A conservative valuation metric representing a company's physical worth after subtracting all liabilities and intangible assets.

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

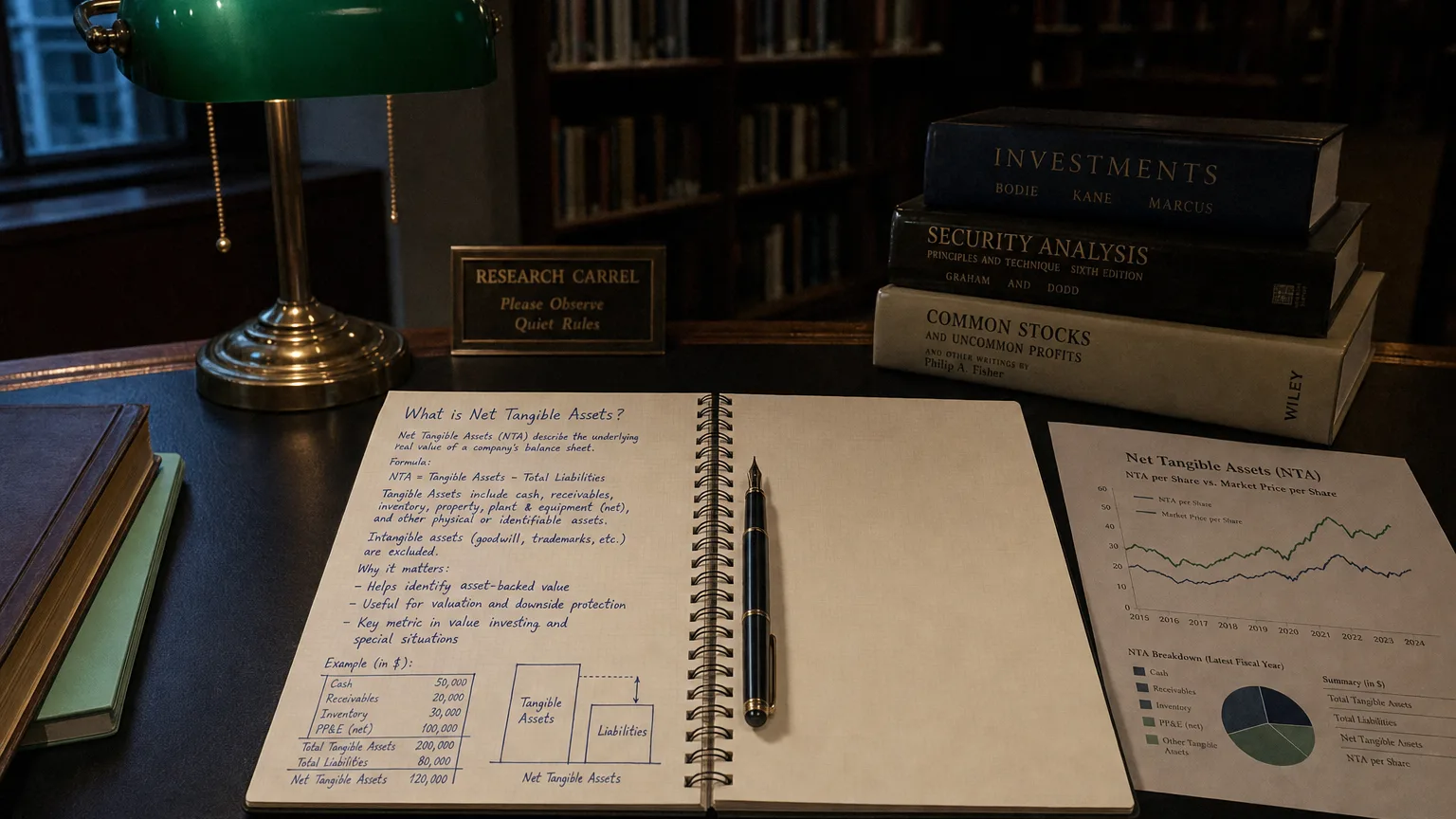

Net Tangible Assets (NTA) represent the value of a company’s physical, tangible assets after deducting all liabilities and excluding any intangible assets. In other words, it is essentially the company’s net book value or net asset value attributable to tangible assets only. This metric is often described as the firm’s “tangible” net worth - the portion of equity backed by real, tangible assets (sometimes called tangible book value or tangible net asset value).

How to Calculate NTA

The calculation of NTA follows directly from its definition. You take everything the company owns (total assets) and subtract two things: (1) the value of intangible assets, and (2) the company’s total liabilities.

Formula:

By removing intangibles and liabilities from total assets, NTA tells us the net value of assets that are tangible and unencumbered by debt.

Tangible vs. Intangible Assets

The distinction between asset types is central to understanding NTA:

- Tangible Assets: These are assets with physical substance that can be seen or touched. Examples include cash, inventory, equipment, vehicles, land, and buildings.

- Intangible Assets: These assets lack physical form but still hold value. Common examples are goodwill, patents, trademarks, copyrights, and brand reputation. They are excluded from NTA because their value is harder to sell or realize in a liquidation.

Importance and Uses of NTA in Analysis

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

NTA is a useful figure in financial analysis and valuation as it provides insight into the solid underlying value of a business:

- Conservative Value Measure: NTA provides a conservative estimate of a company’s worth by reflecting what value would remain if the company had to rely only on its physical assets.

- Creditworthiness & Solvency: Lenders and creditors use NTA to assess financial strength. A higher NTA means more hard assets are available to secure loans and cover obligations.

- Investor Analysis (Valuation): Investors compare a stock’s price to its NTA per share. If the price is significantly below NTA per share, it could indicate the stock is undervalued relative to its physical assets.

- Mergers & Acquisitions: NTA helps acquirers evaluate the baseline tangible worth of a target company, providing an anchor point for valuation by focusing on assets that can be valued more objectively.

Industries Where NTA is Especially Relevant

The relevance of NTA can vary greatly across industries:

Asset-Intensive Industries

NTA is most meaningful in industries where physical assets dominate, such as manufacturing, utilities, oil & gas, and real estate. In these sectors, NTA closely reflects the company’s underlying value because most of the value is tied to tangible things.

Intangible-Heavy Industries

NTA can understate the true worth of businesses in sectors like technology, pharmaceuticals, and media. These companies rely heavily on intangible assets like patents, software, and brand value, which NTA excludes. A low NTA here doesn’t necessarily signal weakness.

Example: Computing NTA from a Balance Sheet

NTA Calculation

Suppose Company X’s balance sheet shows:

- Total Assets = $10 million

- Intangible Assets = $2 million (e.g., goodwill)

- Total Liabilities = $6 million

Using the formula, we subtract the intangibles and liabilities from total assets:

Formula:

This result indicates that Company X’s net tangible assets amount to **2 million of value would remain for shareholders. This calculation provides a cautious view of the company’s worth by focusing only on what can be realized from its physical resources.