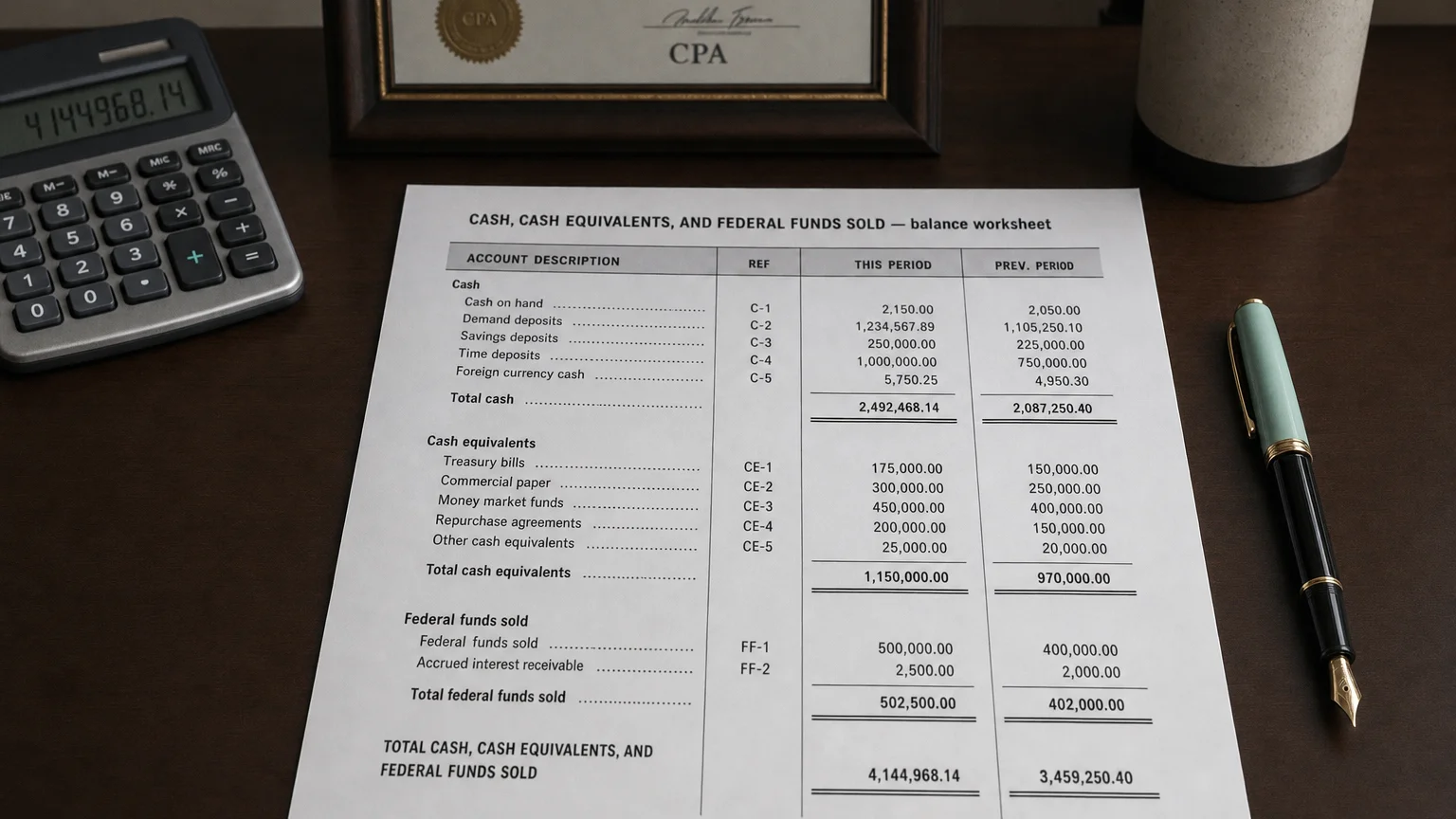

Cash, Cash Equivalents, and Federal Funds Sold is a bank balance sheet line that groups vault cash, Federal Reserve deposits, and overnight unsecured loans to other banks (federal funds sold) into a single measure of immediate liquidity, typically the first asset line reported.

It is all about redundancy. Nature likes to overinsure itself.

Cash, Cash Equivalents, and Federal Funds Sold is a line item commonly seen on the balance sheets of banks and financial institutions. It combines traditional cash and cash equivalents with federal funds sold—short-term (usually overnight) unsecured loans to other depository institutions in the federal funds market. This represents the bank’s most liquid resources available for immediate operations, lending, or meeting reserve requirements.

Breakdown of the Components

This aggregated line includes:

Cash and Cash Equivalents

- Vault cash and currency

- Deposits at Federal Reserve (reserve balances)

- Deposits with other banks

- Very short-term investments (≤3 months)

Federal Funds Sold

- Overnight loans to other banks

- Settled through Fedwire

- Earn federal funds rate

Together, they form the bank’s immediate liquidity pool.

“It is all about redundancy. Nature likes to overinsure itself.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Antifragile: Things That Gain from Disorder (2012)

Why Banks Report It This Way

Banks operate differently from non-financial companies. Their ‘cash’ isn’t just for paying bills—it’s actively managed for:

- Meeting daily settlement needs

- Satisfying reserve requirements

- Earning modest return on excess reserves

- Providing intraday liquidity

Federal funds sold turns idle cash into interest-earning assets overnight.

A Simple Example

A regional bank ends the day with:

- $50M in vault cash and Fed reserves → Cash/Cash Equivalents

- $150M excess reserves lent overnight to another bank → Federal Funds Sold

Total line: 150M returns plus a day’s interest at the fed funds rate.

This cycle repeats daily—banks constantly lend excess and borrow when short.

How It Appears

On bank balance sheets (top of assets):

- ‘Cash, Cash Equivalents, and Federal Funds Sold’

- ‘Cash and Due from Banks’ + separate ‘Federal Funds Sold’

- Often the first or second asset line

Footnotes detail reserve requirements and average balances.

Real-World Dynamics

In normal times, banks minimize excess cash and maximize fed funds sold to earn the rate. During crises or when reserves pay interest (post-2008), banks hold large balances at the Fed.

2020-2023 saw trillions in reserves as QE flooded the system—fed funds sold dropped near zero.

What to Look For

- Size vs. deposits (liquidity coverage)

- Trend (rising = caution or excess reserves)

- Fed funds sold portion (active liquidity management)

- Interest earned vs. rate environment

- Comparison to federal funds purchased (net position)

Very high balances can mean low lending appetite or abundant system liquidity.

Q · 01What are federal funds sold on a bank balance sheet?+

Q · 02How does the line differ from standard cash and cash equivalents?+

Q · 03Why do banks lend excess reserves overnight instead of holding them?+

Q · 04What does a rising federal funds sold balance indicate?+

Q · 05How does this line relate to the fed funds purchased line?+