Pearson's Correlation Coefficient is a financial concept covered in this article.

The goal of a successful trader is to make the best trades. Money is secondary.

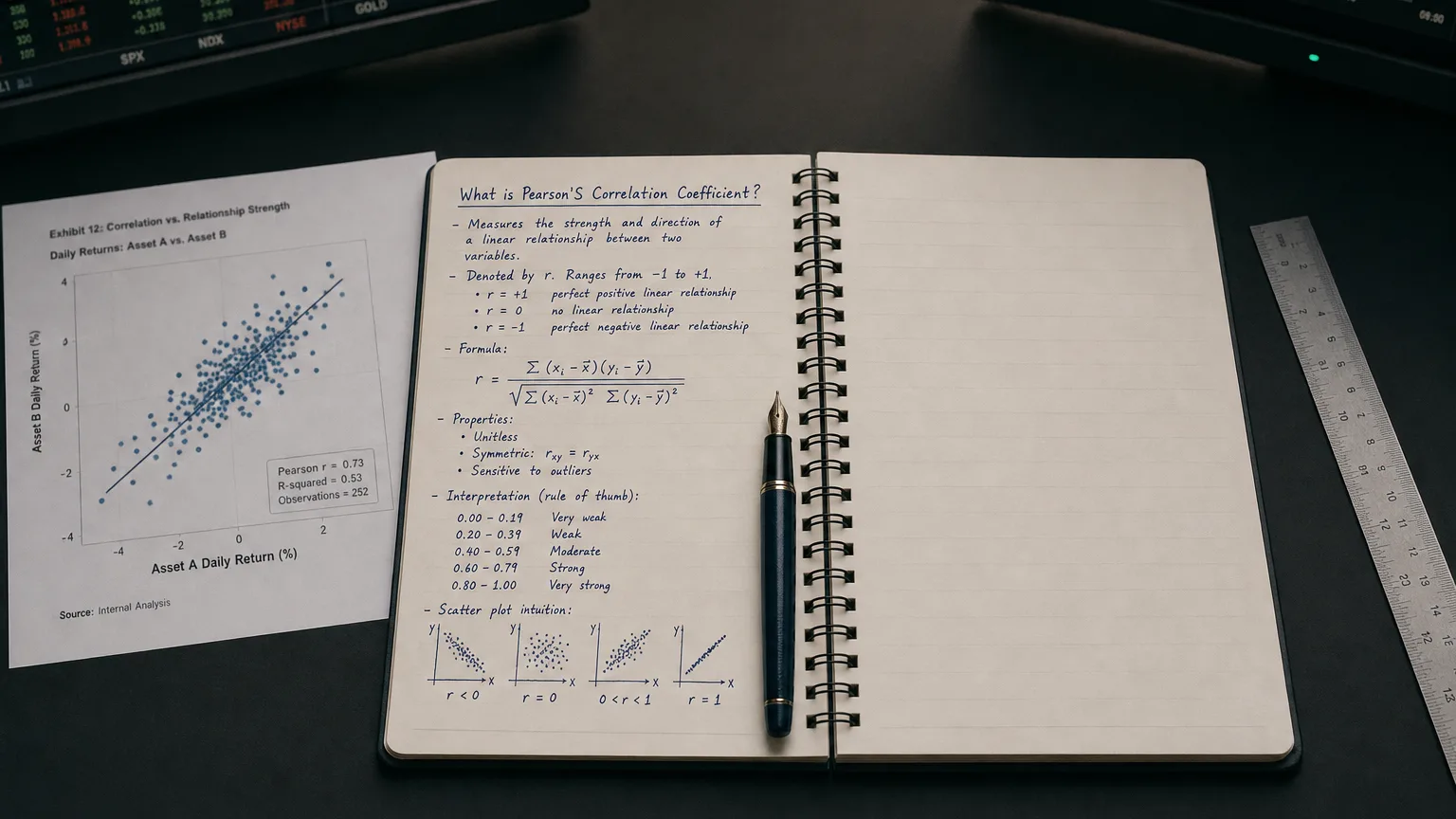

Developed by Sir Karl Pearson (1896), r is the classic gauge of linear association between two quantitative variables. It answers one burning question: “When X moves, does Y groove in the same direction, the opposite, or not at all—and by how much?”

-

Range: –1 to +1

-

+1 = perfect positive line

-

0 = no linear link

-

–1 = perfect negative line

-

The Formula (Population & Sample)

(Formula — visualization pending)

-

Numerator: covariance (co-movement “rhythm”)

-

Denominator: product of the two standard deviations (scales the jam between –1 and +1)

Core Assumptions

| # | Assumption | Why It Matters |

|---|---|---|

| 1 | Linearity | r only measures straight-line love; curved relationships slip through the cracks. |

| 2 | Homoskedasticity | Constant spread keeps variance stable; funnel-shaped scatter weakens reliability. |

| 3 | Interval/ratio scales | Rank or categorical data need different grooves (Spearman, Kendall). |

| 4 | No huge outliers | One rogue soloist can hijack the whole score. |

Interpreting the Decibels

| Weak | Moderate | Strong | |

|---|---|---|---|

| Positive | 0 < r ≤ 0.3 | 0.3 < r ≤ 0.7 | 0.7 < r ≤ 1 |

| Negative | –0.3 ≥ r > 0 | –0.7 ≥ r > –0.3 | –1 ≥ r > –0.7 |

Rule of thumb—always eyeball a scatter plot; numbers alone can’t reveal nonlinear riffs.

Significance Test (Is r Just Noise?)

(Formula — visualization pending)

Compare to the critical t for your α-level (e.g., 0.05). If |t| exceeds the cutoff, the correlation’s louder than random chatter.

Strengths & Limitations

Strengths

-

Simple, dimensionless, and widely understood.

-

Fast to compute—even streaming in real time.

-

Input to many advanced models (CAPM betas, factor analysis, Kalman filters).

Cautions

-

Correlation ≠ Causation—no matter how tight the groove.

-

Sensitive to outliers—trim or winsorize when necessary.

-

Blind to nonlinear jams—consider rank or distance measures if curvature lurks.

-

Spurious links from non-stationary data; always test for common trends or cointegration in time series.

Finance-Flavored Use-Cases

-

Portfolio Diversification – Pair assets with low or negative r to damp overall volatility.

-

Pairs Trading – Spot highly positive correlations, then exploit temporary spread deviations.

-

Factor Exposure Diagnostics – Correlate returns with macro factors (rates, oil, VIX).

-

Risk Parity Weighting – Use dynamic correlation matrices in covariance estimation.

-

Event Studies – Check how stock returns co-move with benchmark pre/post news.

Quick Example

Imagine daily returns for Stock A and Stock B over 60 trading days:

-

Covariance = 0.0008

-

σₐ = 0.02

-

σᵦ = 0.018

(Formula — visualization pending)

Interpretation: moderate positive correlation—they often groove together, but plenty of solo sections remain.

Encore Takeaways

-

Pearson’s r is the straight-line vibe check—always start (but seldom finish) your analysis here.

-

Plot before you quote: scatterplots reveal hidden solos.

-

Guard against outliers, spurious links, and nonlinearity—use robust or rank-based alternatives when needed.

-

In markets, dynamic correlations can change key signatures—update your matrix often.

Now you’ve got Pearson’s Correlation dialed up to 11. Drop it into your analytical set list and keep those insights rock-solid.