Treasury Shares Number Definition & Examples

An overview of shares repurchased by a company, their strategic uses, and their significant impact on key financial statements and metrics.

Overview

An overview of shares repurchased by a company, their strategic uses, and their significant impact on key financial statements and metrics.

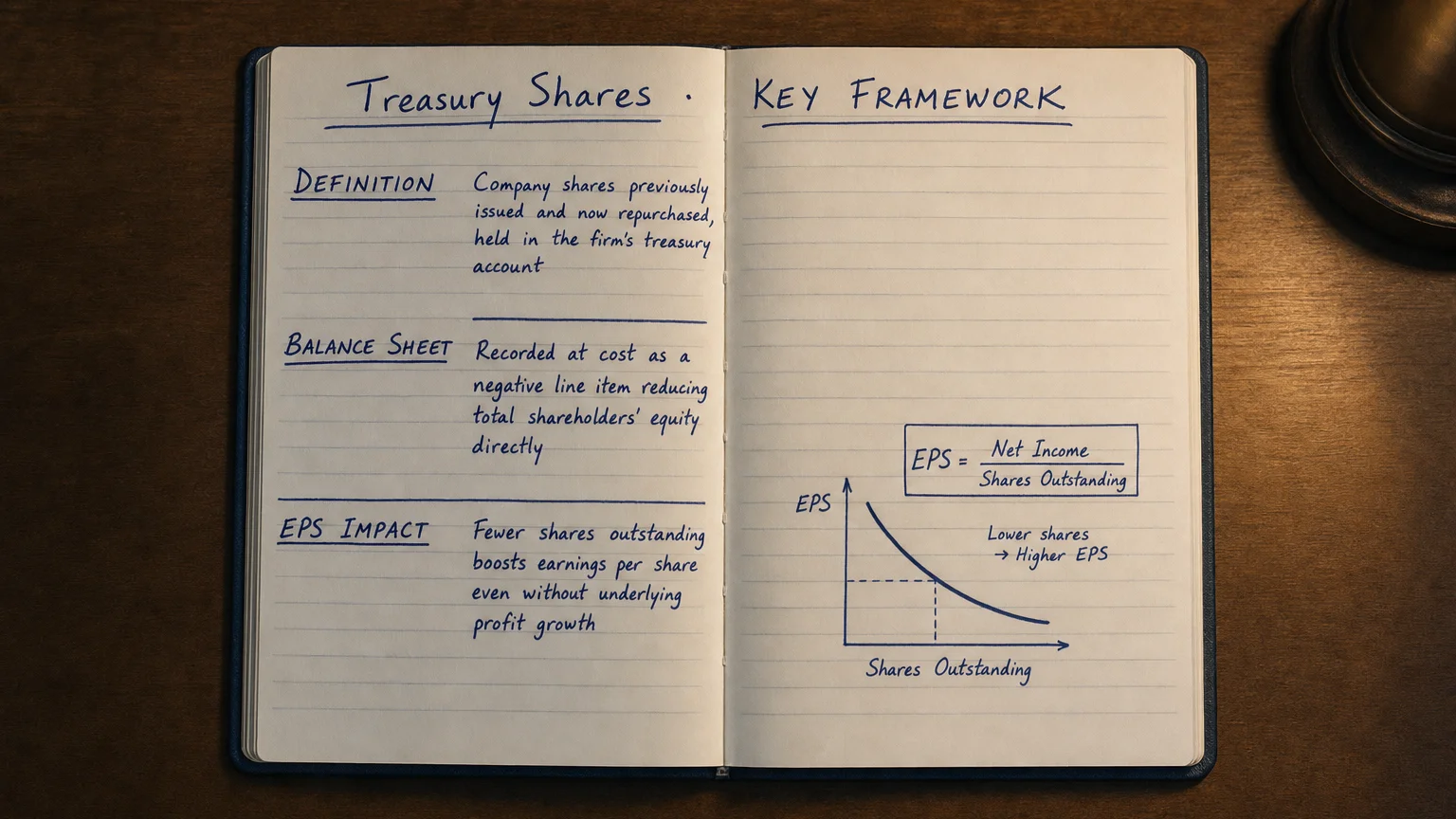

Treasury shares (also known as treasury stock) are shares of a company’s own stock that it previously issued and later repurchased from shareholders. Once reacquired, these shares are held by the company itself (in the corporate “treasury”) and are no longer considered outstanding shares in the market. In practical terms, treasury shares have no voting rights, do not receive dividends, and are excluded from earnings-per-share calculations. They represent stock that the company owns internally after a buyback, rather than being held by outside investors.

The "Treasury Shares Number" on the Balance Sheet

The “Treasury Shares Number” on a balance sheet refers to the number of shares that the company currently holds as treasury stock (i.e., the count of shares repurchased and not reissued). In fact, the number of treasury shares is essentially the difference between the total number of shares issued and the number of shares currently outstanding in the market. This treasury shares number is often disclosed in the equity section of the balance sheet or in the notes, indicating how many shares the company has in its treasury that could be reissued or retired in the future.

Calculating Treasury Shares

If a company has issued 1,000,000 shares in total and 900,000 are outstanding (held by external shareholders), the remaining 100,000 shares are treasury shares held by the company.

Why Do Companies Hold Treasury Shares?

Companies may choose to buy back their own stock and hold it as treasury shares for several strategic reasons:

- Boost Shareholder Value: Repurchasing shares reduces the number of shares in circulation, which can make each remaining share more valuable. By decreasing supply, a buyback often increases the share price and the ownership percentage of remaining shareholders. In other words, each shareholder ends up owning a slightly larger slice of the company than before.

- Improve Financial Metrics (EPS and ROE): With fewer outstanding shares after a buyback, key performance metrics can improve. A notable example is earnings per share (EPS) - since EPS is calculated as net income divided by outstanding shares, reducing the share count boosts EPS (even if total earnings remain the same). Similarly, share repurchases reduce total equity, which can increase return on equity (ROE) because the same earnings are measured against a smaller equity base. This can make the company appear more profitable and efficient in the eyes of investors.

- Signal Confidence / Undervaluation: When management buys back stock, it often signals to the market that they believe the company’s shares are undervalued. A buyback demonstrates confidence in the company’s future prospects, suggesting that the best investment the company can make is in itself. This vote of confidence can attract investors and potentially lift the stock price.

- Defend Against Takeovers: Holding treasury shares can be a defensive tactic. By reducing the number of shares available on the open market, a company makes it harder for a hostile bidder to acquire a controlling stake. In a potential takeover scenario, fewer publicly available shares mean an outsider would have more difficulty accumulating enough shares to challenge existing ownership control.

- Provide Stock for Future Use: Treasury shares give the company flexibility for future corporate actions. The company can reissue these shares later for various purposes - for example, to fund acquisitions, raise capital, or fulfill employee stock option and compensation plans without issuing brand-new shares. This reserve of shares can be useful to avoid diluting existing shareholders when new shares are needed for strategic transactions. Alternatively, the company may choose to permanently retire some or all of the treasury shares, reducing the total share count indefinitely.

"Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray."

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman's Letter 2014 (2014)

Impact of Treasury Shares on Earnings Per Share (EPS)

Earnings per share (EPS) is directly affected by treasury shares because of how EPS is calculated. When a company holds treasury shares, those shares are not part of the outstanding share count used in the EPS calculation. By repurchasing shares and increasing the treasury stock, the company lowers the denominator (outstanding shares) in the EPS formula, which increases EPS assuming net income stays the same.

Formula:

EPS Calculation Example

If a company earned $10 million and had 10 million shares outstanding, its EPS would be $1.00. If the company buys back 2 million shares (moving them to treasury), then only 8 million shares remain outstanding. If earnings are still 1.25** ($10 million / 8 million shares). This boost in EPS occurs without any change in total earnings, purely due to fewer shares in the hands of the public.

Investor Awareness

Investors should be aware that an EPS boost from share buybacks doesn’t reflect improved business performance, but rather a change in capital structure. Since treasury shares are not outstanding, they are completely excluded from EPS calculations.

Impact of Treasury Shares on Shareholders’ Equity

Treasury stock also has a significant impact on the shareholders’ equity section of the balance sheet. When a company buys back its own shares, it uses cash (an asset) to repurchase stock, and in exchange it records the repurchased shares as treasury stock in the equity section. Treasury stock is recorded as a contra-equity account - essentially a negative equity balance. This means it reduces total shareholders’ equity.

On the balance sheet, you will typically see treasury stock listed under shareholders’ equity as a negative number (a deduction), often labeled “Treasury Stock (at cost)” or “Treasury Shares.” For instance, if a company spent 5 million and simultaneously its equity is reduced by $5 million. Treasury shares do not count as an asset; instead, repurchasing shares is essentially returning capital to shareholders, so it reduces the company’s net equity value.

Real-World Example: Apple Inc.

Apple Inc., which has executed massive share buyback programs, saw its total shareholders’ equity shrink from about $134 billion in 2017 to roughly $50.7 billion by 2022. This dramatic drop was largely because Apple returned so much capital to shareholders via stock repurchases (treasury stock) and dividends that it exceeded its net income, directly eroding the equity base.

Gains and Losses on Treasury Stock

It’s important to note that treasury share transactions do not contribute to retained earnings or profit. Any gains or losses from reissuing treasury shares are typically recorded in other equity accounts (like additional paid-in capital), not as earnings on the income statement.

Where Are Treasury Shares Reported on the Balance Sheet?

Treasury shares are reported in the shareholders’ equity section of the balance sheet, not among assets or liabilities. They usually appear as a separate line item called “Treasury Stock” or “Treasury Shares”, with a negative value to indicate that it reduces total equity. Often, the entry will specify the number of treasury shares and the total cost paid for them. For example, a balance sheet might list: Treasury stock - 100,000 shares (at cost $2,000,000). This tells readers that the company holds 100,000 of its own shares and spent $2 million to acquire them.

In summary, treasury shares on the balance sheet indicate shares that the company has issued in the past but later bought back and now holds internally. Understanding the role of treasury shares helps investors and students of finance interpret a company’s financial statements more accurately, shedding light on how share buybacks affect a company’s financial health and shareholder value.