Gains & Losses Not Affecting Retained Earnings is a financial concept covered in this article.

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

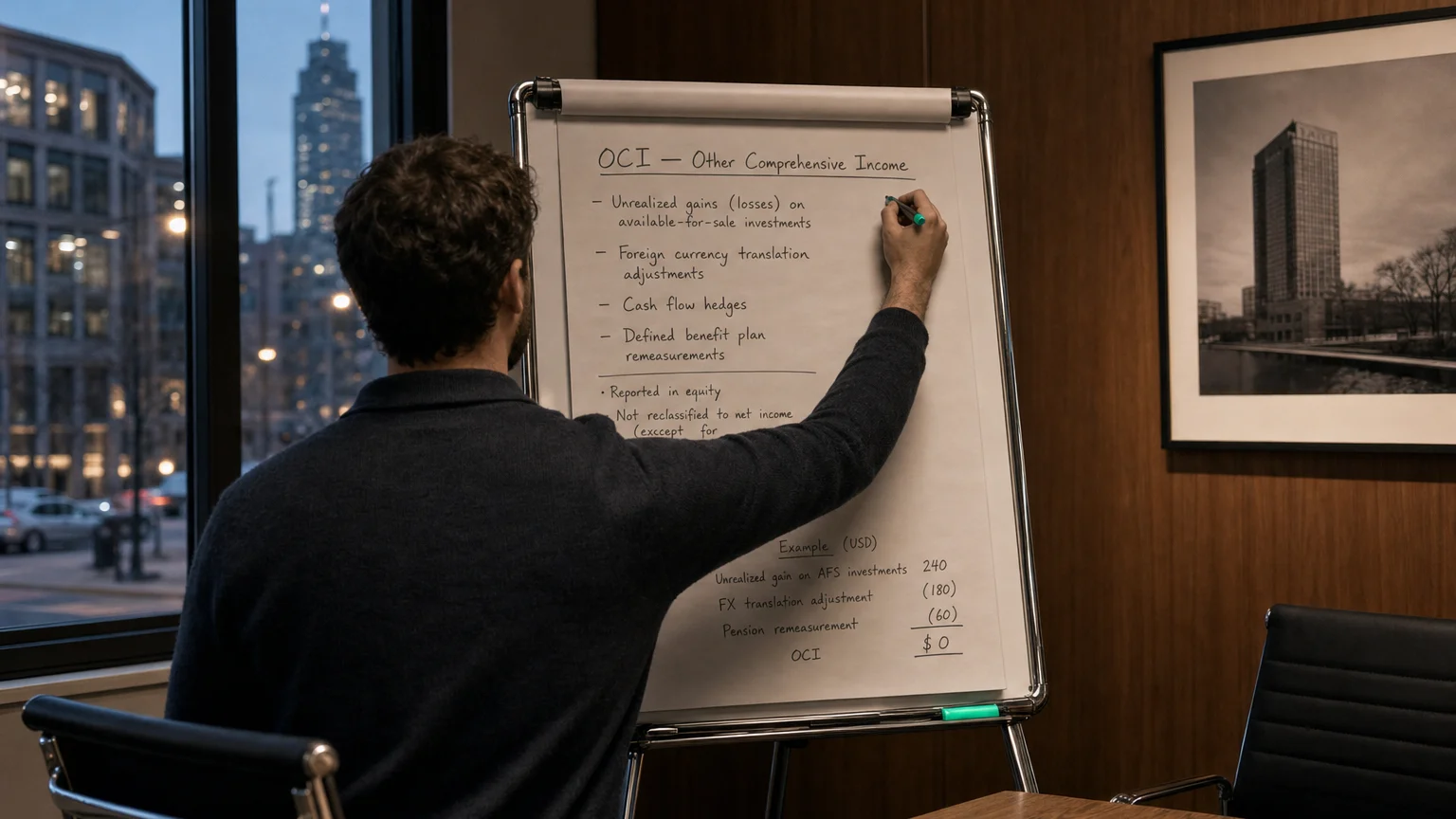

In financial reporting, gains and losses not affecting retained earnings refer to certain income items that are recorded outside of net income, directly in equity. These typically appear as part of Other Comprehensive Income (OCI) and accumulate on the balance sheet in Accumulated Other Comprehensive Income (AOCI), separate from retained earnings. They represent special, often unrealized or non-operational items, that are excluded from the traditional profit-and-loss computation.

Why These Gains & Losses Don’t Affect Retained Earnings

Retained earnings represents the accumulated net income of a company over time, minus dividends. Because the gains and losses in question are, by definition, excluded from net income, they do not impact the retained earnings account. They are recorded directly in equity through OCI, so they increase or decrease shareholders’ equity without passing through the income statement’s ‘bottom line’.

Comprehensive Income vs. Net Income

Comprehensive income is a broader measure than net income. The relationship is: Since retained earnings only accumulates net income, the OCI portion is kept separate.

Reporting in OCI and AOCI

These gains and losses are reported in Other Comprehensive Income (OCI), which is presented separately from net income. Companies either show OCI as a section below net income (creating a single ‘Statement of Comprehensive Income’) or in a second, consecutive statement.

The OCI items from each period are then accumulated on the balance sheet in a dedicated equity account called Accumulated Other Comprehensive Income (AOCI). AOCI appears as a separate line item within the shareholders’ equity section, distinct from retained earnings and contributed capital. This transparent reporting allows stakeholders to see the impact of these items without conflating them with regular, realized earnings.

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (1934)

Examples of Gains & Losses in OCI

Common examples of items that are routed through OCI and thus bypass retained earnings include:

- Unrealized Gains/Losses on Certain Investments: Under U.S. GAAP, changes in the fair value of ‘available-for-sale’ debt securities are recorded in OCI. The gain or loss is only moved to net income when the security is sold.

- Foreign Currency Translation Adjustments: When a company consolidates foreign subsidiaries, gains or losses from translating their financial statements into the parent’s currency are reported in OCI.

- Cash Flow Hedge Gains/Losses: The effective portion of unrealized gains or losses on derivatives designated as cash flow hedges is recorded in OCI until the hedged transaction affects earnings.

- Pension Plan Adjustments: Certain remeasurements for defined benefit pension plans, such as actuarial gains and losses, are recorded in OCI to smooth their impact on earnings.

- Revaluation Surplus (IFRS Only): Under IFRS, companies can revalue property, plant, and equipment to fair value. The resulting upward gain is recorded in OCI, not net income.

Accounting Principles and Standards (GAAP vs. IFRS)

Both U.S. Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) require the separate treatment of OCI items. Accounting standards explicitly mandate that certain gains and losses be excluded from net income and reported in OCI.

Under U.S. GAAP, ASC 220 governs comprehensive income reporting. Under IFRS, IAS 1 stipulates the presentation of OCI. While there are minor differences in which specific items are directed to OCI under each framework, the core concept is identical: some gains and losses are intentionally kept out of the income statement to provide a clearer picture of a company’s core operational performance.