Variance is a financial concept covered in this article. The Core Statistical Measure of Price Dispersion and Volatility

Technical analysis tracks the past; it does not predict the future. You have to use your own intelligence to draw conclusions.

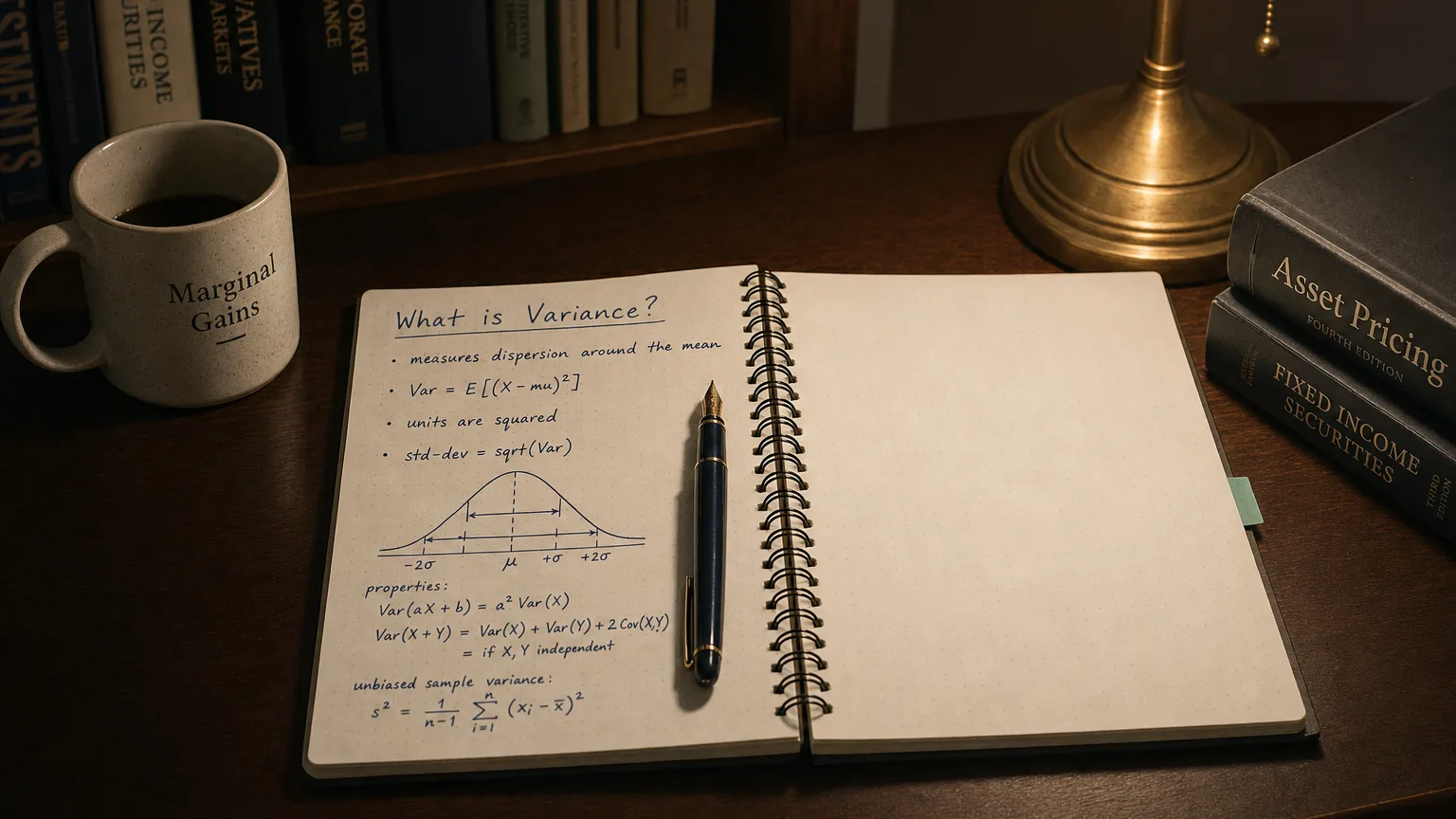

Variance is the granddaddy of volatility stats – it quantifies how spread out prices are around their average by averaging the squared deviations. In trading, it’s the raw engine behind Standard Deviation (σ = √variance), powering Bollinger Bands, risk models, and dispersion analysis. High variance means wild price swings; low variance signals calm clustering. It’s the pure, unrooted measure of ‘how much prices are deviating’ – essential for understanding market chaos, building adaptive systems, and sizing risk properly.

The Core Formula – Squared Deviations

Population variance (most trading platforms):

\text{Variance} = \frac{1}{N} \sum_{i=1}^{N} (P_i - \bar{P})^2

- P_i: Price (usually close) each period

- \bar{P}: Mean price over N periods

- N: Look-back window

Sample variance uses N−1 – minor difference for large N.

“Technical analysis tracks the past; it does not predict the future. You have to use your own intelligence to draw conclusions.”

— Bruce Kovner, Hedge Fund Manager & Founder, Caxton Associates Market Wizards (1989)

Interpreting Variance Levels

Volatility signals:

- Low variance: Prices hugging the mean – low volatility, potential squeeze.

- Rising variance: Dispersion increasing – volatility expansion, trend possible.

- High variance: Wide swings – over-extension or strong momentum.

- Falling variance: Calming down – consolidation brewing.

Since it’s squared, units are price² – take square root for intuitive σ.

Practical Trading Applications

Where variance shines:

- Bollinger Bands: Width = k × √variance – dynamic volatility envelope.

- Risk models: Portfolio variance for diversification and exposure.

- Adaptive systems: Scale stops/position size with current variance.

- Regime detection: Rising variance from lows → breakout potential.

Parameter Choices

N controls responsiveness:

- Short (10–14): Fast volatility changes – intraday focus.

- Classic (20): Standard for Bollinger and daily analysis.

- Long (50+): Smooth macro dispersion view.

Variance vs Standard Deviation vs ATR

Quick distinctions:

- Variance: Squared dispersion – raw input for models.

- Std Dev (σ): √variance – same units as price, intuitive.

- ATR: Range-based volatility – includes gaps, directionless.

Use variance when feeding models; σ for visualization.

Strengths and Limitations

The Wins

- Pure statistical dispersion – foundation of modern volatility tools.

- Essential for Bollinger, risk parity, and adaptive strategies.

- Clean input for quantitative models.

- Works across any price series.

The Gotchas

- Squared units (price²) – less intuitive than σ.

- Assumes normality – markets have fat tails/outliers.

- Lagging and gap-blind (unlike ATR).

- Sensitive to period choice.

Your Variance Quick-Start

- Plot variance with N=20 on closes.

- Compare to historical levels for context.

- Use as input for Bollinger width or risk scaling.

- Watch rising/falling variance for regime clues.

- Take square root for price-unit volatility (σ).

- Combine with ATR for complete picture.