A guide to understanding the money owed to a company by its customers and other parties, and how this asset impacts liquidity and financial health.

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

Receivables are monetary claims that a company has against other parties – essentially, money owed to the company. These arise typically when a business sells goods or services on credit (creating an accounts receivable) or when it lends out money via formal agreements (creating a note receivable). Receivables are recorded as assets on the balance sheet because they represent future economic benefits – the company expects to receive cash from its customers or debtors in the future. In other words, once the company has delivered a product or service but not yet been paid, it recognizes a receivable for the amount due.

Types of Receivables

Companies may have several types of receivables, including both trade and non-trade receivables. Common categories include:

-

Accounts Receivable (Trade Receivables): These are amounts owed by customers for goods or services sold on credit. Accounts receivable are essentially claims to cash for sales that have been made but not yet paid for. They are typically short-term (due within a few weeks or months) and are usually reported net of any allowance for doubtful accounts (more on this below). In other words, the balance sheet will often show “Accounts receivable, net,” which is the gross receivables minus an estimate of uncollectible amounts.

-

Notes Receivable: These are amounts owed to the company under more formalized credit arrangements, evidenced by a written promissory note. Notes receivable often carry an interest component and a fixed term. They can be short-term or long-term assets depending on the note’s maturity date. If a note receivable is due within one year, it is classified as a current asset; if the payment is due more than one year out, it is classified as a non-current (long-term) asset. Notes receivable give the holder the legal right to receive the specified amount (plus interest, if applicable) at the agreed future date.

-

Other Receivables: This category encompasses any other amounts owed to the company outside of normal customer sales. Examples include interest receivable (interest earned but not yet received), advances or loans to employees, tax refunds due, or any miscellaneous receivables. These are sometimes called non-trade receivables. Like accounts receivable, they would be classified as current or non-current assets based on when the cash is expected to be received. For instance, if an employee owes the company $1,000 to be repaid over the next four months, that amount would appear under current “other receivables.” A pending income tax refund due in the near term would likewise be recorded as a current other receivable.

Balance Sheet Classification

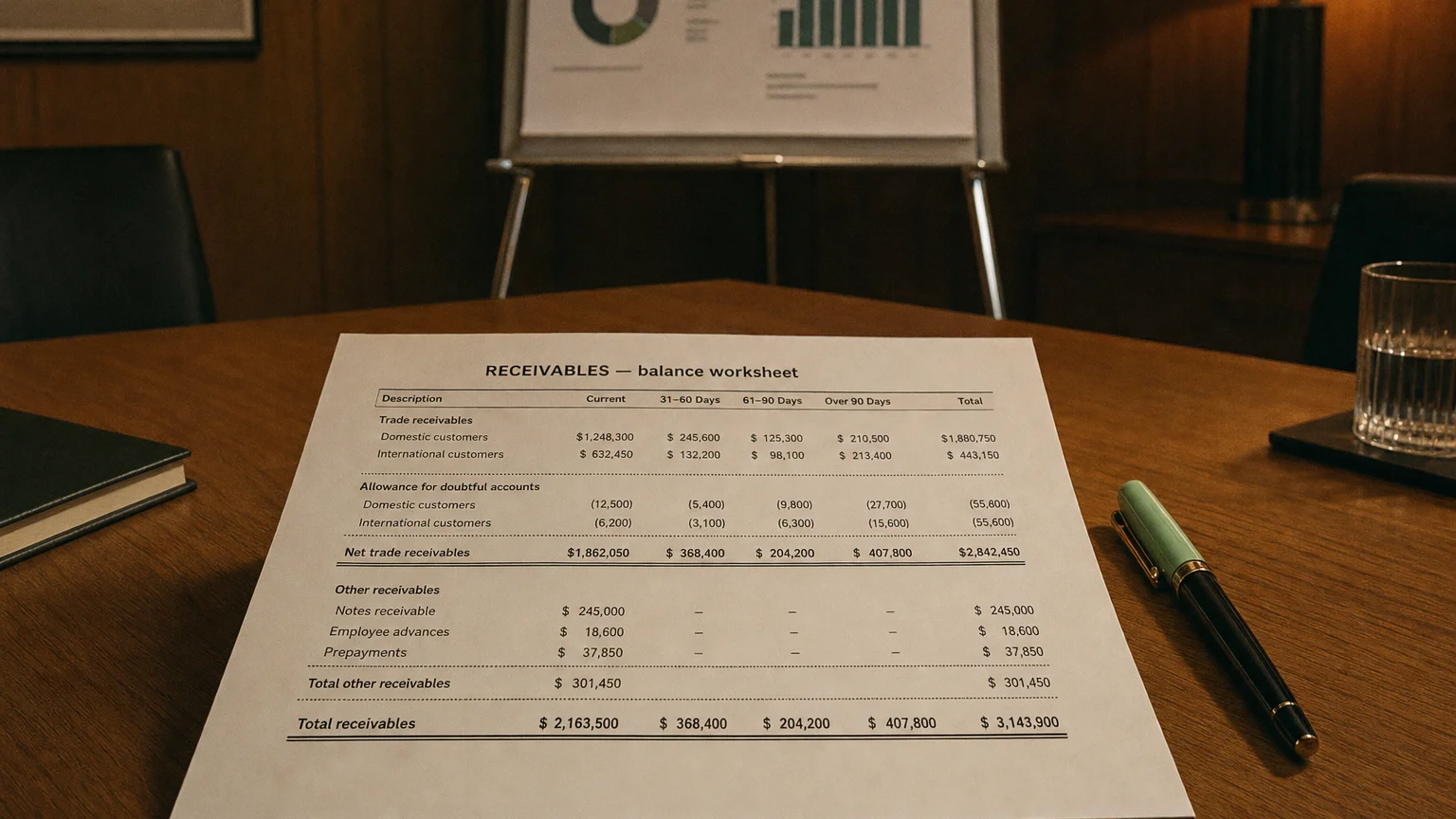

Current assets section of a sample balance sheet (illustrative). Notice that Accounts receivable – net is listed among current assets, after cash and short-term investments, and Other receivables are also shown.

Receivables generally appear in the current assets section of the balance sheet, reflecting their short-term nature. Accounts receivable and other short-term receivables are listed as current assets because they are expected to be converted to cash within the next 12 months (the definition of a current asset). As the example above shows, accounts receivable is often labeled “accounts receivable – net,” indicating that an allowance for uncollectible accounts has been deducted to report the net realizable value. Typically, accounts receivable will be one of the larger current asset line items and is listed just after cash and cash equivalents (and short-term investments) and before inventory on the balance sheet.

If a portion of receivables is not expected to be collected within one year, those longer-term receivables would be classified under non-current assets (often in a category like “Other assets” or a specifically labeled “Long-term receivables” line). For example, a multi-year note receivable or any installment payments due beyond a year would be reported as a long-term asset. In practice, companies may separate the current and non-current portions of notes receivable on the balance sheet to give a clear view of what is due in the short term versus later.

Significance to Liquidity and Working Capital

Receivables are a key component of a company’s liquidity and working capital position. Working capital is the excess of current assets over current liabilities, and accounts receivable often constitute a significant portion of current assets. Because receivables will eventually turn into cash (when customers pay their bills), they contribute to the company’s ability to meet short-term obligations. In essence, a healthy accounts receivable balance (relative to sales) can indicate robust revenue streams and upcoming cash inflows, bolstering the company’s short-term financial health.

However, it’s important to note that receivables are not the same as cash until they are collected. A company that has most of its current assets tied up in accounts receivable could face liquidity issues if those customers delay payment. In other words, even if working capital is positive, slow collection of receivables can lead to cash flow problems. This is why the quality of receivables (how quickly and reliably they turn into cash) is closely monitored. Analysts often look at metrics like the accounts receivable turnover ratio, which measures how many times during a period the company collects its average receivables, or the average collection period (days sales outstanding). A high turnover or low days outstanding indicates the company is efficiently converting credit sales into cash, which enhances liquidity. Conversely, a slowdown in collections can signal credit issues or an impending cash crunch, even if sales are strong on paper.

In summary, receivables contribute to liquidity but must be managed well. They are an integral part of working capital management: companies may use strategies like offering discounts for early payment or more stringent credit policies to ensure receivables are collected timely, thus maintaining healthy cash flow.

Common Risks and Considerations

While receivables represent future cash, they also carry certain risks and require careful management. Key considerations include:

-

Credit Risk and Bad Debts: Not all customers will pay their bills. Some receivables can become uncollectible due to customer default (e.g., bankruptcy or other financial troubles). This risk of bad debt means that a portion of accounts receivable might never turn into cash. To account for this, companies estimate and record an Allowance for Doubtful Accounts (a contra-asset) to reduce receivables by the amount of receivables expected to be uncollectible. This results in the “net” receivables figure mentioned earlier. For example, if a company has $100,000 of gross receivables and expects $5,000 may not be collected, it will report “Accounts receivable, net $95,000,” with $5,000 in the allowance account. (In Microsoft’s financial statements, for instance, the allowance for doubtful accounts is described as management’s “best estimate of probable losses inherent in the accounts receivable balance” – essentially the anticipated bad debts.) When a specific account is deemed uncollectible after all efforts, it is written off by removing it from accounts receivable and charging it against the allowance, recognizing a bad debt expense at that point.

-

Collection and Cash Flow Timing: Even if receivables are eventually collected, slow-paying customers can strain a company’s cash flow. Selling on credit increases revenue, but until the cash is received, the company cannot use those funds to pay its own bills. A growing accounts receivable balance that isn’t turning into cash in a timely manner can lead to liquidity problems – the company may appear profitable yet struggle to pay salaries, suppliers, or lenders due to lack of cash. Effective credit management (credit checks, setting credit limits, and following up on overdue accounts) is important to mitigate this risk. Companies sometimes resort to strategies like factoring (selling receivables to a finance company for immediate cash) or using receivables as collateral for loans if they need to accelerate cash inflows, though such actions come with costs.

In managing receivables, businesses must balance sales growth (which often means offering credit to customers) with the risk of not collecting payment. Concentration risk is another consideration: if a large portion of receivables is tied to one or a few customers, the financial health of those customers is crucial to the company’s own financial stability. Diversifying the customer base and monitoring creditworthiness helps manage this risk.

Another important consideration is the accounting for receivables: companies follow the principle of conservatism by not overstating receivables. The use of the allowance for doubtful accounts, as mentioned, ensures that the net receivables reflect a more realistic amount the company expects to collect. This way, investors and creditors see a balance sheet figure that is already reduced for potential losses. Periodically, management reviews receivables and adjusts the allowance as needed (increasing it if expected bad debts rise, which in turn increases bad debt expense on the income statement).

Measurement and Reporting (GAAP vs. IFRS)

Under both U.S. GAAP and IFRS, receivables are measured and reported in a way that reflects their collectible value. In practice, this means receivables are shown at their net realizable value – the amount of cash the company expects to ultimately collect. For example, under U.S. GAAP a company reports “Accounts Receivable, net” on the balance sheet, which equals the total receivables minus the allowance for doubtful accounts (the estimated uncollectible portion). This net figure is considered the best estimate of collectible amount, and it aligns with the accounting principle that assets should not be overstated. According to GAAP, an accounts receivable balance should be presented net of anticipated losses from bad debts, so that the balance sheet reflects a realistic value of that asset. Any adjustments to this estimate (i.e. changes in the allowance) flow through the income statement as bad debt expense.

IFRS has a very similar requirement, though the terminology and methodology differ slightly. IFRS uses an expected credit loss (ECL) model for financial assets like trade receivables. Under IFRS 9, companies must recognize an impairment allowance for receivables from the moment they are originated, based on the probability of default and expected loss even if the risk of default is low. In simpler terms, IFRS requires companies to continually estimate how much of their receivables won’t be collected, factoring in not just past collection history but also forward-looking information (such as economic conditions or customer credit changes). This allowance for expected credit losses serves the same purpose as the allowance for doubtful accounts in GAAP – reducing the carrying value of receivables to the amount likely to be received. The IFRS approach is more explicitly forward-looking, but the end result (net receivables on the balance sheet) is conceptually the same as GAAP’s net realizable value.

Despite some differences in estimation techniques, both GAAP and IFRS aim to ensure that receivables are reported at a realistic recoverable amount. Both frameworks require that if collection of a receivable becomes doubtful, an impairment loss is recognized. The allowance (or provision) for credit losses is updated over time as expectations change. By reporting receivables net of expected uncollectible amounts, the financial statements give a clearer picture of the company’s true assets. In sum, receivables on the balance sheet – whether under GAAP or IFRS – are not simply the sum of all invoices owed, but rather that sum minus a reasonable estimate of what won’t be collected, so that the asset is shown at its fair net value to the business.

Sources:

-

Investopedia – Definition and explanation of Accounts Receivable (AR)

-

Corporate Finance Institute – Definition of Notes Receivable and balance sheet classification

-

Investopedia – Working Capital components (accounts receivable, notes receivable) and liquidity considerations

-

AccountingCoach – Balance sheet presentation of accounts receivable (net of allowance) and other receivables

-

KPMG (IFRS) – IFRS 9 expected credit loss model for trade receivables

-

CareerPrinciples (Accounting & Finance) – Discussion of accounts receivable as current assets and risks (bad debts, cash flow)

-

2012 Accounting Textbook (Lardbucket) – GAAP requirement to report accounts receivable at net realizable value (amount expected to be collected)

-

Pearson (Financial Accounting Channel) – Summary of GAAP vs. IFRS treatment of receivables and allowances

Q · 01What is Receivables?+