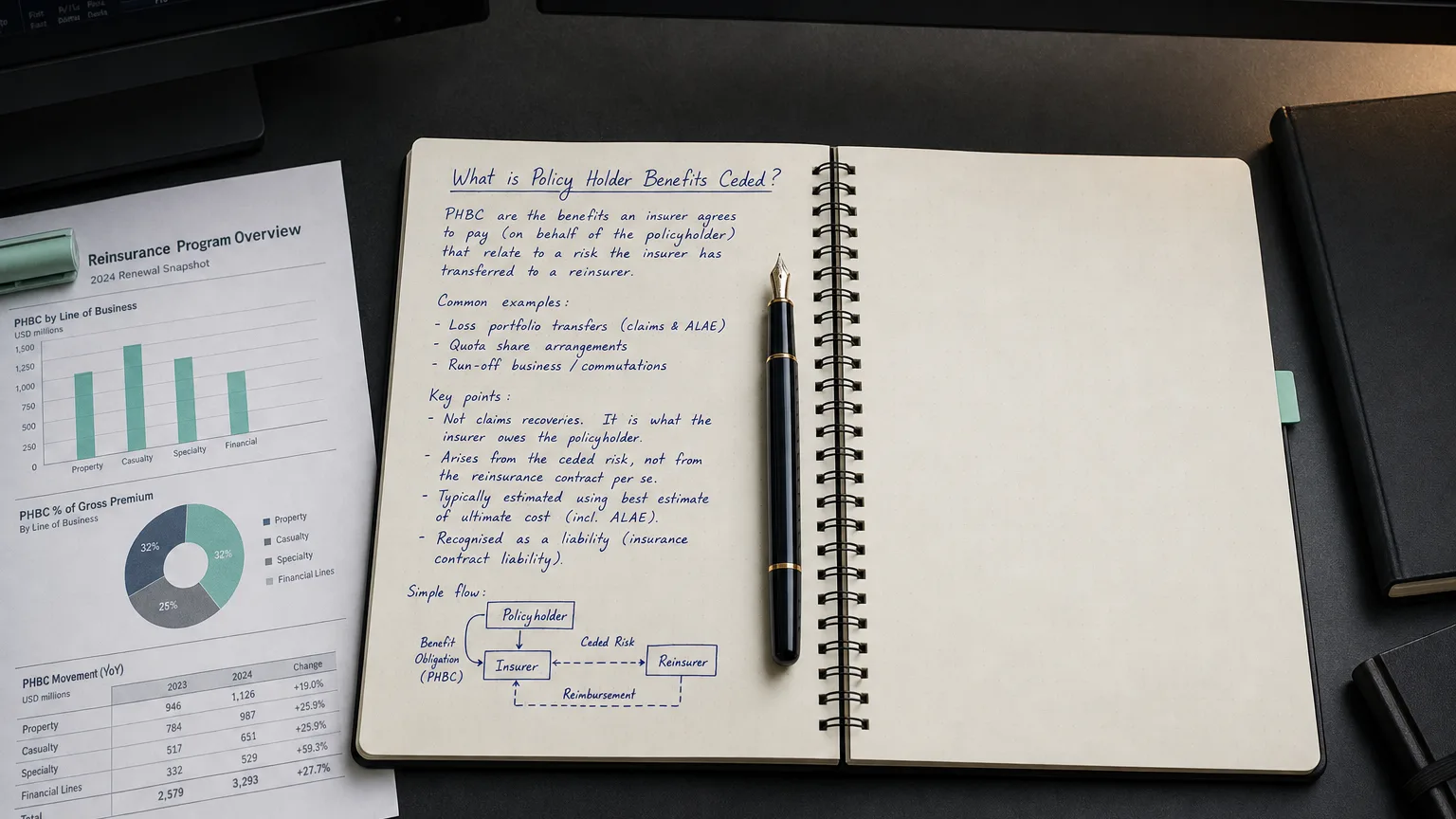

Policy Holder Benefits Ceded represents the portion of insurance claims, benefits, and loss reserves that a primary insurer transfers to reinsurance companies under reinsurance agreements. This amount is subtracted from gross policyholder benefits and claims to arrive at net figures, effectively reducing the primary insurer’s net exposure and volatility. Ceded benefits include proportional (quota share) and non-proportional (excess of loss) reinsurance recoveries for paid claims, reserve changes, and IBNR (Incurred But Not Reported). While ceding reduces risk and stabilizes earnings, it comes at the cost of ceding premiums, impacting net premium retention. This line is crucial for understanding reinsurance strategy, risk retention, and true economic loss experience.

What is Policy Holder Benefits Ceded?

Policy Holder Benefits Ceded is the share of gross insurance obligations (claims paid, benefits, and reserve changes) that the primary insurer recovers from reinsurers under reinsurance contracts.

Under US GAAP (ASC 944) and IFRS 17, ceded benefits are presented as a reduction to gross amounts, yielding net policyholder benefits and claims. This reflects the economic substance of risk-sharing arrangements.

Ceding is a core risk management tool—insurers cede to protect capital from large losses (catastrophes) or stabilize earnings across cycles.

High ceded benefits indicate heavy reinsurance reliance; low suggests greater risk retention.

“It is all about redundancy. Nature likes to overinsure itself.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Antifragile: Things That Gain from Disorder (2012)

Types of Reinsurance Affecting Ceded Benefits

Main reinsurance structures:

Key Types

- Proportional (Quota Share): Fixed % of all premiums and losses ceded (e.g., 30% share)

- Non-Proportional (Excess of Loss): Reinsurer pays above retention (e.g., losses > $10M)

- Catastrophe Reinsurance: Specific coverage for major events (hurricanes, earthquakes)

- Facultative: Per-risk reinsurance (large individual policies)

Ceded benefits mirror the structure—proportional yields steady recoveries; excess provides protection for tail risks.

Calculation and Relationship to Gross/Net

Formula: Net Policy Holder Benefits = Gross Benefits & Claims − Policy Holder Benefits Ceded

Ceded includes recoveries on paid claims and changes in ceded reserves (reinsurer share of IBNR/case reserves).

Tip: Ceding commissions (reinsurer pays primary for expenses) offset some premium cost but are separate.

Examples

Example 1: Proportional Reinsurance

Gross claims: $5B

30% quota share ceded. Policy Holder Benefits Ceded: 3.5B (stable across years).

Example 2: Catastrophe Event

Gross claims from hurricane: $8B

Excess of loss retention 7B Net claims: $1B (reinsurance caps impact).

Example 3: Reserve Development

Prior year gross reserves strengthened $500M.

Reinsurance covers 40%. Ceded increase: $200M (recovery reduces net charge).

Cat reinsurance often causes large ceded swings in disaster years.

Presentation in the Income Statement

For insurers:

Typical Placement

- Subtraction from Gross Policy Holder Benefits

- Separate Ceded Claims/Benefits line

- Footnote disclosure of gross, ceded, net

Reduces net underwriting expense; impacts loss ratio on net premiums.

Importance in Financial Analysis

Analysts examine ceded benefits to:

- Gauge risk retention (low ceded = higher risk/reward)

- Assess reinsurance efficiency (cost vs. protection)

- Evaluate earnings stability (high ceded = smoother results)

- Detect catastrophe exposure management

Rising ceded % may signal increasing risk or hardening reinsurance markets.

Warning: Over-ceding reduces profitability (premium giveaway); under-ceding exposes to volatility.