is a financial concept covered in this article. Non-Recurring or Unusual Gains and Losses from Core Operations

If we avoid the losers, the winners will take care of themselves.

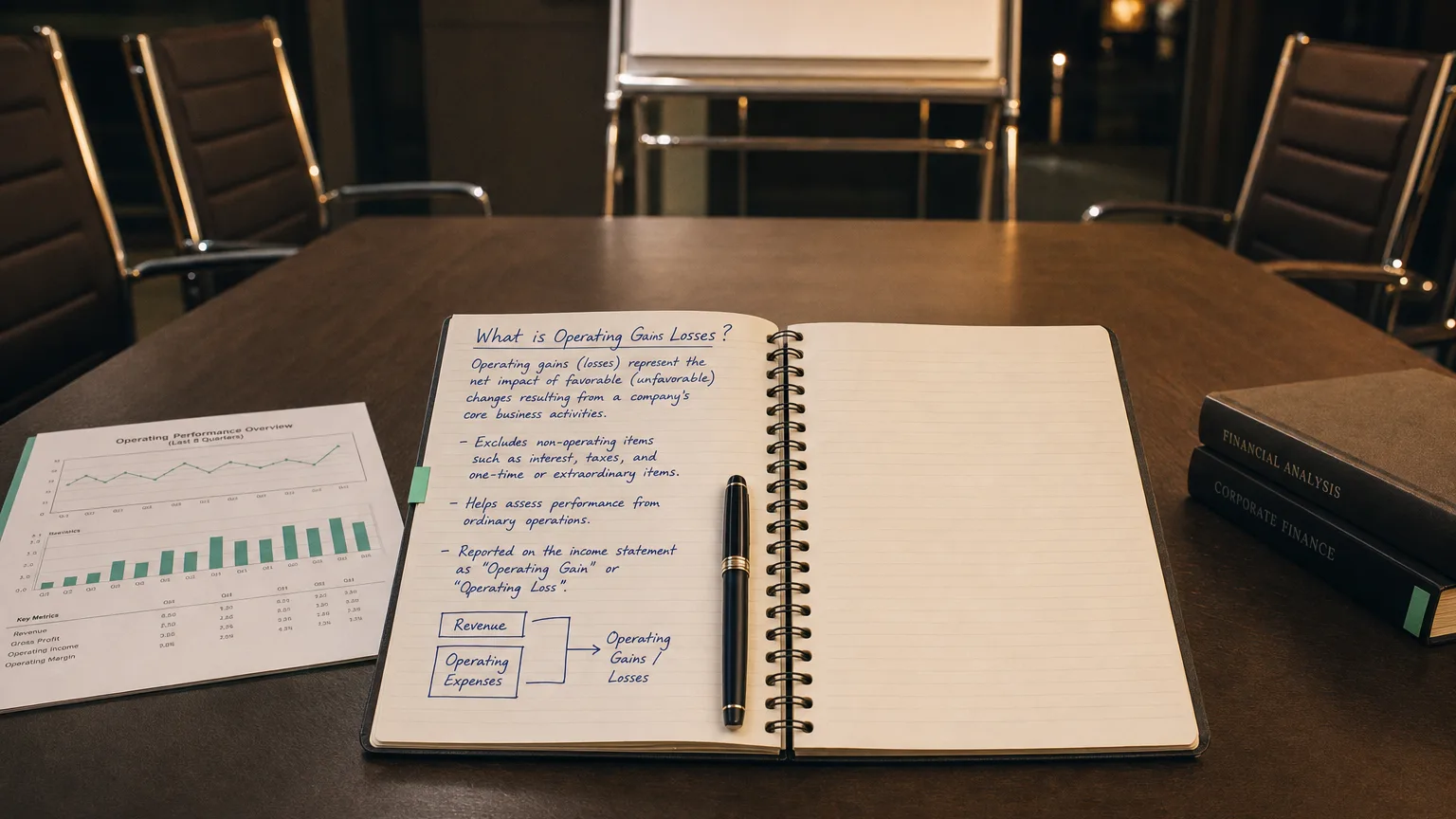

Operating Gains Losses are non-recurring or unusual gains and losses arising from a company’s core business activities that are not part of normal, day-to-day operations. These items are included in operating income but are often highlighted separately because they can distort the view of ongoing profitability. They reflect events like asset disposals, restructuring charges, or litigation settlements tied to operations.

What Counts as Operating Gains/Losses

These are gains or losses from events related to core operations but not expected to recur regularly.

- Gain/loss on sale of operating assets (machinery, vehicles)

- Restructuring charges (severance, facility closure)

- Inventory write-downs or spoilage

- Litigation settlements from business disputes

- Insurance recoveries for operating losses

- Curtailment/settlement gains on pensions (operational impact)

They stay in operating income because they’re tied to the business’s primary activities.

Extraordinary items (unusual AND infrequent) are now prohibited—most go here or non-operating.

“If we avoid the losers, the winners will take care of themselves.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

A Real Example

Manufacturer closes an old factory.

- Sells factory building for 10M) → $5M gain

- Pays 8M loss

- Net Operating Loss: -$3M

- Reported in operating income as ‘Restructuring and asset disposal (net)’

Core ongoing profit looks weaker this year due to one-time cleanup.

Why They’re Separated

- Highlight non-recurring nature

- Help analysts adjust for ‘core’ earnings

- Show impact of strategic decisions (restructuring)

- Transparency on unusual operational events

Presentation

In income statement:

- Separate line(s) in operating expenses/income

- ‘Restructuring charges’, ‘Asset disposal gains/losses’

- Or grouped as ‘Other operating gains/losses’

Cash flow: Non-cash portions added back; cash portions in operating.

Common Scenarios

- Factory or store closures

- Product line discontinuation

- Sale of excess equipment

- Legal settlements from business contracts

- Environmental remediation for operating sites

What to Watch For

- Frequency (recurring ‘one-time’ charges?)

- Size vs. operating profit (distorting core?)

- Trend (restructuring phase?)

- Cash vs. non-cash components

- Management guidance on ‘adjusted’ earnings excluding these

Chronic operating losses may indicate ongoing issues masked as ‘unusual’.