Prepaid Assets is a financial concept covered in this article. Advance Payments for Future Expenses or Benefits

In investing, you get what you don't pay for. Costs matter enormously.

Prepaid Assets (or Prepaid Expenses) are payments made in advance for goods or services that will be received or consumed in future periods. They are recorded as current (or non-current) assets because the company has a right to future economic benefits. As the benefit is realized over time, the prepaid amount is gradually expensed, matching the cost to the period it relates to.

What Prepaid Assets Represent

Prepaid Assets arise when a company pays for something before it actually uses or consumes it. Instead of expensing the full amount immediately, it’s capitalized as an asset and gradually moved to expense as the benefit is received.

This follows the accrual basis—matching costs to the periods they help generate revenue.

Short-term prepaids (benefit within 12 months) are current assets; longer-term are non-current.

“In investing, you get what you don’t pay for. Costs matter enormously.”

— John C. Bogle, Founder, The Vanguard Group Common Sense on Mutual Funds (1999)

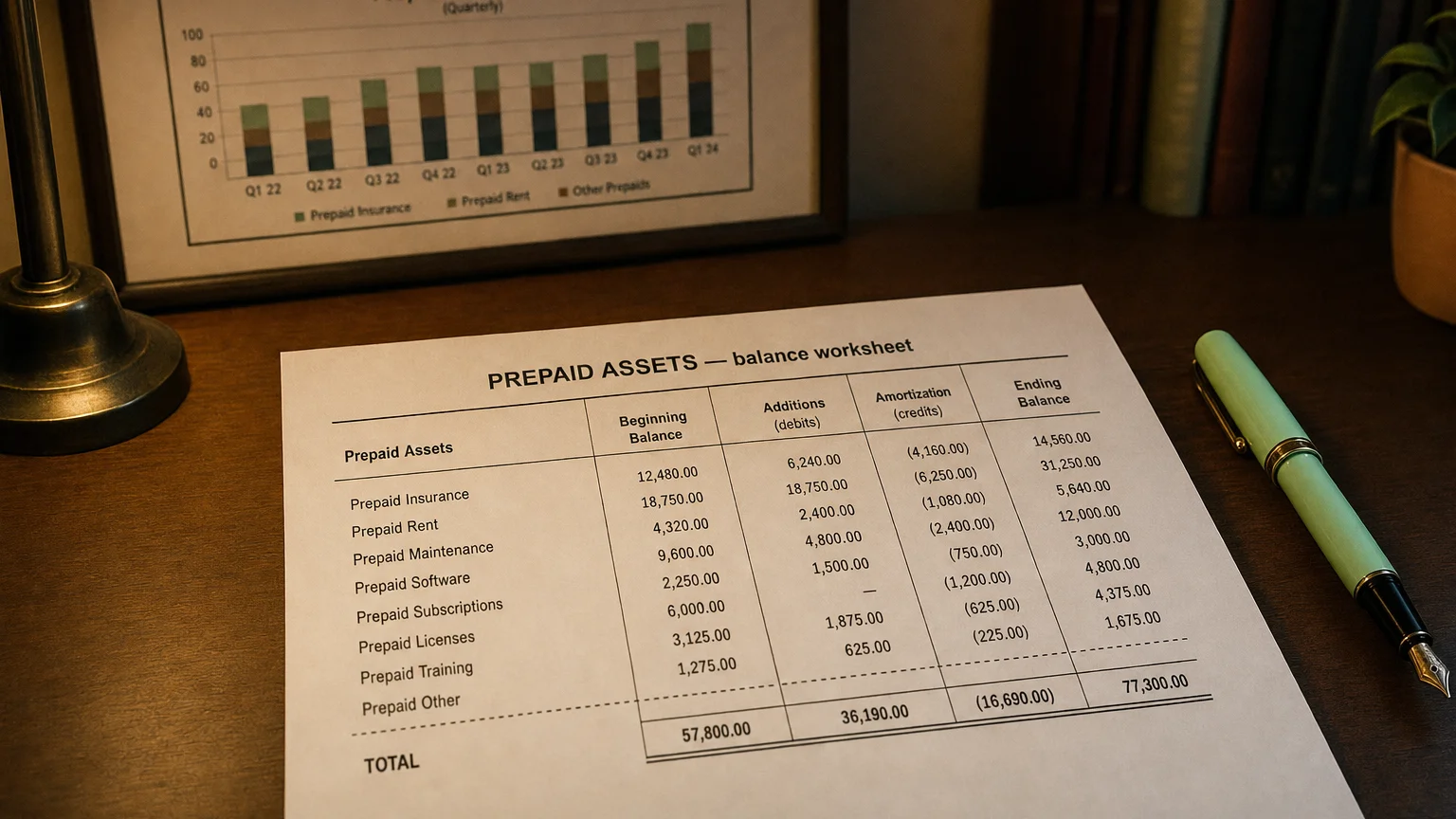

Common Examples

- Prepaid insurance premiums

- Prepaid rent or lease payments

- Prepaid advertising or marketing campaigns

- Prepaid software licenses or subscriptions

- Prepaid maintenance contracts

- Prepaid property taxes

- Prepaid interest on loans

Almost every company has some prepaid assets—insurance and rent are universal.

A Simple Example

Company pays $24,000 for a 2-year insurance policy on January 1.

- Record $24,000 Prepaid Insurance asset

- First year: Expense 12,000 remains as prepaid

- Second year: Expense remaining $12,000

At mid-year 1: 6,000 non-current prepaid.

Accounting Treatment

- Initial: Debit Prepaid Asset, Credit Cash

- Periodic: Debit Expense, Credit Prepaid Asset (straight-line usual)

- Classify current/non-current by remaining benefit period

- Impair if future benefit lost (e.g., canceled contract)

Amortization pattern should match consumption of benefit.

Balance Sheet Presentation

Under current assets (most common) or non-current as:

- ‘Prepaid Assets’

- ‘Prepaid Expenses’

- ‘Prepaid Insurance/Rent/etc.’ (detailed)

- Often in ‘Other Current Assets’ if small

Current portion of long-term prepaids shown in current assets.

Analytical Implications

- Cash outflow timing (paid now, expensed later)

- Working capital component

- Future expense visibility

- Growth signals increasing commitments

- Large non-current prepaids = long-term contracts

Rapid growth may tie up cash without immediate expense relief.

Q · 01What is Prepaid Assets?+