is a financial concept covered in this article. Short-Term Costs Capitalized for Future Benefit Within One Year

Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.

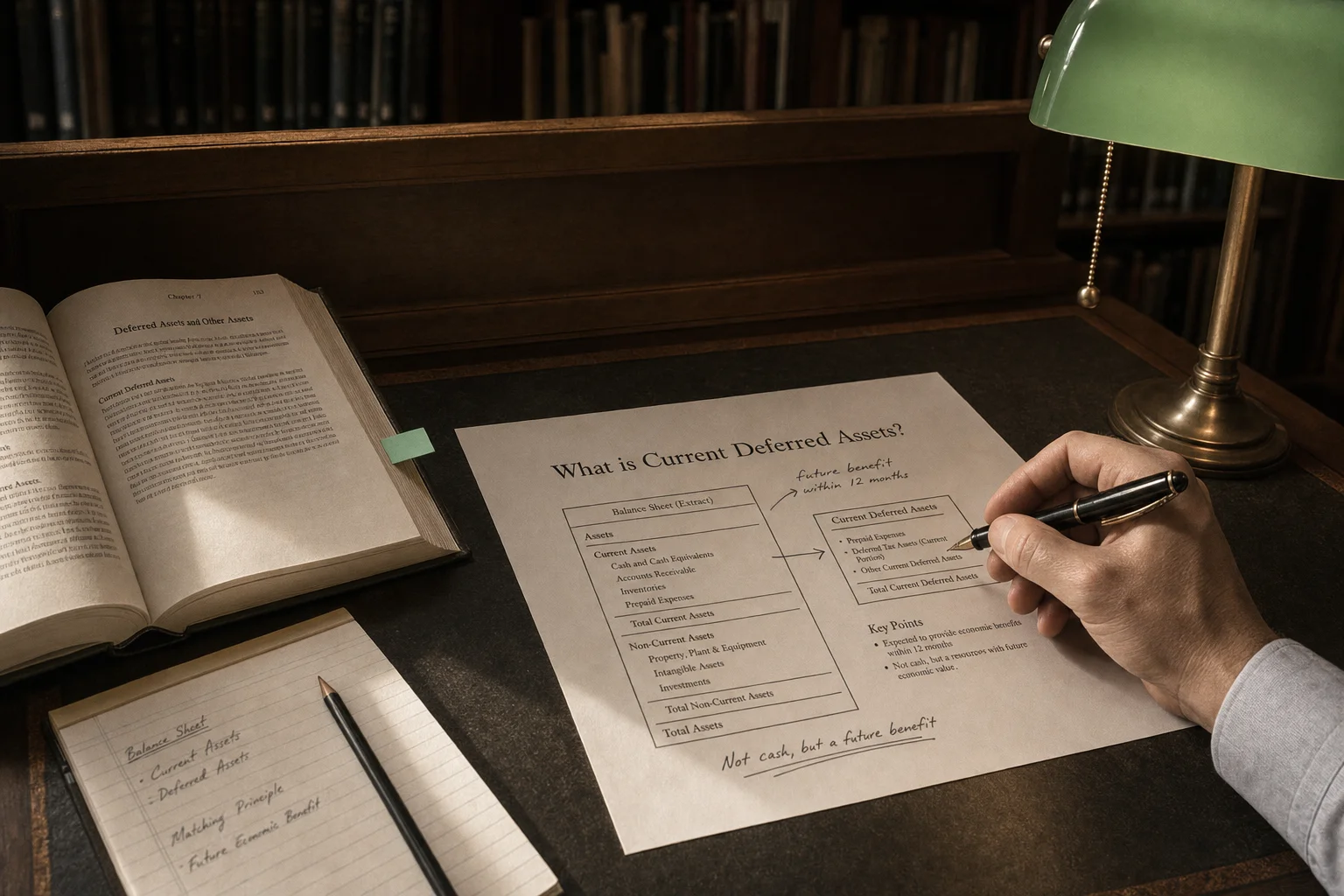

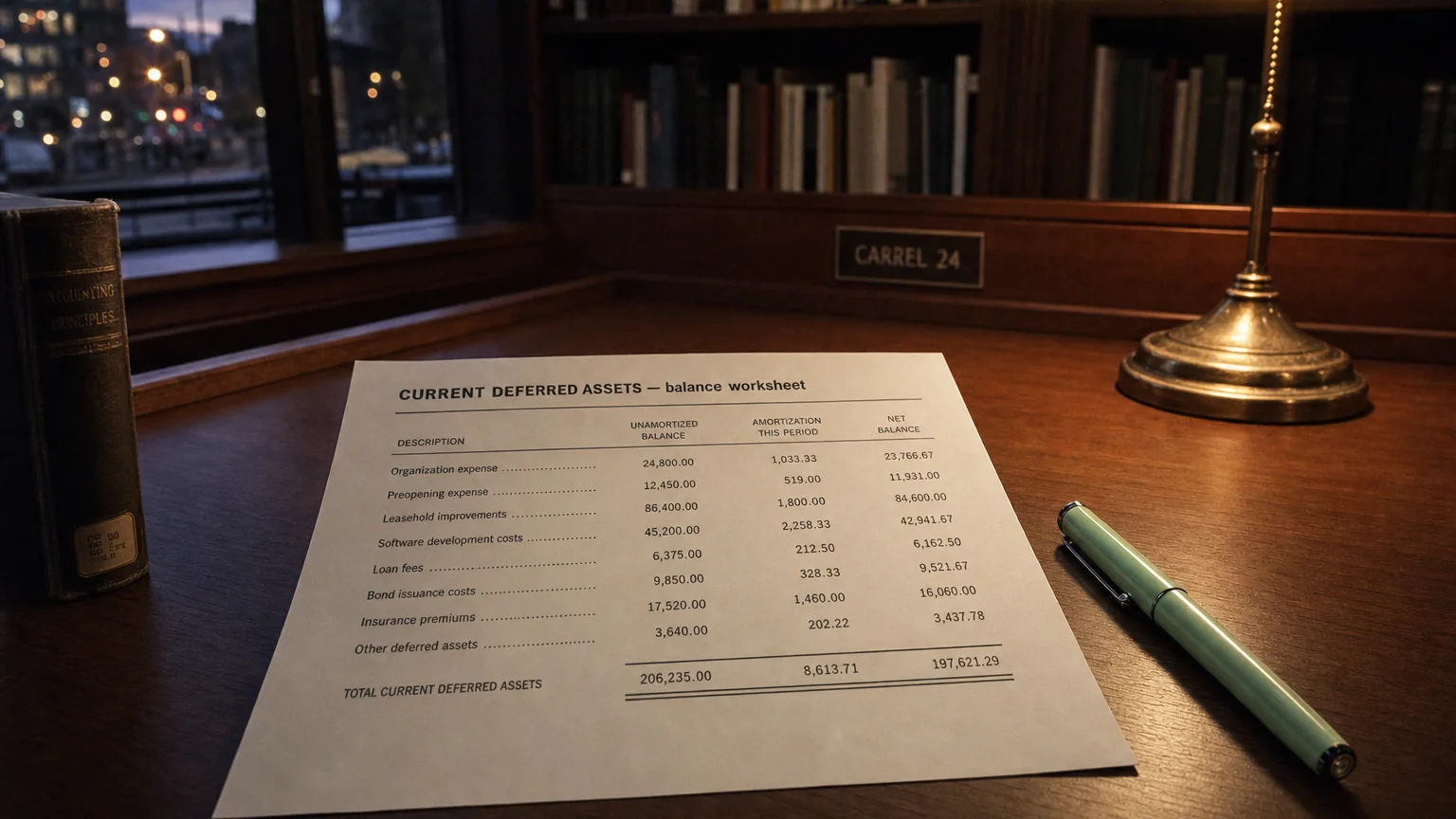

Current Deferred Assets (or Current Deferred Charges) are costs or payments that have been incurred or made in the current period but whose economic benefit will be realized within the next 12 months or operating cycle. These are capitalized as assets rather than expensed immediately, then amortized to expense as the benefit is consumed, following the matching principle.

What They Represent

Current Deferred Assets capture expenditures that provide future value within the short term. Instead of hitting expense all at once, they’re spread over the months the company actually benefits.

The ‘current’ label means the benefit (and thus amortization) will occur within one year.

Often overlaps with short-term portion of prepaid expenses or deferred charges.

Common Examples

“Volatility is far from synonymous with risk. Popular formulas that equate the two have caused students, investors, and CEOs to make many costly errors.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 2014 (2014)

- Current portion of debt issuance costs (financing fees for short-term debt)

- Short-term prepaid insurance, rent, or advertising

- Deferred loan origination costs expected to amortize soon

- Current portion of capitalized software implementation costs

- Short-term contract acquisition costs (under ASC 340/IFRS 15)

- Prepaid subscriptions or licenses with <1 year remaining

Finance teams and companies with short-term borrowing show these most prominently.

A Simple Example

Company issues 500k in fees.

- Capitalize $500k as deferred asset

- At issuance: 167k current (pro-rata)

- Each month: Amortize to interest expense

- After 12 months: All remaining becomes current

Matches financing cost to the period the loan is outstanding.

Accounting Treatment

- Initial capitalization when future benefit clear

- Amortize systematically (straight-line or effective interest)

- Current portion = amount to expense within 12 months

- Reclassify from non-current as time passes

- Impair if benefit no longer expected

Debt issuance costs often netted against debt liability (US GAAP), but some still shown as asset.

Balance Sheet Presentation

Under current assets as:

- ‘Current Deferred Assets’

- ‘Deferred Charges - Current’

- ‘Prepaid Expenses - Current Portion’

- Often in ‘Other Current Assets’

Long-term portion shown in non-current assets.

Analytical Implications

- Future expense already paid (cash outflow timing)

- Amortization impact on upcoming earnings

- Short-term financing activity (debt costs)

- Contract growth (acquisition costs)

- Working capital management

Growth may indicate increasing short-term commitments or borrowing.

Q · 01What is Current Deferred Assets?+