A guide to understanding consolidated equity, the role of non-controlling interests, and why this distinction is crucial for financial analysis.

You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.

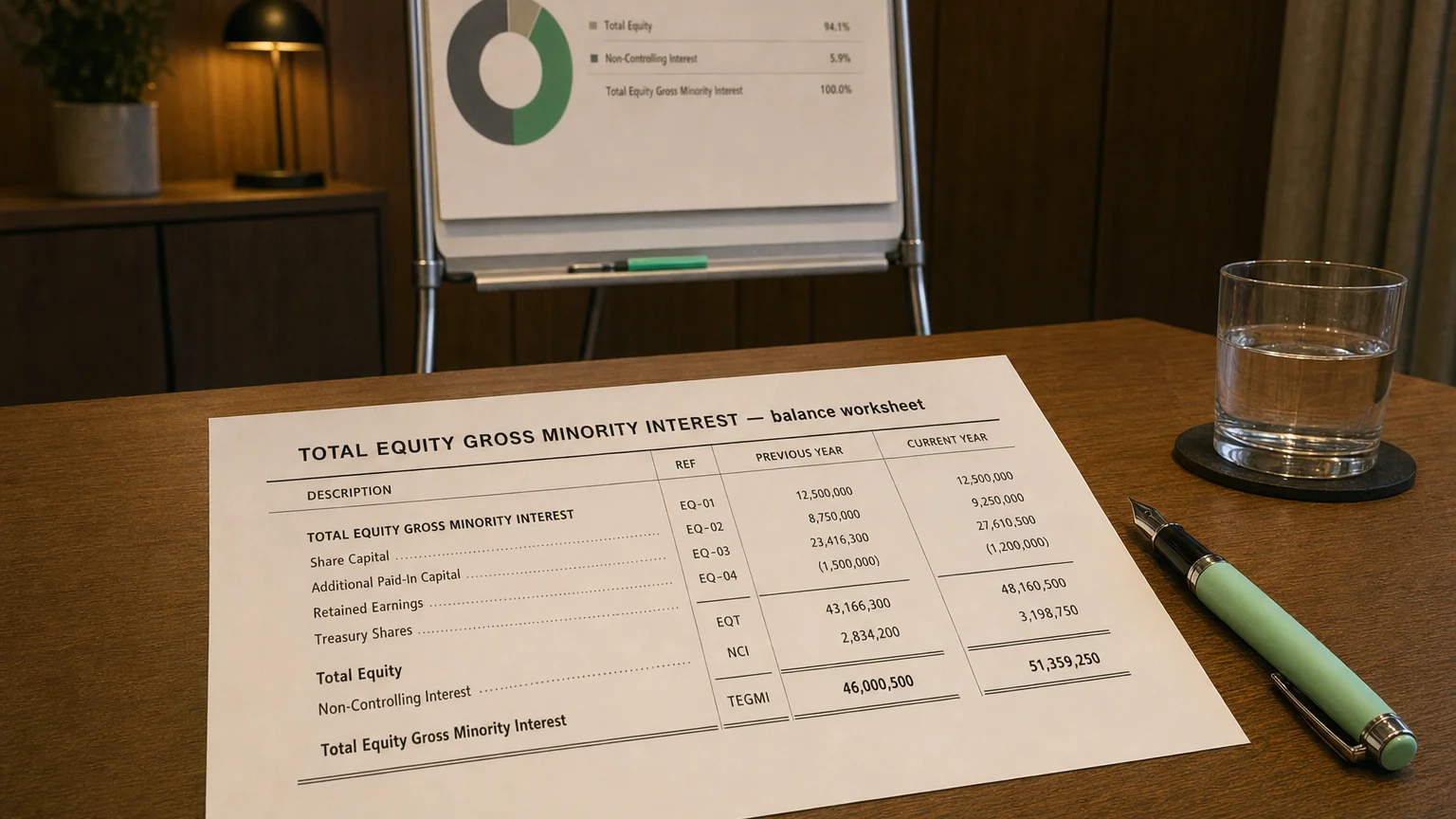

The term “Total Equity (Gross Minority Interest)” on a consolidated balance sheet can be broken down into its key components: Total Equity, representing the overall shareholders’ equity; Minority Interest (or Non-controlling Interest), which is the portion of equity in subsidiaries owned by outside shareholders; and the term ‘Gross,’ which indicates that the minority interest is included in the total equity figure. Understanding these components is essential for accurately interpreting a company’s financial statements.

Defining Total Equity and Minority Interest

Total equity represents the residual interest in a company’s assets after deducting all liabilities. In a consolidated balance sheet, it encompasses the equity attributable to both the parent company’s shareholders and any minority shareholders of its subsidiaries.

Minority Interest, now formally known as Non-Controlling Interest (NCI), is the portion of a subsidiary’s equity that is not owned by the parent company. It arises when a parent owns more than 50% but less than 100% of a subsidiary. Because the parent consolidates 100% of the subsidiary’s assets and liabilities, the NCI is shown in the equity section to represent the claim of these outside owners on the subsidiary’s net assets.

“You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

Consolidation Example

If Company A owns 80% of Company B, it consolidates 100% of Company B’s financials. The 20% of Company B’s equity that Company A does not own is reported as a non-controlling interest on Company A’s consolidated balance sheet.

The Meaning of “Gross” Minority Interest

When you see the phrase “Total Equity Gross Minority Interest,” the word “gross” means inclusive of minority interest. It signals that the total equity figure has not had the minority-owned portion netted out. This terminology is often used by financial data platforms to clarify that the reported total equity includes the NCI.

Gross vs. Net

Essentially, Total Equity (Gross MI) = Parent’s Equity + Minority Interest. If you were to look at equity ‘net of’ minority interest, you would only be looking at the equity attributable to the parent company’s shareholders.

Reporting Under IFRS and US GAAP

Both IFRS and US GAAP require non-controlling interests to be reported within the equity section of consolidated balance sheets, but presented separately from the parent’s equity.

- IFRS Presentation: IAS 1 requires that the equity attributable to owners of the parent and the equity attributable to non-controlling interests be shown as two distinct line items, which then sum to ‘Total Equity.’

- US GAAP Presentation: Similarly, ASC 810 mandates that NCI be treated as a separate component of equity. This is a change from older practices where it was sometimes shown as a ‘mezzanine’ item between liabilities and equity.

The alignment of IFRS and GAAP on this treatment ensures that the fundamental accounting equation (Assets = Liabilities + Equity) holds true for consolidated entities.

Why This Distinction Matters for Investors and Analysts

Understanding the composition of equity and the NCI component is critical for accurate financial analysis and valuation:

- Return on Equity (ROE) and Per-Share Metrics: To properly calculate ROE and Book Value per Share for the parent’s shareholders, analysts must use equity attributable to the parent (i.e., excluding NCI). Using the gross total equity figure would understate ROE by inflating the equity base.

- Debt-to-Equity and Leverage Ratios: Including NCI makes the equity base appear larger, which can make a company seem less leveraged. Analysts often calculate leverage ratios both ways (with and without NCI) to get a complete risk profile.

- Enterprise Value (EV) and Valuation: In the EV formula (), the NCI is added back. This is because EV is compared against metrics like EBITDA which include 100% of the subsidiary’s results. Adding NCI ensures a consistent, apples-to-apples comparison.

- Transparency and Performance Attribution: Separating NCI allows investors to see what portion of profits and net assets belong to the parent’s shareholders versus outside interests. This prevents overestimating the value accruing to the parent company’s owners.

Q · 01What is Minority Interest?+