Restricted Cash is a financial concept covered in this article. Cash Not Freely Available for General Use

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

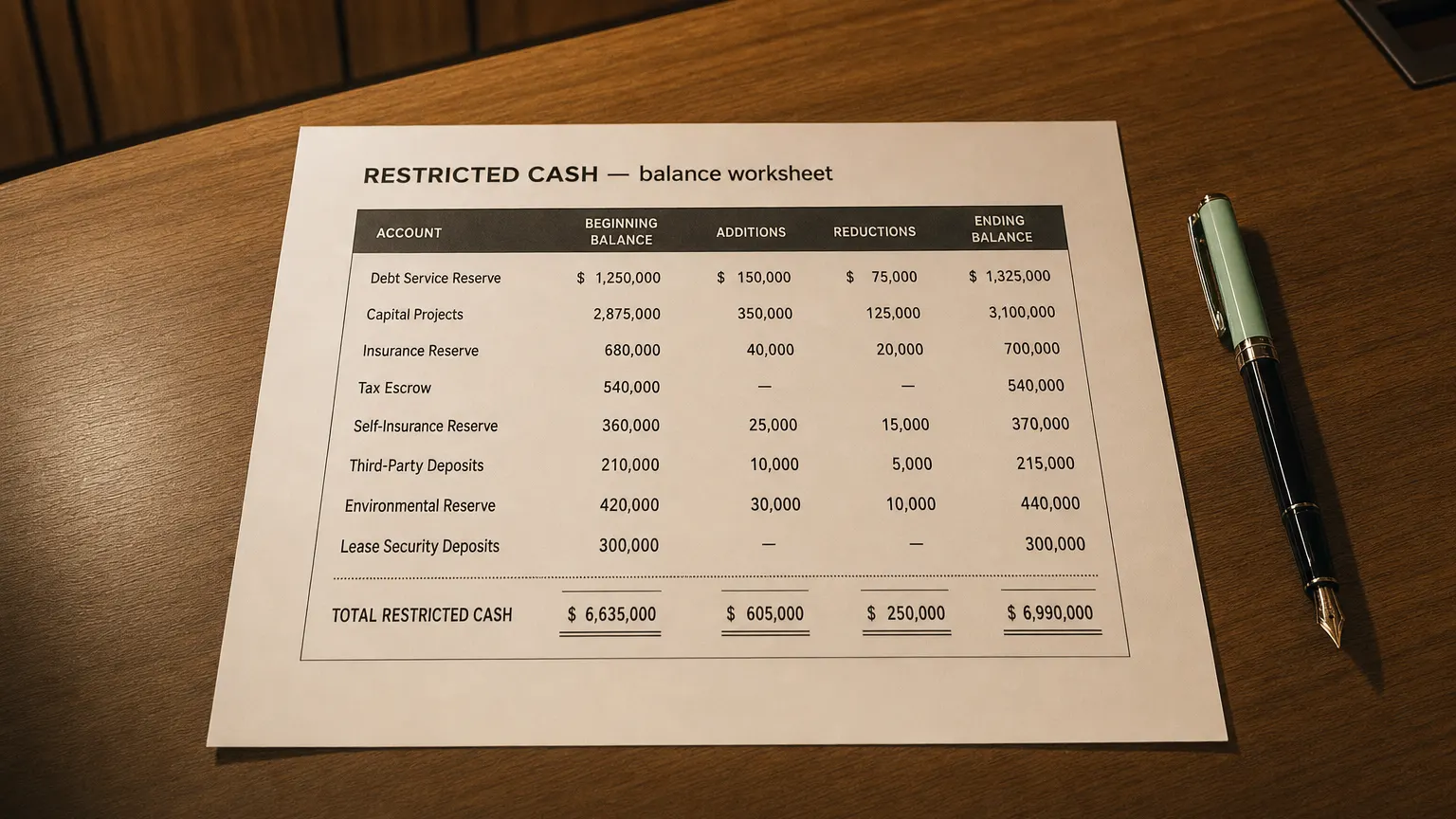

Restricted Cash refers to cash and cash equivalents that are not available for immediate or general business use due to legal, contractual, or other restrictions. These funds are set aside for specific purposes—such as debt service, collateral, escrow, or regulatory requirements—and are reported separately from unrestricted cash to provide a clear picture of true liquidity.

What Restricted Cash Includes

Restricted Cash covers cash balances subject to external constraints:

- Debt service reserve accounts (for bond/loan repayments)

- Escrow funds (M&A, legal settlements, real estate)

- Compensating balances (minimum deposits for credit lines)

- Collateral for letters of credit or derivatives

- Customer deposits held (utilities, rentals)

- Regulatory reserves (banks, insurance)

- Construction or project-specific funds

The key: management cannot use it freely for operations.

Distinguished from unrestricted cash by purpose and access limits.

Common Examples

- Homebuilder holds buyer deposits in escrow until closing

- Bank maintains compensating balance for a revolving credit facility

- Company sets aside funds for upcoming debt principal payment

- Insurance firm segregates policyholder premiums

- Mining company restricts funds for environmental reclamation

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Accounting Treatment

- Classified current if restriction lifts within 12 months

- Non-current if longer-term (e.g., sinking fund for 10-year bond)

- Reported separately from unrestricted cash

- Cash flow statement: Often investing or financing activity

- Reconciliation of total cash (including restricted) in notes

ASU 2016-18 requires reconciliation of total cash including restricted amounts.

Balance Sheet Presentation

Shown as:

- ‘Restricted Cash’

- ‘Restricted Cash and Cash Equivalents’

- Current or non-current based on restriction timing

- Sometimes in ‘Other Assets’ with clear labeling

Footnotes explain nature, amount, and expected release.

Why Companies Have Restricted Cash

- Comply with debt covenants

- Secure financing or letters of credit

- Protect third-party funds (escrow, deposits)

- Meet regulatory capital/reserve rules

- Segregate project-specific funding

Analytical Implications

- True liquidity lower than headline cash

- Debt or contractual commitments

- Regulatory environment (banks, insurers)

- Upcoming large outflows (debt repayment, project spend)

- Cash flow classification (investing vs. operating)

High restricted cash reduces operational flexibility—focus on unrestricted balance.

Q · 01What is Restricted Cash?+